RBSE Class 12 Accountancy Model Paper 4 are part of RBSE Class 12 Accountancy Board Model Papers. Here we have given RBSE Class 12 Accountancy Sample Paper 4.

| Board | RBSE |

| Textbook | SIERT, Rajasthan |

| Class | Class 12 |

| Subject | Accountancy |

| Paper Set | Model Paper 4 |

| Category | RBSE Model Papers |

RBSE Class 12 Accountancy Sample Paper 4

समयः 3.15 घण्टे

पूर्णांक : 80

परीक्षार्थियों के लिए सामान्य निर्देशः

- परीक्षार्थी सर्वप्रथम अपने प्रश्न पत्र पर नामांक अनिर्वायतः लिखें।

- सभी प्रश्न करने अनिवार्य हैं।

- प्रत्येक प्रश्न का उत्तर; दी गई उत्तर-पुस्तिका में ही लिखें।

- जिन प्रश्नों में आंतरिक खण्ड है, उन सभी के उत्तर एक साथ ही लिखें।

- यह प्रश्न पत्र दो खण्डों में विभक्त है- अ और ब। खण्ड ‘अ’ सभी छात्रों के लिए अनिवार्य है।

- खण्ड ‘ब’ के दो भाग हैं, प्रत्येक भाग में सात प्रश्न हैं। परीक्षार्थी को किसी एक भाग के सभी सात प्रश्नों को हल करना है।

-

खण्ड प्रश्न संख्या अंक प्रत्येक प्रश्न अ 1-8 1 9-14 2 15-21 4 22-23 6 ब 24-25 1 26-27 2 28-29 4 30 6 - प्रश्न संख्या 22 (खण्ड-अ) तथा 30 (खण्ड-ब) में आन्तरिक विकल्प हैं। इन प्रश्नों में से आपको एक ही विकल्प हल करना है।

खण्ड – अ

प्रश्न 1.

साझेदारी फर्म से आप क्या समझते हैं? [1]

प्रश्न 2.

साझेदार की मृत्यु की दशा में लाभ ज्ञात करने की विधियाँ लिखिए। [1]

प्रश्न 3.

त्याग अनुपात ज्ञात करने का सूत्र लिखिए। [1]

![]()

प्रश्न 4.

A, B व C लाभों को \(\frac {1}{4} :\frac {2}{5} :\frac {7}{20}\) के अनुपात में बाँटते हैं। B अवकाश ग्रहण करता है तथा B का हिस्सा A व C 1 : 2 के अनुपात में क्रय करते हैं। नया लाभ विभाजन अनुपात व फायदे का अनुपात ज्ञात करो। [1]

A, B and C are partners in a firm sharing profits in the ratio of \(\frac {1}{4} : \frac {2}{5} : \frac {7}{20}\). B retires and his share is taken by A & C in the ratio of 1:2. Calculate New profit sharing ratio & Gaining ratio.

प्रश्न 5.

फर्म के समापन पर अलिखित सम्पत्तियों के विक्रय से प्राप्त राशि का लेखा कहाँ किया जाता है? [1]

प्रश्न 6.

निर्गमित पूँजी से क्या आशय है? [1]

प्रश्न 7.

संयुक्त साहस का समापन कब होता है? [1]

प्रश्न 8.

ऋणपत्रों के निर्गमन से प्राप्त प्रीमियम की राशि किस खाते में क्रेडिट की जाती है? [1]

प्रश्न 9.

A, B व C एक फर्म में साझेदार हैं जो 3 : 2 : 1 के अनुपात में लाभ विभाजन करते हैं। D लाभ में भाग के लिए प्रवेश करता है। यह अपना हिस्सा A, B व C से बराबर-बराबर प्राप्त करता है। नया लाभ विभाजन अनुपात ज्ञात करो। [2]

A, B and Care partners in a firm, sharing profits in the ratio of 3 : 2 : 1. D is admitted for 1/6th share in profits of the firm which he acquired in equal proportions from A, B & C. Calculate New Profit Sharing Ratio.

![]()

प्रश्न 10.

संयुक्त साहस पर संक्षिप्त टिप्पणी कीजिए। [2]

प्रश्न 11.

प्रेषण व विक्रय में दो अन्तर बताइए। [2]

प्रश्न 12.

2,000 किलो गुड़ ₹ 20 प्रति किलोग्राम की दर से प्रेषण पर भेजा। 100 किलोग्राम माल की सामान्य हानि हो गयी। 1500 किलोग्राम माल प्रेषणी ने बेच दिया। शेष रहे माल का मूल्य ज्ञात करिये। [2]

प्रश्न 13.

आय व्यय खाता एवं आर्थिक चिट्ठा तैयार करते समय सम्पत्ति की बिक्री का लेखा किस प्रकार करेंगे? [2]

प्रश्न 14.

एक संस्था के 1125 सदस्य हैं प्रत्येक 10 वार्षिक चन्दा देता है। वर्ष के प्रारम्भ में तथा वर्ष के अन्त में अग्रिम प्राप्त चंदे के क्रमशः ₹ 3,250 तथा ₹ 3,500 प्राप्त हुए। वर्ष के अन्त में ₹ 3,250 अदत्त चन्दा तथा वर्ष के दौरान प्राप्त चंदा ₹ 10,000 वर्ष के प्रारम्भ में अदत्त चंदे की राशि की गणना कीजिए। [2]

प्रश्न 15.

P, Q और R 3 : 2 : 1 के अनुपात में लाभ बाँटते हुए साझेदार हैं। उनके बीच तय हुआ कि [4]

- R को न्यूनतम ₹ 3,00,000 लाभ के हिस्से के रूप में दिया जायेगा।

- Q ने फर्म को गारण्टी दी कि न्यूनतम ₹ 4,80,000 फर्म को कमा कर देगा। फर्म ने चालू वर्ष में ₹ 15,20,000 की आय अर्जित की। इसमें Q द्वारा फर्म को कमा कर दी गई राशि ₹ 3,20,000 शामिल है। साझेदारों में लाभ के बँटवारे हेतु लाभ नियोजन खाता बनाइए।

P, Q and Rare Partner, sharing profit in ratio 3:2:1. It was agreed that

- Rwould get imnimum profits ₹ 3,00,000

- Q made guarantee to the firm that he would earn minimum ₹ 4,80,000. Firm earned ₹ 15,20,000 for the current year in included ₹ 3,20,000 earned by Q. Prepare Profit & Loss Appropriation Account for distribution of profit among partners.

![]()

प्रश्न 16.

A, B व C एक फर्म में साझेदार हैं जो 5 : 3 : 2 के अनुपात में लाभ विभाजन करते हैं। B अवकाश ग्रहण करता है। फर्म की ख्याति का मूल्यांकन ₹ 21.,000 पर किया गया। ख्याति के लिए आवश्यक प्रविष्टियाँ कीजिए। [4]

A, B & C are partners in a firm sharing profits in the ratio of 5:3:2. B retires and the goodwill of the firm is valued at ₹ 21,000. Pass necessary journal entries for treatment of goodwill.

प्रश्न 17.

फर्म के विघटन के समय वसूली खाता बनाने के नियम लिखिए। [4]

प्रश्न 18.

गैर-चालू सम्पत्ति शीर्षक के अन्तर्गत आने वाले पाँच उप-शीर्षकों के नाम लिखिए। [4]

प्रश्न 19.

प्रदीप और प्रवीण एक संयुक्त साहस में पुराने स्कूटरों के क्रय विक्रय के लिए सहमत होते हैं। वे लाभ हानि बराबर बाँटते हैं। प्रवीण ने प्रदीप द्वारा लिखे गये ₹ 20,000 का बिल स्वीकार किया, जिसे प्रदीप ने ₹ 19,600 में बैंक से भुना लिया। प्रदीप ने स्कूटर ₹ 35,000 में खरीदे। उसने इनकी मरम्मत के लिये ₹ 5,000 चुकाये। स्कूटर बेचने के लिए प्रवीण को भेज दिये। प्रवीण ने स्कूटर प्राप्त करने पर ₹ 600 किराया भाड़ा एवं ₹ 400 चुंगी के चुकाये। प्रवीण ने सभी स्कूटर एजेन्ट के द्वारा ₹ 60,000 में बेच दिये। एजेन्ट ने कमीशन व बिक्री व्यय के ₹ 4,200 वसूल किये। दोनों पक्षों के बीच अन्तिम भुगतान पूर्ण हो गया। प्रदीप की पुस्तकों में स्मरणार्थ संयुक्त साहस तथा प्रवीण के साथ संयुक्त साहस खाता बनाइये। [4]

Pradeep and Praveen agreed to purchase and sale of old scooter in a joint venture. They decided to share profit or losses equally. Praveen accepted bill of ₹ 20,000 drawn by Pradeep, which was discounted by Pradeep for ₹ 19,600 from bank. Pradeep purchased scooters for ₹ 36,000. He paid ₹ 35,000 for repairs of the scooter and were dispatched to Praveen for sale. Praveen paid 600 freight and ₹ 5400 octroi on the receipt of scooters. Praveen sold all the scooters through an agent for ₹ 60,000. The agent charges for commission and sales expenses ₹ 34,2000. Final settlement was completed between both parties.

Prepare Memorandum Joint Venture Account and Joint Venture with Praveen Account in the books of Pradeep.

प्रश्न 20.

100 टन कोयला ₹ 1,300 प्रति टन बीजक मूल्य तथा ₹ 800 प्रति टन लागत मूल्य पर भेजा गया। प्रेषक ने ₹ 20,000 खर्च किये। 76 टन कोयला एजेण्ट द्वारा बेचा गया जिस पर ₹ 8,000 विक्रय खर्च के प्रेषणी ने चुकाये। 5 टन कोयला कम होने की सूचना दी। एजेण्ट के पास बिना बिके स्टॉक का मूल्य ज्ञात करिये। [4]

100 ton coal sent on consignment for ₹ 1,300 per ton at invoice price and 800 per ton at cost price and consignor paid ₹ 20,000. Agent sold 76 ton coal and paid ₹ 8,000 for sales expenses. It is informed that 5 tonnes Coal is found less. Calculate the value of remaining stock with agent.

प्रश्न 21.

निम्न सूचनाओं से 1 अप्रैल, 2017 को राजक्लब की पूँजी ज्ञात कीजिए। [4]

Building ₹ 25,000 outstanding Salary ₹ 1,800 Furniture ₹ 18,000 Cash in hand ₹ 30,700. Bank overdraft ₹ 3,400 Fixed Deposit ₹ 18,000, Outstanding subscription ₹ 3,600, Creditor for Sports Material ₹ 7,200 Subscription Received in advance for next year ₹ 4,800.

![]()

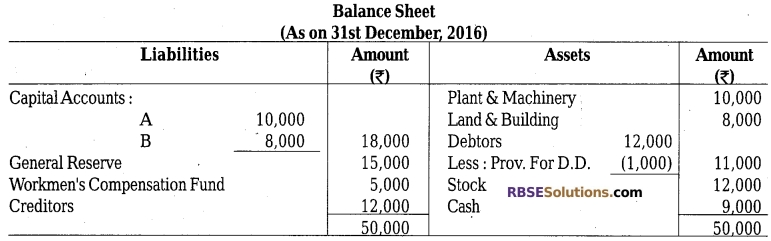

प्रश्न 22.

A तथा B साझेदार हैं। लाभ को 3 : 2 के अनुपात में बाँटते हैं। 31 दिसम्बर, 2016 को उनका स्थिति विवरण इस प्रकार था

A and B who are partners in a firm sharing profits in the ratio of 3 : 2. On 31st December, 2016 their Balance Sheet was as follows: [6]

उन्होंने C को लाभ में 1/5 हिस्से के लिए निम्नलिखित शर्तों पर साझेदारी में सम्मिलित करने का निर्णय लिया–

- संदिग्ध ऋण के लिए प्रावधान को ₹ 2,000 से बढ़ा दिया जाए।

- स्टॉक के मूल्य को ₹ 4,000 से बढ़ा दिया जाए और भूमि तथा मदन के मूल्य को ₹ 18,000 तक बढ़ा दिया जाए।

- कर्मचारी क्षतिपूर्ति कोष से दायित्व ₹ 2,000 निर्धारित किया गया है।

- C ख्याति का अपना हिस्सा है ₹ 10,000 नकद लाया।

- उपरोक्त पुनर्मूल्यांकन तथा समायोजन कर लेने के बाद C अपनी पूँजी के लिए A व B की संयुक्त पूँजी के 20% के बराबर राशि लाएगा। पुनर्मूल्यांकन खाता, साझेदारों के पूँजी खाते और C के प्रवेश के बाद फर्म का स्थिति विवरण बनाइए।

They agreed to admit C into partnership for 1/5th share of profits on the following terms:

- Provision for doubtful debts be increased by ₹ 2,000.

- The value of stock be increased by ₹ 34,000 and Land & Building be increased to ₹ 18,000.

- The liability against workmen’s compensation fund is determined at ₹ 2,000.

- C brought in as his share of goodwill ₹ 10,000 in cash.

- C would bring cash as would make his capital equal to 20% of combined capital of A & B, after the above revaluation and adjustments are carried out. Prepare Revaluation Account. Partners Capital Accounts and the Balance Sheet of the firm after C’s admission.

![]()

अथवा

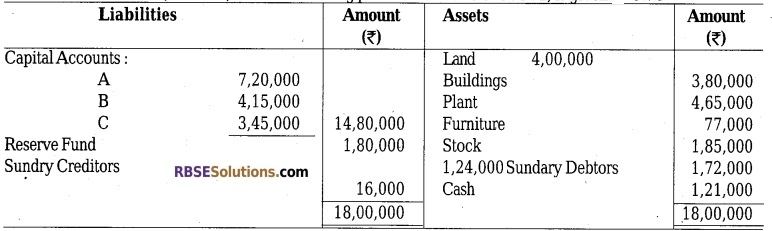

A, B और C का आर्थिक चिट्ठा, जो कि 5 : 3 : 2 के अनुपात में लाभों का विभाजन करते थे, 31 मार्च 2017 को निम्नलिखित है

The Balance Sheet of A, B, and C, who were sharing profits in the ratio of 5:3:2, is given below as at 31st March 2017:

उपर्युक्त तिथि को B अवकाश लेता है और उसके अवकाश पर निम्नलिखित समायोजनों के लिए सहमति बनी है

(अ) रहतिया का मूल्य ₹ 1,72,000 लगाया गया था।

(ब) फर्नीचर का मूल्य ₹ 3,000 से कम लगाया गया था।

(स) D से देय ₹ 10,000 की राशि संदिग्ध थी और इसके लिए प्रावधान करना आवश्यक था।

(द) फर्म की ख्याति का मूल्य ₹ 2,00,000 लगाया गया था।

(इ) B को अवकाश के समय तुरन्त ₹ 40,000 दे. दिया गया था और शेष उसके ऋण खाता में हस्तान्तरित कर दिया गया था।

(फ) A और C भविष्य के लाभों को 3 :2 के अनुपात में बाँटेंगे। पुनर्मूल्यांकन खाता, पूँजी खाते और पुनसँगठित फर्म का आर्थिक चिट्ठा बनाइए।

B retires on the above date and the following adjustments are agreed upon his retirement :

(a) Stock was valued at ₹ 1,72,000.

(b) Furniture was undervalued by ₹ 3,000.

(c) An amount of ₹ 10,000 due from D was doubtful and a provision for the same was required.

(d) Goodwill of the firm was valued at ₹ 2,00,000.

(e) B was paid ₹ 40,000 immediately on retirement and the balance was transferred to his loan account.

(f) A and C were to share future profits in the ratio of 3 : 2.

Prepare Revaluation Account, Capital Accounts and Balance Sheet of the reconstituted firm.

प्रश्न 23.

राकेश लि. ने 1 अप्रैल, 2016 को ₹ 8,00,000 के 12% ऋणपत्र जनता को प्रस्तावित किये प्रत्येक 100 वाला, सम्पूर्ण भुगतान आवेदन पर 01 मई, 2016 को या इससे पूर्व देय था। निर्गमन की शर्तों के अनुसार ऋणपत्रों पर ब्याज का भुगतान छमाही आधार पर प्रतिवर्ष 30 सितम्बर व 31 मार्च को 10% आयकर काटकर किया जायेगा। जनता से ₹ 8,000 ऋणपत्रों के लिए प्रस्ताव आये। कम्पनी ने 01 जून, 2016 को बंटन किया। कम्पनी की पुस्तकों में वर्ष 2016-17 में ब्याज के भुगतान एवं लाभ-हानि विवरण में अन्तरण की प्रविष्टियाँ दीजिये। [6]

Rakesh Ltd. offered to public 12% debentures of ₹ 8,00,000,100 each. Whole amount was payable on application on or before 1st May 2016. As per term of issue, debentures interest was payable half yearly basis on 30th September and 31st March each year, after deducting income tax at the rate of 10%. Public offered to purchase ₹ 8,000 debentures. Company made allotment of debentures on 01st June 2016. Give journal entries in the books of the company for payment of debentures interest for the year 2016-17 and transferred it to Statement of Profit & Loss A/C.

![]()

खण्ड -ब

प्रश्न 24.

तुलनात्मक चिट्ठे से आप क्या समझते हैं? [1]

प्रश्न 25.

बेचे गये माल की गणना किस प्रकार की जाती है? [1]

प्रश्न 26.

एक कम्पनी की कुल सम्पत्तियाँ ₹ 80,000 गैर चालू दायित्व ₹ 2,00,000 तथा चालू दायित्व ₹ 1,00,000 हो तो कम्पनी के [2]

- ऋण समात अनुपात

- स्वामित्व अनुपात की गणना करो।

प्रश्न 27.

वित्तीय विवरणों की कोई दो विशेषताएँ बताइए। [2]

प्रश्न 28.

निम्नांकित सूचनाओं से समानाकार लाभ-हानि खाता बनाइये [4]

प्रश्न 29.

माल के सम्बन्ध में नैतिक आधार पर लेखांकन करते समय क्या ध्यान में रखा जाना चाहिए। [4]

![]()

प्रश्न 30.

एक कं. का तरलता अनुपात 1.5, चालू अनुपात 2 और स्टॉक आवर्त अनुपात 6 गुना था। इसकी कुल चालू सम्पत्तियाँ वर्ष 2015 में ₹ 8,00,000 की थीं। यदि माल लागत पर 25 लाभ पर बेचा गया हो तो वार्षिक बिक्री बताइए। [6]

A company had a liquid ratio of 1.5 and current ratio of 2 and inventory turnover ratio 6 times. It has total current assets of ₹ 8,00,000 in the year 2015. Find out annual sales if goods are sold at 25% profit on cost.

अथवा

निम्न सूचनाओं से गणना कीजिए-

- सकल लाभ अनुपात

- स्थायी सम्पत्ति आवर्त अनुपात

- विनियोग पर प्राप्ति।

Calculate:

- Gross Profit Ratio

- Fixed Assets Turnover Ratio

- Return on Investment from the following information:

![]()

We hope the given RBSE Class 12 Accountancy Model Paper 4 will help you. If you have any query regarding RBSE Class 12 Accountancy Sample Paper 4, drop a comment below and we will get back to you at the earliest.