Rajasthan Board RBSE Class 12 Economics Chapter 11 Perfect Competition Market

RBSE Class 12 Economics Chapter 11 Practice Questions

RBSE Class 12 Economics Chapter 11 Multiple Choice Questions

Question 1.

Market for perishable commodities is :

(a) National

(b) International

(c) Local

(d) Regional

Answer:

(c)

Question 2.

The price of commodity in a perfectly competitive market is determined by:

(a) Sellers

(b) Equilibrium of demand and supply

(c) Government

(d) Finance Minister

Answer:

(b)

Question 3.

Firms in the long run under perfect competition receive:

(a) Abnormal Profit

(b) Loss

(c) Normal Profit

(d) Zero Profit

Answer:

(c)

Question 4.

In which type of market number of buyers and seller is innumerable?

(a) Oligopoly

(b) Perfect Competition

(c) Monopolistic Competition

(d) Duopoly

Answer:

(b)

Question 5.

Market for Rajasthani chunnari will be called –

(a) International

(b) National

(c) Regional

(d) Local

Answer:

(c)

RBSE Class 12 Economics Chapter 11 Very Short Answer Type Questions

Question 1.

Define the word ‘market’.

Answer:

The term market refers not necessarily to place but always to a commodity and the buyers and sellers who are in direct competition with one another to sell and buy it.

Question 2.

Give two examples of specific market.

Answer:

Two specific market are the following

(a) Jewellery Market

(b) Cloth Market.

Question 3.

What do you mean by Online Market?

Answer:

Online market is a form of electronic commerce that allows consumers to buy goods or services directly from the seller on the Internet using a web browser. The buyers and sellers do not come in contact directly. Examples are Amazon, Flipkart, etc.

Question 4.

Write down any two characteristics of perfect competition market.

Answer:

(a) There are large number of buyers and sellers and their demand and supply is a small fraction of the total market demand and supply of the product.

(b) There is no restriction on the entry of new firms into the market or on the exit of existing firms from the market.

RBSE Class 12 Economics Chapter 11 Short Answer Type Questions

Question 1.

Differentiate betweens retail and wholesale market.

Answer:

Following are the differences between retail and wholesale market:

- In wholesale, the goods are mainly sold to the retailer who sells it to the customers.

- The wholesale price is always lower than the retail price, because the retailer has to include many other costs while selling the goods, like the salaries of employees, rent of shop, tax, and advertising of the goods that he buys from a wholesaler.

- The wholesaler has direct links with the manufacturer and he buys products or goods directly from him. On the other hand, a retailer has no direct contact with the manufacturer.

Question 2.

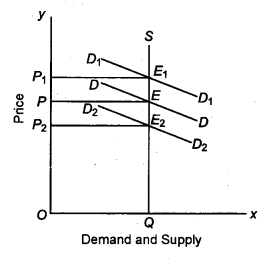

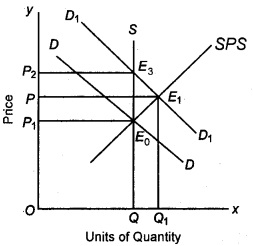

What do you mean by very short period market? Explain with the help of figure.

Answer:

In this market, due to limited time period, we can neither increase the sale or decrease the sale. It means that supply is completely fixed. Only demand may change. Perishable commodities are included in this type of market. For example, milk, curd, butter, fruits, vegetables, eggs, etc.

In the given figure, on X axis, we have taken units of quantity, and on Y axis, price of the commodity. Since supply is fixed, therefore, supply curve SQ is a vertical line parallel to Y axis. Demand and supply is equal at point E, and price of commodity is determined at OP. Due to increase in demand, demand shifts upwards and new demand curve is D1D1. The new equilibrium point is at and new price is OP1. On the contrary, due to decrease in demand, the demand curve shifts downwards and new demand curve is D2D2. The new and supply is at E2. The price decreases and new price is OP2. Therefore, in very short period market, since supply is fixed, demand alone determines the price.

Question 3.

Classify the market according to time period.

Answer:

According to the time period, the market is divided into 4 parts :

(i) Very Short Period Market : In this market, due to limited time period, we cannot increase sales or reduce sales. This means that the supply is completely fixed and only the demand can change. In this type of market, there are perishable items such as milk, curd, butter, fruits, vegetables, eggs, etc.

(ii) Short Period Market: The time period in this market is so short that by changing only the variable factors, the supply can be increased. In this market, time is sufficient for the manufacturer to increase the production by using the full potential of the current capacity.

(iii) Long Run Market: When the period of time is so long that it is possible to adjust the production according to the demand, then it is a long-term situation. Since the time duration is quite long, we can change all the variable and fixed factors, and can adjust both the supply and demand.

(iv) Very Long Period Market : Here, the time period is so long that it is possible to bring long lasting changes in demand and supply. Due to new products, new technology and new innovations, the supply side completely changes. Demand-side varies completely due to changes in consumers’ choices, likes, taste, fashion, size and composition of population, etc.

Question 4.

What do you mean by perfect competition market? Explain.

Answer:

Perfect Competition Market: It refers to the market condition in which there are large number of buyers and sellers of homogenous products. The price of the product is determined by the forces of demand and supply in the market. Maximum production that a firm can produce is relatively small compared to the total demand of the industry’s product so that it cannot affect the price by changing the supply of the output. With many companies and products under the perfect competition, no individual firm in this is in a position to influence the price of the product.

RBSE Class 12 Economics Chapter 11 Long Answer Type Questions

Question 1.

Describe the main characteristics of perfectly competitive market.

Answer:

A perfectly competitive market has the following characteristics :

(a) Large number of buyers and sellers : Under perfect competition, the number of sellers is assumed to be so large that the share of each seller in the total supply of a product is very small. Therefore, no single seller can influence the market price by changing his supply or can charge a higher price. Therefore, firms are price-takers, not price-makers. Similarly, the number of .buyers is so large that the share of each buyer in the total demand is very small and that no single buyer or a group of buyers can influence the market price by changing their individual 6r group demand for a product.

(b) Homogenous product: The commodities supplied by all the firms of an industry are assumed to be homogenous or almost identical. Homogeneity of the product implies that buyers do not distinguish between products supplied by the various firms of an industry. Product of each firm is regarded as a perfect substitute for the products of other firms. Therefore, no firm can gain any competitive advantage over the other firms. This assumption eliminates the power of all the firms’ suppliers to charge a price higher than the market price.

(c) Perfect mobility of factors of production : Another important characteristic of perfect competition is that the factors of production are freely mobile between the firms. Labour can freely move from one firm to another or from one occupation to another, as there is no barrier to labour mobility – legal, language, climate, skill, distance or otherwise.

(d) Free entry and free exit: There is no legal or market barrier on the entry of new firms to the industry. Nor is there any restriction on exit of the firms from the industry. A firm may enter the industry or quit it at its will. Therefore, when firms in the industry make supernormal profit for some reason, new firms enter the industry and supernormal profits are eliminated. Similarly, when profits decrease or more profitable opportunities are available elsewhere, firms leave the industry.

(e) Perfect KnowledgeBoth buyers and sellers have perfect knowledge about the market conditions. It means that all the buyers and sellers have full information regarding the prevailing and fixture prices and availability of the commodity.

(f) Transportation Cost is Zero:- Buyers and sellers are so close in a perfect competition market, that no costs are borne in movement of goods from one place to another. Product prices are constant in market because of zero transportation costs.

(g) Firms are price acceptors In a perfectly competitive market, no individual firm has any contirbution in price determination of a product. They have to accept the price determined by the industry, and no firm is a price determiner.

(h) Cut-throat Competition In this market, there is cut-throat competition between sellers.

Question 2.

Explain the price determination of industry with the help of a suitable figure under perfect competition market.

Answer:

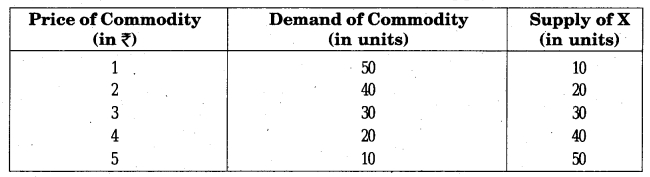

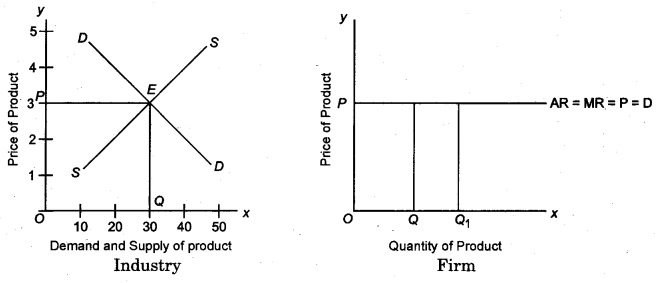

Under Perfect Competition, price of a commodity is not determined by any individual seller or a firm. It is determined by the forces of market supply and market demand for a commodity. In other words, it is determined by the industry. Equilibrium Price of a commodity is determined at that point where the market demand for the product is equal to its market supply. A firm can sell its product at the price determined by the industry. Firm cannot determine the price. It means, that demand curve of a firm is perfectly elastic or horizontal parallel to X- axis. It is further explained by the given table and fig.(a) and (b).

Schedule of Demand and Supply

It is clear from the table that equilibrium price is ₹ 3, when both demand and supply is 30 units: If price falls below this to ₹ 2, demand becomes 40 and supply falls to 20. This imbalance will again bring the price to three rupees, since all buyers won’t be able to buy the product at ₹ 2, and each buyer will be ready to pay a higher price to get the product.

Similarly, if the price increases to say ₹ 4 from ₹ 3, the product’s demand will reduce to 20 units while supply will increase to 40 units. Now, the seller will have to reduce the price to sell all his products, and it will revert to ₹ 3. Thus ₹ 3 will be the prevailing price in market. This is the equilibrium price and 30 units will be the equilibrium quantity.

This data can be further clarified with help of figures, as below :

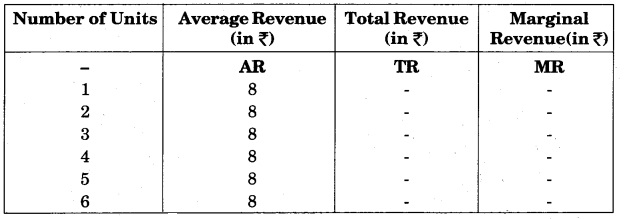

Question 3.

Calculate the total revenue and marginal revenue for the following levels:

Solution:

According to the formula:

Marginal Revenue = TRn+1 – TRn

Or Total Revenue = Average Revenue x units

Question 4.

‘Perfect competition is an imaginary concept.” Explain.

Answer:

Perfect competition is that condition of market where there are large numbers of buyers and sellers who have full knowledge of market. In perfectly competitive market, same type of products are available which are sold or bought at the same price (at a particular time). In this condition, there is no role of firms and individual buyers for determining price. In this condition, the transportation costs are zero and full mobility is found in resources. There is no obstacle in entry or exit of new firms and old firms.

If we focus on these features, then it is clear that these conditions are not seen in actual life. This condition can be an ideal condition, but it is impossible to be found in actual life. That’s why condition of perfect competition is called imaginary condition. Its study can have the theoretical significance, but there is no practical significance of this concept.

RBSE Class 12 Economics Chapter 11 Other Important Questions – Answers

RBSE Class 12 Economics Chapter 11 Multiple-Choice Questions

Question 1.

Assume that when price is ₹ 20, quantity demanded is 9 units, and when price is ₹ 19, quantity demanded is 10 units. Based on this information, what is the marginal revenue resulting from an increase in output from 9 units to 10 units?

(a) ₹ 20

(b) ₹ 19

(c) ₹ 10

(d) ₹ 1

Answer:

(c)

Question 2.

Assume that when price is ₹ 20, quantity demanded is 15 units, and when price is ₹ 18 quantity demanded is 16 units. Based on this information, what i is the marginal revenue resulting from an increase in output from 15 units to 16 units?

(a) ₹ 18

(b) ₹ 16

(c) ₹ 12

(d) ₹ 28

Answer:

(c)

Question 3.

Marginal Revenue is equal to :

(a) The change in price divided by the change in output.

(b) The change in quantity divided by the change in price.

(c) The change in P x Q due to one unit change in output.

(d) Price, but only if the firm is a price determiner

Answer:

(c)

Question 4.

Which of the following is not an essential condition of perfect competition?

(a) Large number of buyers and sellers

(b) Homogenous product

(c) Freedom of entry

(d) Absence of transport cost

Answer:

(d)

Question 5.

What is the shape of the demand curve faced by a firm under perfect competition?

(a) Horizontal

(b) Vertical

(c) Positively sloped

(d) Negatively sloped

Answer:

(a)

Question 6.

Which is the first order condition for the firm’s profit to be maximum?

(a) AC = MR

(b) MC = MR

(c) MR = AR

(d) AC = AR

Answer:

(b)

Question 7.

Assume that consumer’s income and the number of sellers in the market for good A both decrease. Based upon this information, we can conclude, with certainty, that equilibrium:

(a) Price will increase

(b) Price will decrease.

(c) Quantity will increase

(d) Quantity will decrease

Answer:

(d)

Question 8.

Which of the following is not a condition of perfect competition?

(a) A large number of firms.

(b) Perfect mobility of factors.

(c) Informative advertising to ensure that consumers have good information.

(d) Freedom of entry and exit into and out of the market.

Answer:

(c)

Question 9.

Which of the following is not a characteristic of a perfectly competitive market?

(a) Large number of firms in the industry.

(b) Output of the firms are perfect substitutes for one another.

(c) Firms face downward-sloping demand curves.

(d) Resources are very mobile.

Answer:

(c)

Question 10.

Price-accepting firms, i.e., firms that operate in a perfectly competitive market, are said to be “small”, relative to the market. Which of the following best describes this smallness?

(a) The individual firm must have fewer than 10 employees.

(b) The individual firm faces a downward-sloping demand curve.

(c) The individual firm has assets of less than ₹ 20 lakh.

(d) The individual firm is unable to affect market price through its output decisions.

Answer:

(d)

Question 11.

In which form of the market structure is the degree of control over the price of its product by a firm very large ?

(a) Monopoly

(b) Imperfect Competition

(c) Oligopoly

(d) Perfect Competition

Answer:

(a)

Question 12.

Price discrimination will be profitable only if the elasticity of demand in different market in which the total market has been divided is:

(a) Uniform

(b) Different

(c) Less

(d) Zero

Answer:

(b)

Question 13.

The firm in a perfectly competitive market is a price acceptor. This designation as a price acceptor is based on the assumption that:

(a) The firm has some, but not complete, control over its product price.

(b) There are so many buyers and sellers in the market that any individual firm cannot affect the market.

(c) Each firm produces a homogenous product.

(d) There is easy entry into or exit from the market place.

Answer:

(b)

Question 14.

A perfectly competitive firm’s supply schedule in the short run is determined by-

(a) Its average revenue

(b) Its marginal revenue

(c) Its marginal utility for money curve

(d) Its marginal cost curve

Answer:

(d)

Question 15.

In perfect competition in the long run there will be no :

(a) Normal profits

(b) Above-normal profit

(c) Production

(d) Costs

Answer:

(b)

Question 16.

An Agricultural goods market depicts the characteristics close to :

(a) Perfect Competition

(b) Oligopoly

(c) Monopoly

(d) Monopolistic Competition

Answer:

(a)

Question 17.

Which of the following markets would most closely satisfy the requirement for a perfectly competitive market ?

(a) Electricity

(b) Cable television

(c) Cola

(d) Milk

Answer:

(d)

Question 18.

In perfect competition firm is the :

(a) Price maker and not price taker

(b) Price taker and not price maker

(c) Neither price maker nor price taker

(d) None of the above

Answer:

(b)

Question 19.

The condition for perfect competition is:

(a) Large number of buyers and sellers, free entry and exit

(b) Homogenous product

(c) Both (a) and (b)

(d) None of these

Answer:

(c)

Question 20.

When the perfectly competitive firm and industry are in long run equilibrium then:

(a) P = MR = SAC = LAC

(b) D = MR = SMC = LMC

(c) P = MR = Lowest point on the LAC curve

(d) All of the above

Answer:

(d)

RBSE Class 12 Economics Chapter 11 Very Short Answer Type Questions

Question 1.

What do you mean by local market?

Answer:

When the buyers and sellers of product are spread to a village, suburb or township, then the market is called local market. Example Markets for perishable goods -butter, eggs, milk, vegetables, etc.

Question 2.

What do you mean by regional market?

Answer:

When the market of any product is limited to a region only, then it is called regional market. Example:- Semi-durable goods – Shirts.

Question 3.

What is national market?

Answer:

When the product’s buyers and sellers are spread all over the country, then the market of that product is called the national market. Examples:Durable goods and industrial goods.

Question 4.

What is international market?

Answer:

When the buyers and sellers of the product are spread in different countries of the world, the market of that product is called the international market.

Question 5.

What do you understand by common market?

Answer:

When the sale and purchase of various products is done in a market, that market is called the general market.

Question 6.

What is special market?

Answer:

When in any market the sale and purchase of a specific product is done, then that market is called special market.

Question 7.

What is the meaning of retail market?

Answer:

The retail market is the market in which the product is sold to the consumer in small quantities.

Question 8.

What is the meaning of wholesale market?

Answer:

The wholesale market is the market in which the product is sold to the consumer in bulk or in wholesale. Most of these products are bought by retailers.

Question 9.

What do you mean by very short period market?

Answer:

In this market, due to limited time period, the sale of the product does not increase or decrease. It means supply is completely fixed. Only demand may change. Example: Perishable product – milk, curd, butter, fruits, vegetables, eggs, etc.

Question 10.

What is short period market?

Answer:

The time period in this market is such that supply can be increased or decreased by changing the variable factors only.

Question 11.

What do you understand by long-run market?

Answer:

When the period of time becomes so long that it is possible to adjust the production according to demand, then it is a long-term situation. Since the time duration is quite long, we can change all the variable as well as fixed factors. Changing the fixed and variable factors can help adjust both, the supply and the demand.

Question 12.

What is the meaning of perfect competition market?

Answer:

Perfect competition refers to a market situation in which there are large number of buyers and sellers of homogenous products. The price of the product is determined by industry with the forces of demand and supply.

Question 13.

What is the meaning of homogenous product?

Answer:

Homogenous product means that the products of various firms are indistinguishable from each other; they are perfect substitutes for one another.

Question 14.

What is the meaning of industry?

Answer:

The group of firms which produce any particular good is called industry.

Question 15.

What do you understand by cut-throat competition?

Answer:

When there is huge competition between different firms then it is called cut-throat competition.

Question 16.

How is the price of product determined in perfect competition?

Answer:

The price of the goods in perfect competition is determined by the relative strengths of the demand and supply of the industry.

Question 17.

“In perfect competition, the firm is acceptor of price”. What does it mean?

Answer:

Individual firms have no role in determining the price of the item in perfect competition. In the market, the price is determined by the industry and at the same price the firm has to sell its product, hence it is called the acceptor of price.

Question 18.

What is the shape of demand curve of perfect competition?

Answer:

The demand curve of a competitor firm is perfectly elastic, that is, it is in the form of a horizontal line parallel to the X-axis.

Question 19.

Is the perfect competition seen in the real world?

Answer:

Perfect competition is an imaginary concept. It does not exist in reality.

Question 20.

What do you mean by the absence of transportation cost?

Answer:

Buyers and sellers are so close in the perfect competition market that there is no cost to carry one item from one place to another. This is called the absence of transportation costs.

Question 21.

What are Shopping Malls?

Answer:

When companies sell various types of goods in large quantities under a single roof, they are known as shopping malls.

Question 22.

What is very long-run market?

Answer:

When the time is so long, that long term changes occur both in demand and supply, then it is called a long-run market. Organizational changes are also possible in this period.

Question 23.

What is the objective of perfect competition?

Answer:

The objective of perfect competition is to maximize the profit of the firm.

Question 24.

In relation to determining price in perfect competition, what is the position of the firm and industry?

Answer:

The price is determined by the industry in perfect competition and the firm has to accept that price.

Question 25.

What is the shape of Marginal Revenue Curve of firm in perfect competition?

Answer:

In perfect competition, a firm’s marginal revenue curve is in the form of a straight line parallel to the X axis.

RBSE Class 12 Economics Chapter 11 Short Answer Type Questions

Question 1.

What are the four characteristics of perfect competition market?

Answer:

Following are the four characteristics of perfect competition market:

(a) Large Number of Firms In perfect competition, there are large number of firms in the industry. A single firm is not in a position to influence the price of the product by increasing or decreasing its output. The individual firm under perfect competition therefore takes the price of the product as a given datum and adjusts its output to earn maximum profits. In other words, a firm under perfect competition is price taker and output adjuster.

(b) Homogenous ProductIn perfect competition, the products produced by all firms in the industry are fully homogenous and identical. It means that the products of various firms are indistinguishable from each other; they are perfect substitutes for one another.

(c) Perfect KnowledgeBuyers and sellers are fully aware of the price prevailing in the market. Buyers know it fully well at what price sellers are selling a given product. As a consequence, only one price prevails in the market.

(d) No Extra Transport Cost For one price to prevail throughout the market, it is essential that there is no extra transport cost for the consumers while buying a commodity from different sellers.

Question 2.

Who determines the price in perfect competition – Industry or Firm?

Answer:

In perfect competition, the price is fixed by the forces of market demand and market supply. It is at the price thus determined that all the firms in the industry sell their output. On its own, no firm can affect the prevailing market price. The number of firms under perfect competition is so large, that no individual firm, by changing its sale, can cause any meaningful change in the total market supply. Accordingly, the market price cannot be affected on the basis of market supply.

All firms in a perfectly competitive industry produce homogeneous products. In such a situation, if any firm fixes its price higher than the equilibrium market price, buyers would shift from this firm to other firms in the market. The policy of higher price will simply fail. Firm’s demand curve under perfect competition is perfectly elastic. It means that a firm can sell whatever amount it wishes to sell at the existing price. In such a situation, the policy of attracting buyers by lowering the price would result in unnecessary loss.

Thus, it is concluded that under perfect competition, it is neither possible nor desirable for an individual firm to change the price of the product. The firm is simply a price taker, not a price maker.

Question 3.

Classify the market on the basis of their areas.

Answer:

On the basis of area, markets are classified as follows :

(a) Local MarketWhen the buyers and sellers of product are spread to a village, suburb or township, then the market is called local market. Example : Markets for perishable goods -butter, eggs, milk, vegetables, etc.

(b) Regional MarketWhen the market of any product is limited to a region only, then it is called regional market.

Example: Semi-durable goods – Shirts.

(c) National Market When the product’s buyers and sellers are spread all over the country, then the market of that product is called national market.

Examples: Durable goods and industrial goods.

(d) International MarketWhen the buyers and sellers of the product are spread in different countries of the world, the market of that product is called the international market.

Question 4.

Classify the markets on the basis of their commodity.

Answer:

On the basis of commodity, the markets are classified as follows:

(a) Common Market: Common market is the place in which various types of products are sold and bought.

Example : Clothes, Utensils, Jewellery, grocery markets are found in a common market.

(b) Special Market: It is the market in which special kinds of products are sold and bought.

Example: Grocery market, Clothes market, Jewellery market, Fruit market, etc.

(c) Market of Sales from Sample When the sale of the goods is done by looking at the sample then it is called a market of sale by sample. Sale is usually done by showing a sample in wholesale markets.

(d) Market of Sales from GradingPurchase and sale of some items is based on grading.

Example: Usha Stitching Machine, K-68 Wheat, Lux Soap, Dalda Ghee, Hero Cycle, etc.

Question 5.

Classify the markets on the basis of their sales.

Answer:

On the basis of sales, the markets are classified as follows:

(a) Retail MarketThe market in which a small quantity of goods is sold to consumers is called Retail Market.

Example: Grocery shop of the locality, sweet shop and clothes shop, etc.

(b) Wholesale MarketIn this market, the sale of goods is done in large quantities. In this market, wholesalers sell goods to the retailer.

Example: Textile market, Drug market, etc.

Question 6.

State the short period market with the help of diagram.

Answer:

The time period in this market is so short that supply can be increased or decreased by changing the variable factors only. In this market, time period is just sufficient for the producer to increase the output by fully utilizing the existing capacity.

It is clear from the given figure that the initial demand curve DD and initial supply curve SQ intersect at each other on the E0. Therefore, OP value is determined. Since the producer can change the variable factors to a degree and the supply can change, the new supply curve is SPS. With increase in demand, new demand curve D1D1 intersects SPS supply curve at Ex and new price is OP and supply of quantity increases from OQ to OQ1.

The time period in this market is so short that by changing only the variable factors, the supply can be increased or decreased. In this market, time period is just sufficient from the manufacturer to increase the production by using the full potential of the current capacity.

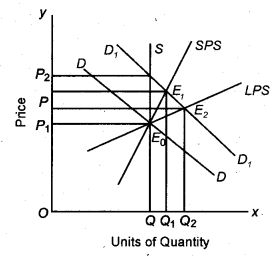

Question 7.

What do you understand by long term market? Explain.

Answer:

When the the time period becomes so long that according to the demand it is possible to adjust the production, it is a long-term condition. Since the time duration is quite long, we can change all the variable and fixed factors, and changing the fixed and variable factors can help adjust, both the supply as well as demand.

In the given figure, the initial demand curve of firm is DD. Whereas SQ is very short period supply curve. SPS is short period supply curve and LPS is long period supply curve. The initial equilibrium point is E0. It is determined by the interaction of SQ (Supply Curve) and DD (demand curve). In this stage, OP is the price and OQ is the quantity. In the long run, equilibrium is at E2, where new demand curve D1D1 intersect LPS at E2. Therefore, new price is OP1 and new quantity is OQ1.

Question 8.

What do you understand by very long term market?

Answer:

When the period of time is so long that it is possible to bring long-lasting changes in demand and supply, it is called the market for a very long time. This is due to new products, new technology and new innovation, etc. The supply side completely changes. Demand change completely due to changes in consumers, preferences, taste, fashion, size and structure of population, etc.

Question 9.

What are the differences between sales by grading and sample?

Answer:

When the products are certified, then it is called grading by sales. Example- K-68 or RR-21 Wheat, Hallmark Jewellery, etc. On the contrary, when the product is sold by showing samples, then it is called a sale by sample. Example- Order of woollen clothes received on the basis of sample.

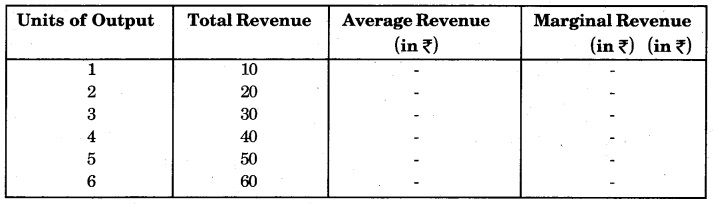

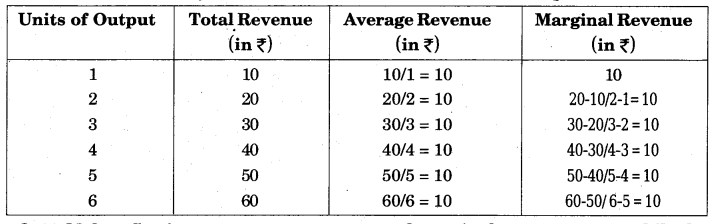

Question 10.

Find out the average revenue and marginal revenue from the following table-

Solution:

Average Revenue = Total Revenue/ Units of Output

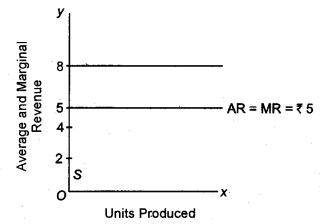

Question 11.

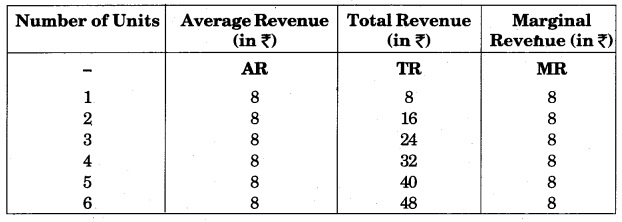

Make a firm’s average revenue curve and marginal revenue curve, while the price of the commodity in the perfect competition market decreases from ₹ 8 to ₹ 5 per unit.

Answer:

In the perfect competition market, the firm has to accept the same value which is determined by the industry. Therefore, the firm will have to sell its item at the price of ₹ 5. The average revenue and marginal revenue of the firm in this market is always equal. Its curve is of the following type –

Question 12.

Why does the supply of goods increase when the price of the item increases?

Answer:

When the price of the goods increases, the yield of the producer increases. In such a situation, at the same time, the current producer attempts to earn more profit by increasing production. On the other hand, new producers are attracted for entering the industry of this product, thereby increasing the supply of goods in the market.

Question 13.

When the price of the commodity decreases, why is the supply of the item also reduced?

Answer:

When the price of the item decreases, the benefit of the producers decreases, due to which he either reduces the production or keeps the stock in stores waiting for a reasonable price in future. Due to the decrease in price, firms which start incurring losses exit from the industry, which reduces the supply of goods.

Question 14.

On increasing the number of firms that fulfil the supply of homogenous commodity, what impact does the equilibrium of an item have on the equilibrium price and equilibrium quantity?

Answer:

When the number of firms that meet homogeneous items in the market increases, the equilibrium price of that item decreases and the equilibrium quantity increases.

Question 15.

When is equilibrium in a perfectly competitive market established?

Answer:

The equilibrium in perfect competition market is established at the point at which the demand of the product and supply of the product’s industry become equal. There is no contribution from the firm in bringing equilibrium state. Firms are acceptors of the price fixed by the industry. Changes in perfect competition are due to the changes in the demand and supply in the industry.

RBSE Class 12 Economics Chapter 11 Essay Type Questions

Question 1.

Classify the markets on the basis of area, on the basis of commodity, on the basis of time period and on the basis of sales.

Answer:

1. On the basis of area, markets are classified as follows :

(a) Local Market When the buyers and sellers of product are spread to a village, suburb or township, then the market is called local market. Example Markets for perishable goods -butter, eggs, milk, vegetables, etc.

(b) Regional MarketWhen the market of any product is limited to a region only, then it is called regional market. Example:- Semi-durable goods – Shirts.

(c) National Market When the product’s buyers and sellers are spread all over the country, then the market of that product is called the national market. Examples: – Durable goods and industrial goods.

(d) International MarketWhen the buyers and sellers of the products spread in different countries of the world, the market of that product is called the international market.

2. On the basis of commodity, the markets are classified as follows:

(a) Common Market: The common market is the place in which various types of products are sold and bought. Example – Clothes, Utensils, Jewellery, grocery markets are found in a common market.

(b) Special Market: It is the market in which a special kinds of products are sold and bought. Example:- Grocery market, Clothes market, Jewellery market, Fruit market, etc.

(c) Market of Sales from Sample When the sale of the goods is done by looking at the sample then it is called a market of sale by sample. Sale is usually done by showing a sample in wholesale markets.

(d) Market of Sales from GradingPurchase and sale of some items is based on grading. Example:- Usha Stitching Machine, K-68 Wheat, Lux Soap, Amul butter, Hero Cycle, etc.

3. On the basis of time period, the markets are classified as follows:

(a) Long Run Market – When the the time period becomes so long that according to the demand it is possible to adjust the product, it is a long-term condition. Since the time duration is quite long, we can change all the variable as well as fixed factors. Changing the fixed and variable factors can help adjust both the supply and demand.

(b) Short Period Market – The time period in this market is so short that supply can be increased or decreased by changing the variable factors only. In this market, time period is just so much that the producer can increase the output by fully utilizing the existing capacity.

(c) Very Long -Run Market – When the time period is so long, that long term changes occur both in demand and supply, then it is called a long-run market. Organizational changes are also possible in this period.

(d) Very Short Period Market – In this market, due to limited time period, the sale of the product does not increase or decrease. It means supply is completely fixed. Only demand may change. Example: Perishable products – milk, curd, butter, fruits, vegetables, eggs, etc.

4. On the basis of sales, the markets are classified as follows :

(a) Retail Market:- The market in which a small quantity of goods is sold to consumers is called Retail Market. Example – Grocery shop of the locality, sweet shop and clothes shop, etc.

(b) Wholesale Market – In this market, the sale of goods is done in large quantities. In this market, wholesalers sell goods to the retailer. Example: Textile market, Drug market, etc.

Question 2.

What are the characteristics of Perfect Competition? Explain.

Answer:

Following are the characteristics of perfect competition:

(a) Large number of buyers and sellers: There are so many buyers and sellers, that no person can influence the price of a commodity in the buyer’s and seller’s market. This means that the individual production of each seller is a negligible fraction of total production. Therefore, none of them is capable of influencing market price.

(b) Homogeneous products : All the firms in the perfect competition market sell homogeneous (identical) products. The products are identical in all respects like size, shape, colour, quantity, design, weight, etc. The products are perfect substitutes of one another. Therefore, cross elasticity of demand is zero.

(c) Free entry or exit of firms : The industry is characterized by the freedom of entry and exit of companies. Companies earn only normal profits in the perfect competition in the long run. In the short term, the firm can also earn unusual profit or loss. This is the reason that new companies are attracted to enter the industry and some companies come out of the industry. Therefore, due to the entry of firms and the freedom to exit, each firm only generates common profit in the long run.

(d) Perfect mobility of factors of production: The factors of production can move easily from one firm to another. Workers can move between jobs and between places. It means mobility of factors from one industry to such another industry, which gives them more remuneration. Factors may shift to other firms, if fair wages are not paid.

(e) Perfect knowledge of buyers and sellers : Firms have complete knowledge about the product market and factor market. Buyers also have perfect knowledge about the product market. In simpler words, perfect knowledge exists with the buyers and sellers regarding market conditions, i.e. price and commodities.

(f) Transport cost is ignored: In a perfectly competitive market, all firms are assumed to have equal competitive power. Hence, the element of transport cost difference is ruled out by assuming zero transport cost. If there is difference of transport cost, the competitive strength of two firms supplying identical goods will not be the same in economic sense.

(g) Price Taker and Quantity Adjuster: Firm are price takers and quantity adjusters. A firm may sell any amount of quantity by accepting the price determined by industry.

(h) Cut-throat competition : Cut-throat competition is present in this market. This is due to competition in the market among the sellers.