RBSE Class 12 Accountancy Model Paper 3 are part of RBSE Class 12 Accountancy Board Model Papers. Here we have given RBSE Class 12 Accountancy Sample Paper 3.

| Board | RBSE |

| Textbook | SIERT, Rajasthan |

| Class | Class 12 |

| Subject | Accountancy |

| Paper Set | Model Paper 3 |

| Category | RBSE Model Papers |

RBSE Class 12 Accountancy Sample Paper 3

समयः 3.15 घण्टे

पूर्णांक : 80

परीक्षार्थियों के लिए सामान्य निर्देशः

- परीक्षार्थी सर्वप्रथम अपने प्रश्न पत्र पर नामांक अनिर्वायतः लिखें।

- सभी प्रश्न करने अनिवार्य हैं।

- प्रत्येक प्रश्न का उत्तर; दी गई उत्तर-पुस्तिका में ही लिखें।

- जिन प्रश्नों में आंतरिक खण्ड है, उन सभी के उत्तर एक साथ ही लिखें।

- यह प्रश्न पत्र दो खण्डों में विभक्त है- अ और ब। खण्ड ‘अ’ सभी छात्रों के लिए अनिवार्य है।

- खण्ड ‘ब’ के दो भाग हैं, प्रत्येक भाग में सात प्रश्न हैं। परीक्षार्थी को किसी एक भाग के सभी सात प्रश्नों को हल करना है।

-

खण्ड प्रश्न संख्या अंक प्रत्येक प्रश्न अ 1-8 1 9-14 2 15-21 4 22-23 6 ब 24-25 1 26-27 2 28-29 4 30 6 - प्रश्न संख्या 22 (खण्ड-अ) तथा 30 (खण्ड-ब) में आन्तरिक विकल्प हैं। इन प्रश्नों में से आपको एक ही विकल्प हल करना है।

खण्ड – अ

प्रश्न 1.

एक फर्म में साझेदारों की न्यूनतम सदस्य संख्या क्या है? [1]

प्रश्न 2.

साझेदार कब अवकाश ग्रहण कर सकता है? [1]

प्रश्न 3.

संयुक्त जीवन बीमा पॉलिसी का समर्पण मूल्य चिट्ठे में कहाँ दिखाया जाता है? [1]

![]()

प्रश्न 4.

A, B व C साझेदार 4 : 3 : 1 के अनुपात में लाभ विभाजन करते हैं। B अवकाश ग्रहण करता है और अपने लाभ के भाग को ₹ 8,100 में बेच देता है। A द्वारा इसके लिए ₹ 3,600 व C द्वारा ₹ 4,500 दिये जाते हैं। नया लाभ विभाजन अनुपात व फायदे का अनुपात ज्ञात करें। [1]

A, B & C are partners in a firm sharing profits in the ratio of 4 : 3 : 1. B retires selling his share of profit to A&C for ₹ 8,100, ₹ 3,600 being paid by A ₹ 4,500 by C. Calculate New profit sharing ratio & Gaining ratio.

प्रश्न 5.

समझौते के द्वारा विघटन से आप क्या समझते हैं? [1]

प्रश्न 6.

पंजीकृत पूंजी का अर्थ बताइए। [1]

प्रश्न 7.

संयुक्त साहस में साहसिक की न्यूनतम संख्या कितनी होती है? [1]

प्रश्न 8.

सुरक्षा के दृष्टिकोण से ऋणपत्रों के प्रकार बताइए। [1]

![]()

प्रश्न 9.

A व B 3 : 2 के अनुपात में लाभ विभाजन करते हुए साझेदार हैं। C लाभ में 1/4 हिस्से के लिए प्रवेश करता है। C अपना हिस्सा A व B से 2 : 1 के अनुपात में प्राप्त करता है। नया लाभ विभाजन अनुपात ज्ञात करो। [2]

A and B are partners in a firm, sharing profits in the ratio of 3:2.C is admitted for 1/4th share in profits of the firm which he acquired from A & B in the ratio of 2: 1. Calculate New Profit Sharing Ratio.

प्रश्न 10.

संयुक्त साहस व साझेदारी में दो अन्तर बताइए। [2]

प्रश्न 11.

परिशोध कमीशन व अधिभावी कमीशन में क्या अन्तर है? [2]

प्रश्न 12.

यदि प्रेषणी को परिशोध कमीशन नहीं दिया जाता है तो प्रेषण के एक देनदार के ₹ 1,500 डूबत ऋण होने पर प्रेषक की पुस्तकों में क्या प्रवृिष्टि होगी? [2]

If consignee is not entitled for Delcredere commission and ₹ 1,500 due to debtors become bad, What entry will be passed in the books of consigner for such bad debts.

प्रश्न 13.

ऐसी दो मदों के नाम लिखिए जो प्राप्ति एवं भुगतान खाते में नहीं दिखाई जाती हैं। [2]

प्रश्न 14.

निम्नलिखित सूचनाओं से 1 जनवरी 2017 को प्रारम्भिक पूँजी कोष की गणना करो भवन 1,20,000, फर्नीचर, 24,000 रोकड़ हस्ते, (1.1.17) 18,700 स्थायी। जमा (1.1.2017) 25,500, बकाया चन्दा 1 जनवरी 2017, 9,700, बकाया वेतन 6,700, अग्रिम प्राप्त चन्दा जन. 6,200 खेल सामग्री के लेनदार जन. 2017 को 5,000। [2]

From the following information calculate Opening Capital funds as on 1 Jan. 2017. Building, 1,20,000. Furniture 24,000. Cash in hand (1.1.2017), 18,700. Fixed Deposite (1.1.2017), 20,500 Outstanding Subscription for 1 Jan. 2017, 9,700 Outstanding salary 6,700, Subscription Received in Advance for 1 Jan. 2017, 6,200 Creditors for Sports material as on 1 Jan. 2017, 5,000. Capital Fund (B/F)

![]()

प्रश्न 15.

X, Y और Z 5 : 3 : 2 के अनुपात में लाभ-हानि बाँटते हुए साझेदार हैं। Z फर्म को न्यूनतम ₹ 1,20,000 कमाने की गारण्टी देता है। लेकिन Z फर्म के लिए केवल ₹ 80,000 ही अर्जित करता है। फर्म द्वारा कुल कमाया गया लाभ ₹ 2,00,000 साझेदारों में लाभ के बँटवारे हेतु लाभ नियोजन खाता बनाइए। [4]

X, Y and Z are partners sharing profit in ratio 5:3:2. Z gives guarantee to firm of minimum ₹ 1,20,000 earnings but Z could earn only ₹ 80,000 for the firm. Total profit earned by the firm is ₹ 2,00,000. Prepare Profit & Loss Appropriation Account for distribution of profit among partners.

प्रश्न 16.

A, B व C एक फर्म में साझेदार हैं जिनकी पुस्तकें प्रतिवर्ष 31 मार्च को बन्द होती हैं। A की 30.6.2017 को मृत्यु हो गयी और सहमति के अनुसार मृतक साझेदार को मृत्यु की तिथि तक लाभ का हिस्सा पिछले 5 वर्षों के औसत लाभ के आधार पर निकाला जायेगा। पिछले 5 वर्षों के लाभ हैं- [4]

| वर्ष | 31.3.13 | 31.3.14 | 31.3.15 | 31.3.16 | 31.3.17 |

| लाभ-हानि | ₹ 14,000 | ₹ 18,000 | ₹ 22,000 | ₹ (10,000) हानि | ₹ 16,000 |

A, B and C are partners in a firm whose books are closed on March 31st each year. A died on 30.6.17 and according to the agreement, the share of profits of a deceased partner upto date of death is to be calculated on the basis the average profits for the last five years. The net Profits/Loss for the last 5years have been : ₹ 14,000, ₹ 18,000, ₹ 22,000, ₹ (10,000) Loss. ₹ 16,000 respectively. Calculate A’s share of the profits upto the date of death & Pass necessary Journal Entry.

प्रश्न 17.

गार्नर बनाम मरे के नियम को समझाइये। [4]

प्रश्न 18.

कम्पनी के चिट्ठे में निम्नलिखित मदों को आप किन शीर्षकों के अन्तर्गत रखेंगे [4]

(Under what headings will you show the following items in the Balance Sheet of the Company:)

- Goodwill

- Provision for Tax

- Unclaimed Dividends

- Loose Tools

- Securities Premium

प्रश्न 19.

संयुक्त साहस का लेखा करने की विधियों को संक्षेप में समझाइए। [4]

प्रश्न 20.

मुम्बई के हरीश ने 20 नग जयपुर के चैन सिंह को ₹ 1,800 प्रति नग की लागत पर प्रेषित किये। प्रेषण पर गाड़ी भाड़ा के ₹ 2,000 चुकाये। रास्ते में 4 नग क्षतिग्रस्त हो गये। बीमा कम्पनी ने हानि का 80 प्रतिशत दावा स्वीकार किया। क्षतिग्रस्त माल को प्रेषणी ने ₹ 1,000 में बेच दिया। असामान्य हानि की गणना कीजिये। [4]

Mr. Harish of Mumbai consigned sent 20 items to Chainsingh of Jaipur at ₹ 1,800 per item at cost. He spent ₹ 32,000 on consignment. On the way, 4 items are destroyed. Insurance Co. accepted 80% claim. Consignee sold destroyed goods at ₹ 1,000. Calculate the value of abnormal loss.

![]()

प्रश्न 21.

निम्नलिखित विवरण से संस्था के आय-व्यय खाते में खेल सामग्री के सम्बन्ध में व्यय की राशि ज्ञात कीजिए [4]

प्रश्न 22.

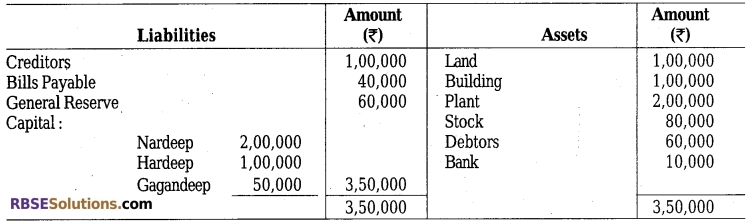

नरदीप, हरदीप तथा गगनदीप एक फर्म के साझेदार थे तथा 2 : 1 : 3 के अनुपात में लाभ बाँटते थे। 31.03.2017 को उनकी स्थिति विवरण निम्न प्रकार से था [6]

Nardeep, Hardeep and Gangandeep were partners in a firm sharing profits in 2:1: 3 ratio. Their Balance sheet as on 31.3.2017 was as follows :

1.4.2017 से नरदीप, हरदीप तथा गगनदीप ने भविष्य में लाभ बराबर-बराबर बाँटने का निर्णय लिया इसके लिए यह समझौता हुआ कि-

(क) फर्म की ख्याति का मूल्यांकन ₹ 3,00,000 किया जाये।

(ख) भूमि का पुनर्मूल्यांकन ₹ 1,60,000 पर किया जाये तथा भवन पर 6% मूल्य ह्रह्मस लगाया जाये।

(ग) ₹ 12,000 के लेनदार दावा नहीं करेंगे। अत: इन्हें अपलिखित कर दिया जाना चाहिए। पुनर्मूल्यांकन खाता, साझेदारों के पूँजी खाते तथा पुनर्गठित फर्म का स्थिति विवरण तैयार कीजिए।

From 1.4.2017, Nardeep, Hardeep and Gagandeep decided to share the future profits equally. For this purpose it was decided that ;

(a) Goodwill of the firm be valued at ₹ 3,00,000.

(b) Land be revalued at ₹ 1,60,000 and building be depreciated by 6%.

(c) Creditors of ₹ 12,000 were not likely to be claimed and hence be written off. Prepare Revaluation Account, Partners Capital Accounts and the Balance Sheet of the reconstituted firm.

अथवा

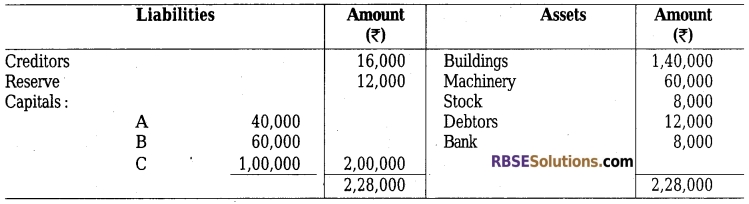

अ, ब तथा स फर्म में साझेदार थे जो अपनी पूँजियों के अनुपात में लाभों को विभाजित करते थे। 31.3.2017 को उनका स्थिति-विवरण निम्नलिखित था

A, B and C were partners in a firm sharing profits in proportion of their capitals. On 31.3.2017 their Balance Sheet was as follows:

30.6.2017 को ब का देहान्त हो गया। साझेदारी संलेख के अन्तर्गत मृत साझेदार के निष्पादकों को निम्न देय था

- साझेदार के खाते का पूँजी शेष।

- 12% प्रति वर्ष की दर से पूँजी पर ब्याज।

- ब की मृत्यु पर फर्म की ख्याति का मूल्यांकन ₹ 2,40,000 किया गया।

- पिछले वित्तीय वर्ष की समाप्ति से मृत्यु की तिथि तक लाभ का भाग पिछले वर्ष के लाभ के आधार पर, 31.3.2017 को समाप्त हुए वर्ष में लाभ ₹ 15,000 था।

ब के निष्पादकों को प्रस्तुत करने हेतु ब का पूँजी खाता बनाइए।

B.died on 30.6.2017. Under the partnership agreement, the executors of a deceased partner were entitled to:

- Amount standing to the credit of partner’s capital account.

- Interest on capital at 12% per annum.

- Share of goodwill of the firm on B’s death was valued at ₹ 2,40,000.

- Share of profit from the closing of last financial year to the date of death on the basis of last year’s profit. Profit for the year ended 31.3.2012 was ₹ 15,000.

Prepare B’s Capital Account to be rendered his executors.

प्रश्न 23.

मॉडर्न लि. ने ₹ 10 वाले 10,000 समता अंशों को ₹ 11 प्रति अंश की दर पर जनता में प्रस्तावित किया। राशि इस प्रकार देय थी- आवेदन पर ₹ 3, आबंटन पर ₹ 4 (प्रीमियम सहित) तथा प्रथम एवं अन्तिम माँग पर ₹ 4,12,000 अंशों के लिए आवेदन प्राप्त हुए तथा संचालकों ने आनुपातिक बंटन किया। राकेश जिसने 240 अंशों के लिए आवेदन किया था, ने बंटन राशि के साथ ही माँग राशि का भुगतान कर दिया। सुकेश जिसे 100 अंश बंटित किये थे, ने बंटन राशि का भुगतान माँग राशि के साथ किया। आवश्यक जर्नल प्रविष्टियाँ दीजिए। [6]

Modern Ltd. offered to public 10,000 equity shares of ₹ 10 each at ₹ 11 per share. Amount was payable as follows-on Application ₹ 3; on Allotment ₹ 4 (including premium) and on first and final call ₹ 4. Applications were received for 12,000 shares and directors alloted on pro-rata basis. Rakesh, who applied for 240 shares paid call money alongwith allotment money. Sukesh to whom 100 shares were alloted paid allotment money along with call money. Give necessary journal entries.

![]()

खण्ड -ब

प्रश्न 24.

वित्तीय विश्लेषण का अर्थ बताइए। [1]

प्रश्न 25.

अनुपात विश्लेषण का महत्व बताइये। [1]

प्रश्न 26.

एक व्यापारिक संस्था का स्कन्ध आवर्त अनुपात 15 गुना है तथा इसके औसत स्कन्ध का मूल्य ₹ 20,000 है। माल विक्रय मूल्य पर 25% लाभ पर बेचा जाता है। लाभ की गणना कीजिये। [2]

प्रश्न 27.

वित्तीय विवरण का अर्थ बताइए। [2]

प्रश्न 28.

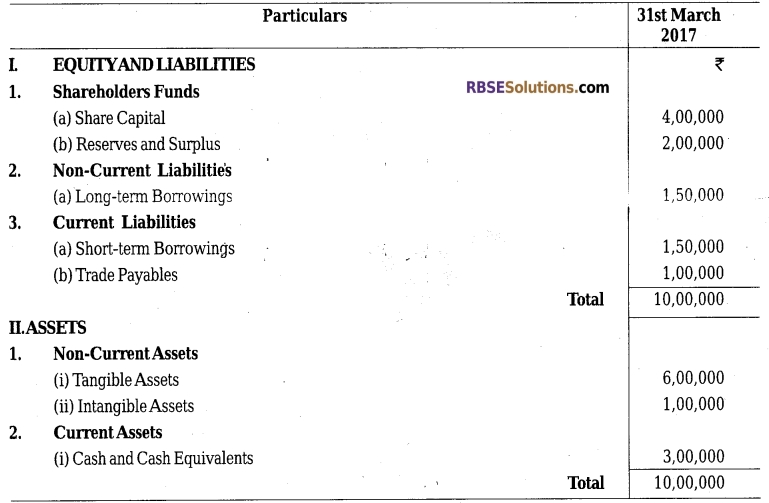

निम्नांकित चिट्ठे से समानाकार चिठ्ठा बनाइये। [4]

प्रश्न 29.

पेशेवर लेखाकार का नैतिकता से क्या सरोकार है? [4]

![]()

प्रश्न 30.

रहतिया आवर्त अनुपात 4 गुना है, अन्तिम रहतिया ₹ 10,000 अधिक है, प्रारम्भिक रहतिया से बिक्री ₹ 1,50,000 है, सकल लाभ 25% है। चालू दायित्व ₹ 20,000 है। तरल अनुपात .75 है तो चालू सम्पत्तियों की गणना कीजिए। [6]

अथवा

यदि चालू दायित्व ₹ 3,000 है, चालू अनुपात 2.25 गुना है तथा तरल अनुपात 1 : 25 गुना है। चालू सम्पत्ति, तरल सम्पत्ति एवं रहतिया की गणना कीजिए।Calculate current Assets, Liquid Assets and closing stock, if current Liabilities ₹ 3,000; Current Ratio 2.25 and Liquid Ratio 1:25 times:)

We hope the given RBSE Class 12 Accountancy Model Paper 3 will help you. If you have any query regarding RBSE Class 12 Accountancy Sample Paper 3, drop a comment below and we will get back to you at the earliest.