Rajasthan Board RBSE Class 12 Accountancy Chapter 2 नये साझेदार का प्रवेश

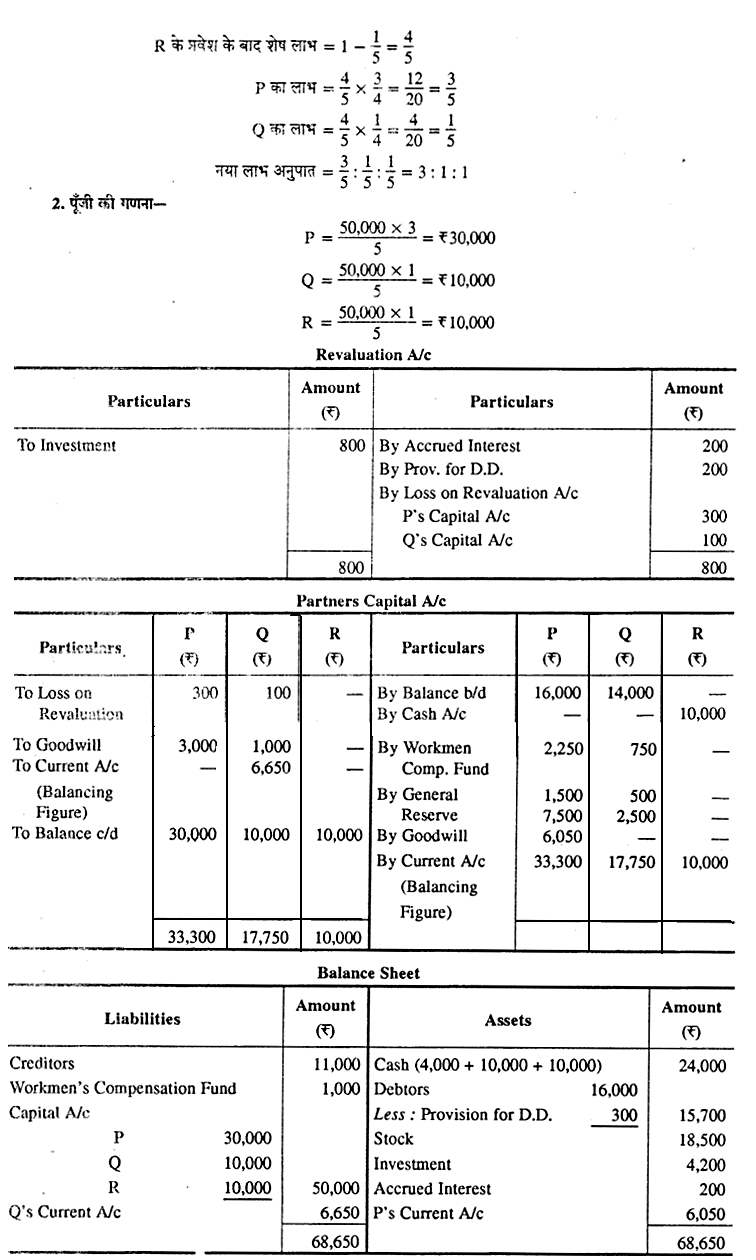

RBSE Class 12 Accountancy Chapter 2 पाठ्यपुस्तक के प्रश्न

RBSE Class 12 Accountancy Chapter 2 बहुचयनात्मक प्रश्न

RBSE Solutions For Class 12 Accountancy Chapter 2 प्रश्न 1.

अधिलाभ है

(अ) सामान्य लाभ – औसत लाभ

(ब) औसत लाभ – सामान्य लाभ

(स) सामान्य लाभ + औसत लाभ

(द) इनमें से कोई नहीं।

RBSE 12th Accountancy Book Solutions प्रश्न 2.

अ व ब बराबर के साझेदार हैं जिनकी पूँजी क्रमशः Rs 16,000 वर Rs 12,000 है, स 1/4 हिस्से के लिए प्रवेश करता है व Rs 15,000 पूँजी के लाता है तो फर्म की ख्याति का मूल्य होगा।

(अ)Rs 60,000

(ब)Rs 1,12,000

(स)Rs 17,000

(द)Rs 43,000.

![]()

RBSE Solutions For Class 12 Accountancy Chapter 2 In Hindi प्रश्न 3.

कुल सम्पत्तियाँ Rs 70,000, दायित्व Rs 10,000, औसत लाभ Rs 8,000, सामान्य प्रत्याय दर 10 प्रतिशत अधिलाभ की राशि होगी।

(अ)Rs 1,000

(ब)Rs 2,000

(स)Rs 3,000

(द)Rs 4,000.

RBSE Solutions For Class 12 Accountancy प्रश्न 4.

लाभों में हिस्सा बँटाने के लिए नया साझेदार.लाता है।

(अ) पूँजी

(ब) ऋण

(स) ख्याति

(द) इनमें से कोई नहीं।

RBSE 12 Accounts Solutions प्रश्न 5.

फर्म की सम्पत्तियों में हिस्सा पाने के लिए नया साझेदार.चुकाता है।

(अ) पूँजी

(ब) ऋण

(स) ख्याति

(द) अनुदान

RBSE Accountancy Book Class 12 Pdf प्रश्न 6.

पुनर्मूल्यांकन खाते की प्रकृति

(अ) व्यक्तिगत खाता

(ब) नाममात्र का खाता

(स) वास्तविक खाता

(द) इनमें से कोई नहीं।

RBSE Solutions For Class 12 प्रश्न 7.

नये साझेदार के प्रवेश पर जब सम्पत्तियों वे दायित्वों का मूल्य बदलना चाहते हैं, तो बनाये जाने वाला खाता होता है

(अ) पुनर्मूल्यांकन खाता

(ब) वसूली खाता

(स) स्मरणार्थ पुनर्मूल्यांकन खाता

(द) इनमें से कोई नहीं ।

RBSE Solutions For Class 12 Accountancy Chapter 2 प्रश्न 8.

सभी अवितरित हानियों को पुराने साझेदारों के पूँजी खातों में किस अनुपात में हस्तान्तरित किया जाता है

(अ) नये लाभ विभाजन अनुपात में

(ब) फायदे के अनुपात में

(स) पुराने लाभ विभाजन अनुपात

(द) त्याग अनुपात में ।

![]()

Class 12 RBSE Accounts Solutions प्रश्न 9.

ख्याति का स्वभाव होता है

(अ) बिल्ली के स्वभाव वाली

(ब) कुत्ते के स्वभाव वाली

(स) चूहे के स्वभाव वाली

(द) उपर्युक्त सभी ।

RBSE Solution Class 12 Accountancy प्रश्न 10.

A व B एक फर्म में 2:1 के अनुपात में साझेदार हैं। वे C को 1/3 हिस्से के लिए प्रवेश देते हैं तो उनको त्याग अनुपात होगा

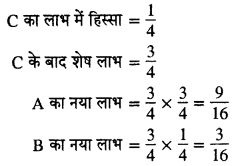

(अ) 2 : 3

(ब) 1 : 2

(स) 2 : 1

(द) 1 : 1.

उत्तर-.

1. (ब),

2. (स),

3. (ब),

4. (स),

5. (अ),

6. (ब),

7. (अ),

8. (स),

9. (द),

10. (स)

RBSE Class 12 Accountancy Chapter 2 अतिलघूत्तरात्मक प्रश्न

12th RBSE Accountancy Solutions प्रश्न 1.

फर्म में नये साझेदार द्वारा ख्याति की रकम नकद लाने पर पुराने साझेदारों में किस अनुपात में बाँटी जाती है ?

उत्तर-

त्याग अनुपात में।

12 RBSE Accounts Solution प्रश्न 2.

अधिलाभ और औसत लाभ में एक अन्तर लिखें।

उत्तर-

अधिलाभ की गणना वास्तविक औसत लाभ में से सामान्य लाभ को घटाकर की जाती है जबकि औसत लाभ की गणना पिछले कुछ वर्षों के लाभों (हानि के सहित) का औसत निकालकर की जाती है।

12th Account Book RBSE प्रश्न 3.

साझेदारी फर्म के पुनर्गठन से क्या अभिप्राय है ?

उत्तर-

साझेदारों के मध्य विद्यमान अनुबन्ध में किसी प्रकार का परिवर्तन करना ही साझेदारी फर्म का पुनर्गठन कहलाता है।

![]()

RBSE Solutions For Class 12 Accountancy Chapter 3 प्रश्न 4.

पुनर्मूल्यांकन खाते की प्रकृति क्या है ?

उत्तर-

पुनर्मूल्यांकन खाते की प्रकृति अवास्तविक खाते की होती है।

RBSE Class 12 Accountancy Solutions प्रश्न 5.

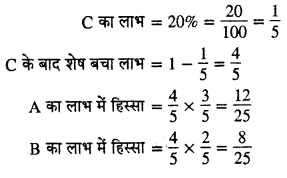

एक फर्म में A व B साझेदार हैं जो 3:2 के अनुपात में लाभ विभाजन करते हैं। C लाभों में 20% हिस्से के लिए प्रवेश करता है तो नया लाभ विभाजन अनुपात व त्याग अनुपात क्या होगा ?

A and B are partners in a firm, sharing profits in the ratio of 3:2. C is admitted for 20% share in profits of the firm. Calculate New Profit Sharing Ratio & Sacrificing Ratio.

उत्तर-

Accountancy Class 12 Book RBSE प्रश्न 6.

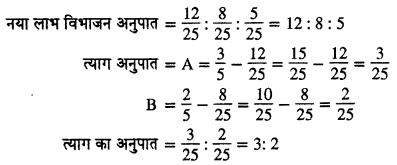

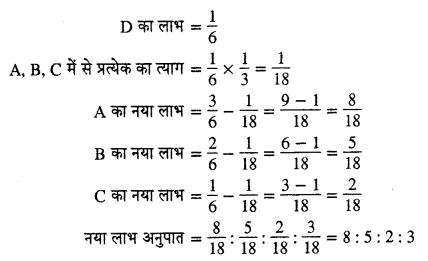

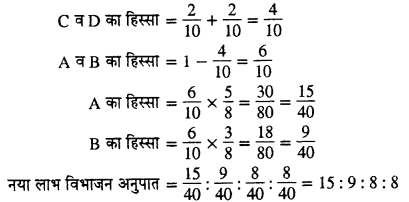

A, B C एक फर्म में साझेदार हैं जो 5:3:2 के अनुपात में लाभ विभाजन करते हैं। D लाभ में 1/5 हिस्से के लिए प्रवेश करता है। नया लाभ विभाजन अनुपात के त्याग अनुपात करो।

A, B & C are partners in a firm, sharing profits in the ratio of 5 : 3:2. D is admitted for 1/5th share in profits of the firm. Calculate New Profit Sharing Ratio & Sacrificing Ratio.

हलः

D का हिस्सा = \(\frac { 1 }{ 5 }\)

त्याग अनुपात = पुराना लाभ विभाजन अनुपात- नया लाभ विभाजन अनुपात

त्याग अनुपात = 5:3:2

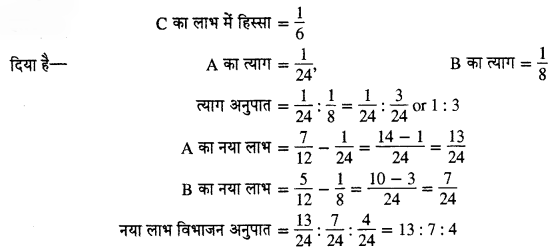

RBSE Solutions 12th Accounts प्रश्न 7.

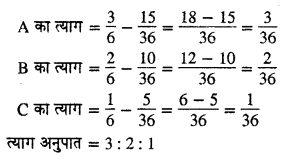

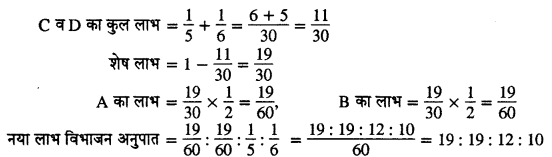

A, B व C एक फर्म में साझेदार हैं जिनका लाभ विभाजन अनुपात: \(\frac { 3 }{ 6 } :\frac { 2 }{ 6 } :\frac { 1 }{ 6 } \) है। D लाभ में 1/6 हिस्से के लिए प्रवेश करता है। नया लाभ विभाजन अनुपात व त्याग अनुपात ज्ञात करो।

A, B & Care partners in a firm sharing profits in the ratio of 3/6: 2/6 : 1/6. D is admitted for 1/6th share in profits of the firm. Calculate New Profit Sharing Ratio & Sacrificing Ratio.

हल :

नया लाभ विभाजन अनुपात = 15 : 10 : 5 : 6

![]()

12 Account Solution RBSE प्रश्न 8.

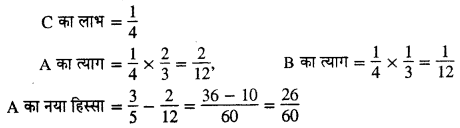

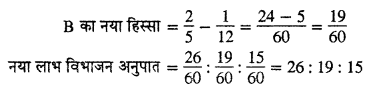

A व B एक फर्म में साझेदार हैं। C को लाभ में 1/4 हिस्से के लिए प्रवेश देते हैं। नया लाभ विभाजन अनुपात व त्याग अनुपात ज्ञात करो।

A and B are partners in a firm, sharing profits of the firm C is admitted for 1/4th share in profits of the firm. Calculate New Profit Sharing Ratio & Sacrificing ratio.

हले :

Class 12th RBSE Accounts Solution प्रश्न 9.

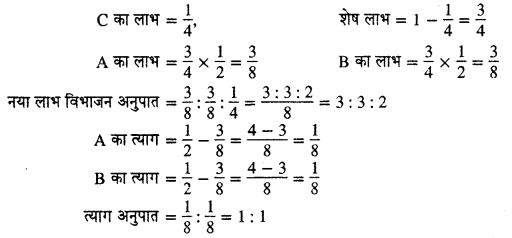

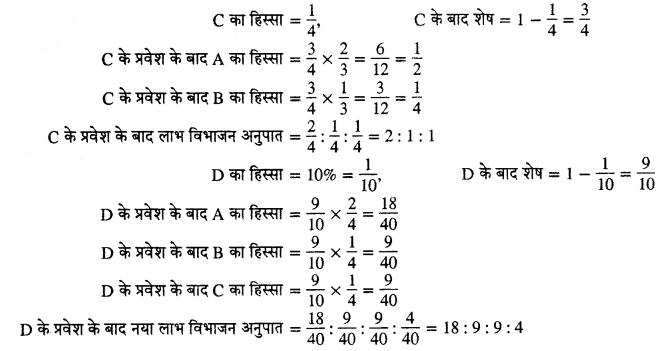

A व B एक फर्म में साझेदार हैं जो 2 : 1 के अनुपात में लाभ विभाजन करते हैं । C को लाभों में 1/4 हिस्से के लिए प्रवेश देते हैं।C के प्रवेश के बाद D को लाभों में 10% हिस्से के लिए प्रवेश देते हैं। D के प्रवेश के बाद नया लाभ विभाजन अनुपात ज्ञात करो।

A and B are partners in a firm, sharing profits in the ratio of 2 : 1. C is admitted for 1/4th share in profits of the firm. After admission of C, D is admitted for 10% share in profits of the firm. Find New Profit Sharing Ratio after admission of D.

हल:

![]()

RBSE Accounts Solutions Class 12 प्रश्न 10.

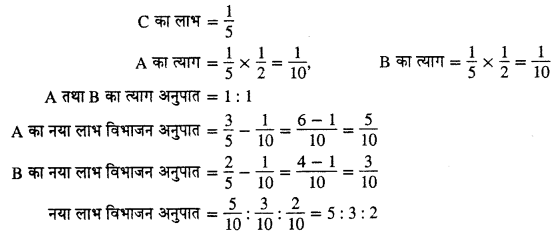

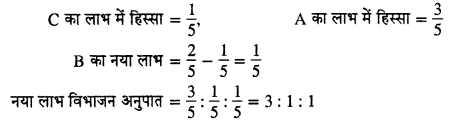

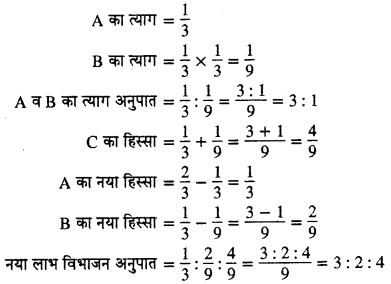

A व B एक फर्म में साझेदार हैं जो 3: 2 के अनुपात में लाभ विभाजन करते हैं। C लाभों में 1/5 हिस्से के लिए प्रवेश करता है। C को A व B से बराबर भाग प्राप्त होता है। नया लाभ विभाजन अनुपात में त्याग अनुपात ज्ञात करो।

A and B are partners in a firm, sharing profits in the ratio of 3 : 2. C is admitted for 1/5th share in profits of the firm which he acquired in equal proportions from both A & B. Calculate New Profit Sharing Ratio and Sacrificing Ratio.

हले:

RBSE Solutions For Class 12 Commerce प्रश्न 11.

A, B, C एक फर्म में साझेदार हैं जो 3:2:1 के अनुपात में लाभ विभाजन करते हैं। D लाभ में 1/6 भाग के लिए प्रवेश करता है। यह अपना हिस्सा A, B, C से बराबर-बराबर प्राप्त करता है । नया लाभ विभाजन अनुपात ज्ञात करो।

A, B and Care partners in a firm, sharing profits in the ratio of 3:2:1.D is admitted for 1/6th share in profits of the firm which he acquired in equal proportions from A, B & C. Calculate New Profit Sharing Ratio.

हल:

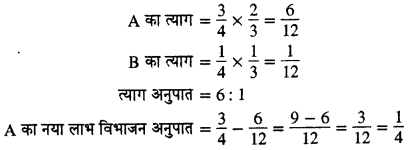

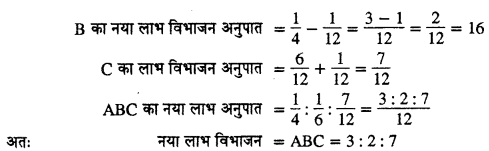

RBSE 12th Commerce Accountancy Book Solutions प्रश्न 12.

A व B 3: 2 के अनुपात में लाभ विभाजन करते हुए साझेदार हैं। C लाभ में 1/4 हिस्से के लिए प्रवेश करता है। C अपना हिस्सा A व B से 2:1 के अनुपात में प्राप्त करता है । नया लाभ विभाजन अनुपात ज्ञात करो।

![]()

A and B are partners in a firm, sharing profits in the ratio of 3 : 2. C is admitted for 1/4th share in profits of the firm which he acquired from A & B in the ratio of 2 : 1. Calculate New Profit Sharing Ratio.

हल :

Class 12th RBSE Accountancy Solutions प्रश्न 13.

A व B एक फर्म में साझेदार हैं जो 3:2 के अनुपात में लाभ विभाजन करते हैं। वे C को लाभ में 1/5 हिस्से के लिए प्रवेश देते हैं। अपना पूरा हिस्सा B से प्राप्त करता है। नया लाभ विभाजन अनुपात ज्ञात करो।

A and B are partners in a firm, sharing profits in the ratio of 3 : 2. C is admitted for 1/5th share in profits of the firm which he acquired entirely from B. Calculate new Profit Sharing Ratio.

हल :

RBSE Class 12 Accountancy Syllabus प्रश्न 14.

A व B एक फर्म में साझेदार हैं जो 7:5 के अनुपात में लाभ विभाजन करते हैं। C को लाभ में 1/6 हिस्से के लिए प्रवेश देते हैं। C 1/24 हिस्सा A से व 1/8 हिस्सा B से प्राप्त करता है। नया लाभ विभाजन अनुपात व त्याग अनुपात ज्ञात करो।

A and B are partners in a firm, sharing profits in the ratio of 7:5. C is admitted for 1/6th share in profits of the firm. C acquires 1/24 from A and 1/8 from B. Calculate New Profit Sharing Ratio & Sacrificing Ratio.

हलः

Class 12 Accountancy Solutions RBSE प्रश्न 15.

A व B एक फर्म में साझेदार हैं जो 3:1 के अनुपात में लाभ विभाजन करते हैं। C को प्रवेश देते हैं। A अपने हिस्से का 2/3 व B अपने हिस्से का 1/3 C के पक्ष में समर्पण करते हैं। नया लाभ विभाजन अनुपात व त्याग अनुपात ज्ञात करे ।

![]()

A and B are partners in a firm, sharing profits in the ratio of 3 : 1. A new partner C is admitted. A surrenders 2/3 of his share & B surrenders 1/3 of his share in favor of C. Calculate New Profit Sharing

हल:

RBSE Class 12 Accountancy Book Pdf प्रश्न 16.

A व B एक फर्म में साझेदार हैं जो 2:1 के अनुपात में लाभ विभाजन करते हैं।C को प्रवेश देते हैं। A अपने हिस्से में से 1/3 भाग व B अपने हिस्से का 1/3 C के पक्ष में त्याग करते हैं। नया लाभ विभाजन अनुपात व त्याग अनुपात करो।।

A and B are partners in a firm, sharing profits in the ratio of 2 : 1. New partner C is admitted. A surrenders 1/3 from his share & B surrenders 1/3 of his share in favor of C. Calculate New profit Sharing Ratio & Sacrificing Ratio.

हले:

![]()

RBSE 12th Accountancy Solutions प्रश्न 17.

A, B व C एक फर्म में साझेदार हैं जो 5:3:2 के अनुपात में लाभ विभाजन करते हैं। D को लाभों में 2/10 हिस्से के लिए प्रवेश देते हैं।C का हिस्सा पूर्ववत रहेगा। नया लाभ विभाजन अनुपात ज्ञात करो।

A, B & Care partners in a firm, sharing profits in the ratio of 5: 3: 2. D is admitted for 2/10 share in profits of the firm. C will retain his original share. Calculate New Profit Sharing Ratio.

हले:

Accounts Class 12 RBSE Solutions प्रश्न 18.

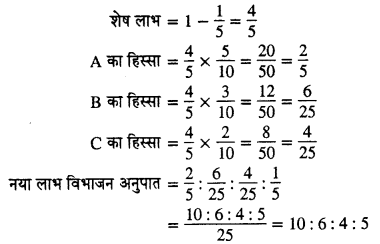

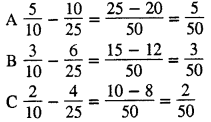

A व B एक फर्म में साझेदार हैं। वे C व D को लाभ में क्रमश: 1/5 व 1/6 हिस्सा देकर प्रवेश देते हैं। नया लाभ विभाजन अनुपात ज्ञात करो।

A and B are partners in a firm, sharing profits. They admitted C & D for 1/5th and 1/6th shares in profits respectively. Calculate New Profit Sharing Ratio.

हले:

![]()

RBSE 12 Accounts Solution प्रश्न 19.

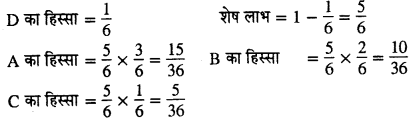

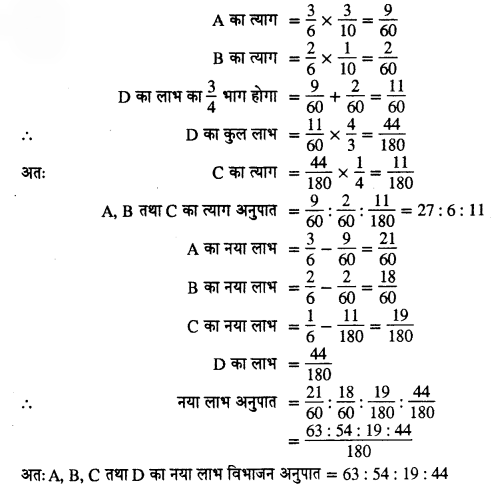

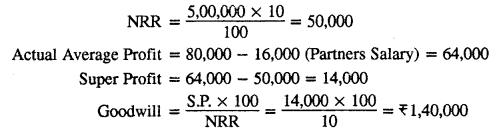

A, B, C एक फर्म में साझेदार है जो 3:2:1 के अनुपात में लाभ विभाजन करते हैं। D को प्रवेश देते हैं, D अपने हिस्से का 1/4 भाग C से प्राप्त करता है A अपने हिस्से का 3/10 भाग व B अपने हिस्से का 1/10 भाग D के पक्ष में त्याग करते हैं। नया लाभ विभाजन अनुपात व त्याग अनुपात ज्ञात करो।

हल:

RBSE Class 12 Accountancy Chapter 2 लघूत्तरात्मक प्रश्न

RBSE 12th Accountancy Book Pdf Download प्रश्न 1.

एक नये प्रवेशित साझेदार द्वारा प्राप्त अधिकारों का उल्लेख कीजिए।

उत्तर-

नये साझेदार के अधिकार—नये साझेदार को निम्नलिखित दो अधिकार प्राप्त होते हैं

- फर्म की सम्पत्तियों में हिस्सा प्राप्त करने का अधिकार नये साझेदार को फर्म का समापन होने पर उसकी समस्त सम्पत्तियों में से अपना हिस्सा प्राप्त करने का अधिकार प्राप्त होता है।

- फर्म के भावी लाभों में हिस्सा प्राप्त करने का अधिकार–नये साझेदार को साझेदारी में प्रवेश करने के दिन से ही फर्म के लाभों में अपना हिस्सा प्राप्त करने का अधिकार प्राप्त हो जाता है।

RBSE Solution Class 12th Commerce Accountancy प्रश्न 2.

लाभ-हानि समायोजन खाता या पुनर्मूल्यांकन खाता क्यों बनाया जाता है ?

उत्तर-

नये साझेदार के प्रवेश के समय सम्पत्तियों एवं दायित्वों को वर्तमान मूल्य पर दिखाने के लिए उनका पुनर्मूल्यांकन किया जाता है। क्योंकि सम्पत्तियों के मूल्यों में वृद्धि होने तथा दायित्वों के मूल्यों में कमी होने पर लाभ होता है और सम्पत्तियों के मूल्यों में कमी होने तथा दायित्वों के मूल्यों में वृद्धि होने पर हानि होती है । लाभ होने पर पुराने साझेदार नये को नहीं देना चाहते हैं तथा हानि होने पर नया साझेदार उसे वहन नहीं करना चाहता है। इसलिए पुनर्मूल्यांकन के लाभ/हानि को पुराने साझेदारों में बाँटने के लिए। लाभ-हानि समायोजन खाता या पुनर्मूल्यांकन खाता बनाया जाता है।

Accountancy Class 12 RBSE प्रश्न 3.

ख्याति के मूल्य की गणना गत पाँच वर्षों के औसत लाभ के 3 वर्षों के क्रय के आधार पर की जाती है। लाभ इस प्रकार से है- Rs 30,000, Rs 25,000, Rs 40,000, Rs 35,000,Rs 20,000 फर्म की ख्याति की गणना कीजिए।

Goodwill of the firm is valued at three year’s purchase of average profits of last five years. The firm earned the following profits during last five years : Rs 30,000, Rs 25,000, Rs 40,000, Rs 35,000, Rs 20,000.

उत्तर-

Average Profit = \(\frac { 30,000+25,000+40,000+35,000+20,000 }{ 5 }\)

= \(\frac { 1,50,000 }{ 5 }\) = 30,000

Goodwill = Average Profit x No. of Years Purchased

= 30,000 x 3 = Rs 90,000

![]()

RBSE 12th Accountancy Book Pdf प्रश्न 4.

एक फर्म की ख्याति गत चार वर्षों के औसत लाभ के दो वर्षीय क्रय के आधार पर की जाती है।

फर्म की ख्याति की गणना कीजिए।

Goodwill of the firm is valued at two year’s purchase of average profits of last four years. The firm earned the following profits during last four years : 2013- Rs 10,000, 2014 Rs 16,000, 2015- RS 6,000 (Loss), 2016- Rs 12,000. Calculate the value of goodwill of the firm.

हल:

Average Profit = \(\frac { 10,000+16,000-6,000+12,000 }{ 4 }\)

= \(\frac { 32,000 }{ 4 }\)

= Rs 8,000

Goodwill = 8,000 x 2 = Rs 16,000

RBSE Solutions For Class 12 Accountancy Chapter 1 In Hindi प्रश्न 5.

एक फर्म के फ्छिले 4 वर्षों के लाभ-हानि निम्न थे

2013 – Rs 20,000 – (सट्टे के लाभ Rs 4,000 शामिल)

2014 – Rs (2,000) – (असामान्य हानि चार्ज की गयी Rs 16,000)

2015 – Rs 17,000 – (अन्तिम स्टॉक का मूल्यांकन Rs 2,000 से अधिक किया गया)

2016 – Rs 19,000 – (मशीन विक्रय के लाभ Rs 2,000 शामिल)

औसत लाभों के तीन गुने के आधार पर ख्याति की गणना करें।

Profits of the firm for last four years—

2013 – Rs 20,000 (including Rs 4,000 speculative profits)

2014 – Loss Rs 2,000 (after charging on abnormal loss of Rs 16,000)

2015 – Rs 17,000 (Closing stock overvalued by Rs 2,000)

2016 – Rs 19,000 (including profit on sale of machine Rs 2,000)

Goodwill of the firm is valued three times of average profits of last four years.

उत्तर

Average Profit = \(\frac { 16,000+14,000+17,000+17,000 }{ 4 }\)

= \(\frac { 64,000 }{ 4 }\)

= 16,000

Goodwill = 16,000 x 3 = 48,000

![]()

RBSEsolution.Com Class 12 प्रश्न 6.

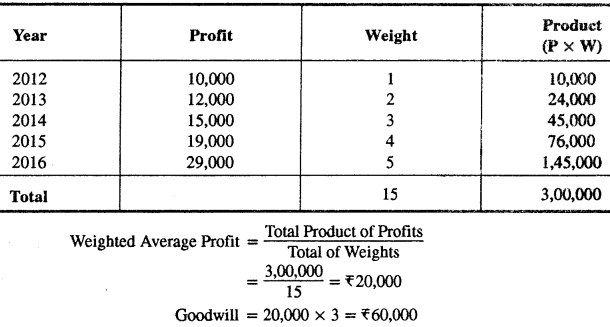

एक फर्म के गत पाँच वर्षों के लाभ इस प्रकार हैं

ख्याति का मूल्य भारित औसत लाभ के 3 वर्षों के क्रय के आधार पर कीजिये।

Profits of the firm for last five years :

Calculate value of goodwill on the basis of three years purchase of weighted average profits.

हल :

RBSE Solution Class 12 प्रश्न 7.

एक फर्म की पूँजी Rs 2,00,000 है वे औसत लाभर Rs 30,000 सामान्य प्रत्याय दर 10% है । ख्याति का मूल्य अधिलाभों के तीन वर्षों के क्रय के आधार पर ज्ञात कीजिये।

Capital of the firm is Rs 2,00,000. Normal Rate of Return is 10% and average profit of the firm is Rs 30,000. Goodwill is to be valued at three years purchase of super profits.

हलः

Normal Profit = Capital Employed x Normal Rate of Return

= 2,00,000 x \(\frac { 10 }{ 100 }\) = 20,000

Average Profit = 30,000

Super Profit = Average Profit – Normal Profit

Super Profit = 30,000 – 20,000 = Rs 10,000

Goodwill = Super Profit x No. of Year’s Purchase

= 10,000 x 3 = Rs 30,000

![]()

RBSE 12th Class Solution प्रश्न 8.

एक फर्म की पूँजी Rs 1,80,000 है व औसत लाभर Rs 24,000 हैं । सामान्य प्रत्याय दर 12% मानते हुए पूँजीकरण विधि से ख्याति का मूल्य ज्ञात कीजिये।

Capital of the firm is Rs 1,80,000 and average profit of the firm is Rs 24,000. Normal Rate of Return is 12% Calculate value of goodwill by capitalization method.

हल:

Capitalization of Average Profit

Goodwill = Capitalized Value of Profits – Capital Employed

= 2,00,000 – 1,80,000 = Rs 20,000

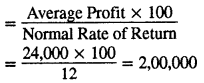

RBSE Solutions Class 12 Accountancy प्रश्न 9.

A व B एक फर्म में साझेदार हैं। फर्म की विनियोजित पूँजी Rs 5,00,000 है और सामान्य प्रत्याय की दर 10% वार्षिक है। प्रत्येक साझेदार का वार्षिक वेतन Rs 8,000 है । औसत लाभ Rs 80,000 हैं। अधिलाभों के पूँजीकरण के आधार पर ख्याति की गणना करो।

A & B are partners in a firm. Capital employed of the firm is Rs 5,00,000. Normal Rate of Return is 10% and Salary of each partner is Rs 8,000 p.a. average profit of the firm is Rs 80,000. Calculate value of goodwill according to capitalization of super profit method.

हले:

Average Profit = 80,000

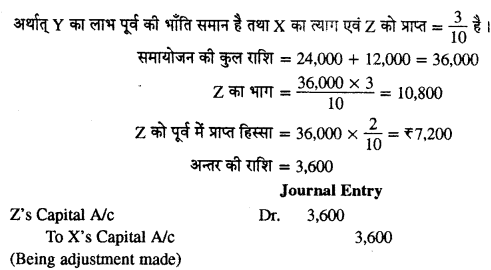

Tyag Anupat Ko Samjhaiye प्रश्न 10.

X व Y की समायोजित पूँजी क्रमशः Rs 30,000 व Rs 25,000 हैं।Z जो लाभों में 1/4 हिस्से के लिए Rs 25,000 पूँजी लाता है। ख्याति की गणना कीजिये।

Adjusted capital of X and Y is 30,000 and Rs 25,000 respectively. Z bring in Rs 25,000 as capital for 1/4 share of profits in the firm. Calculate value of goodwill.

हल :

Z की पूँजी के आधार परफर्म की कुल पूँजी = \(\frac { 25,000X4 }{ 1 }\) = Rs 1,00,000

फर्म की ख्याति = कुल पूँजी – पुराने साझेदारों की समायोजित पूँजी – Z की पूँजी

= 1,00,000 – 55,000 – 25,000

= 1,00,000 – 80,000 = 20,000

![]()

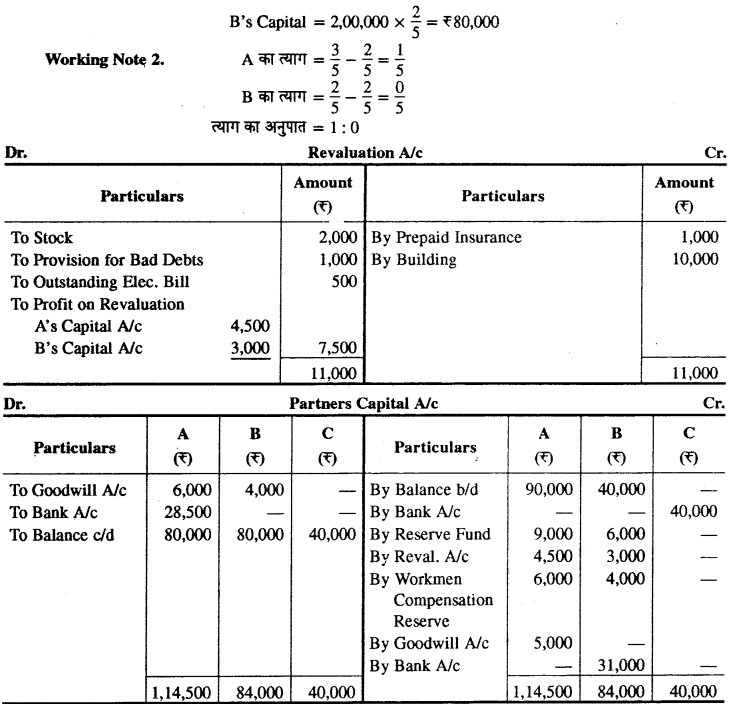

प्रश्न 11.

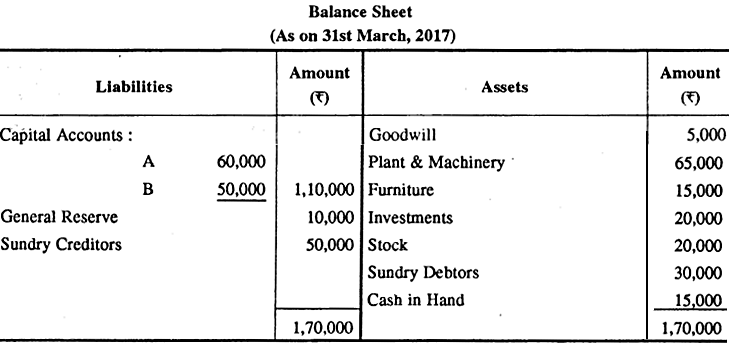

31.12.2016 को समाप्त होने वाले वर्ष के चिट्टे में A व B की पूँजी क्रमशः Rs 40,000 वर Rs 30,000 है तथा सामान्य संचय में Rs 20,000 का शेष है। C लाभों में 1/3 हिस्से के लिए 1.1.17 को प्रवेश करता है और पूँजी Rs 50,000 लेकर आता है । ख्याति की गणना कीजिये ।

Balance of Capital A/cs of A & B were Rs 40,000 & 30,000 respectively. For the year ended 31.12.2016. Balance of General Reserve Stood at Rs 20,000. C is admitted on 1.01.2017 for 1/3rd share in profits. C brings in Rs 50,000 for his share of capital. Calculate value of goodwill.

हल :

पुराने साझेदारों की समायोजित पूँजी = 40,000 + 30,000 + 20,000 (सामान्य संचय)

= Rs 90,000

C की पूँजी के आधार पर फर्म की कुल पूँजी = \(\frac { 50,000X3 }{ 1 }\) = 1,50,000

ख्याति = 1,50,000 – 90,000 – 50,000

= Rs 10,000

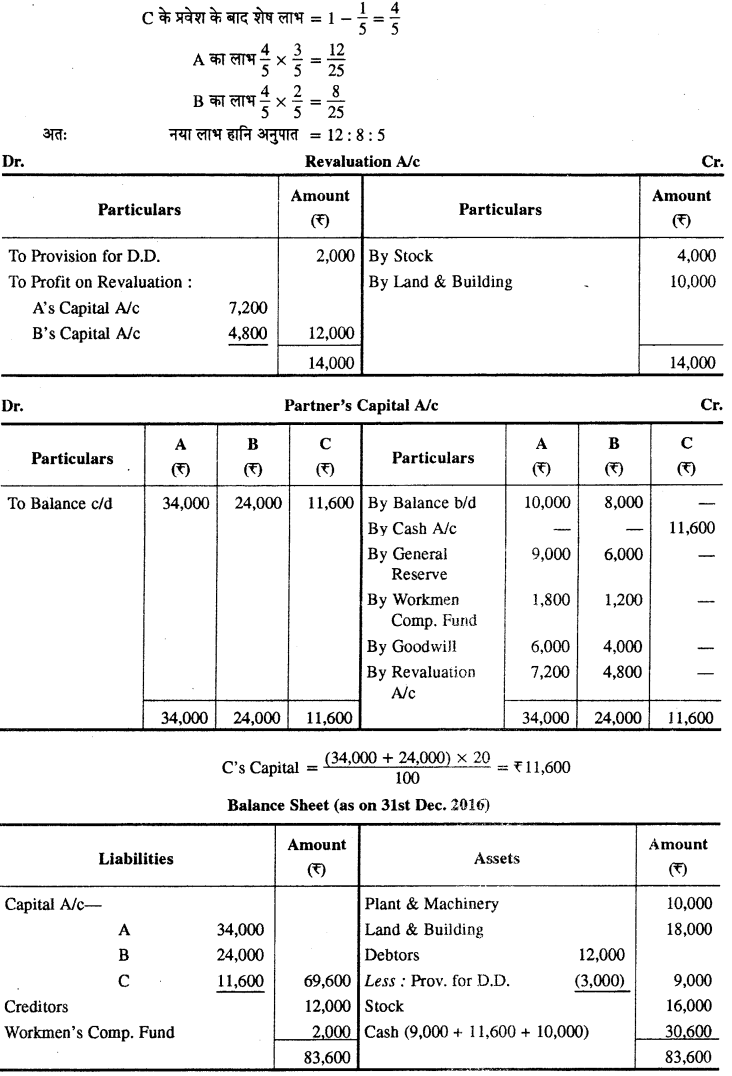

प्रश्न 12.

किसी फर्म के अधिलाभ के Rs 10,000 हैं। यदि 5 वर्ष के लिए 10% ब्याज दर पर एक रुपये की वार्षिकी का वर्तमान मूल्य 3.791 है तो ख्याति का मूल्य होगा।

Super profit of a firm is Rs 10,000. The present value of an annuity of Rs 1 for five years at 10% per annum may taken at 3.791. Find the value of goodwill of the firm.

हुल:

Goodwill = Super Profit x Present Value of Annuity

= 10,000 x 3:791 = Rs 37,910

प्रश्न 13.

किसी व्यवसाय का क्रय प्रतिफल Rs 3,50,000 तय हुआ। इस व्यवसाय की सम्पत्तियाँ Rs 4,00,000 वे दायित्व Rs 80,000 है तो ख्याति का मूल्य होगा।

Purchase consideration of a business is determined at Rs 3,50,000. Assets were Rs 4,00,000 & liabilities were worth Rs 80,000. Find the value of goodwill of the firm.

हले-

Net Asset = Assets – Liabilities

= 4,00,000 – 80,000

= Rs 3,20,000

Goodwill = Purchase Consideration – Net Assets

= 3,50,000 – 3,20,000 = Rs 30,000

![]()

प्रश्न 14.

A व B एक फर्म में 2:1 के अनुपात में लाभों को बाँटते हुए साझेदार हैं। वे C को लाभों का 1/6 हिस्सा देकर प्रवेश देते हैं। C Rs 40,000, पूँजी वर Rs 15,000 ख्याति के लिए नकद लेकर आता है। A व B ख्याति की राशि निकाल लेते हैं। C के प्रवेश की तिथि को पुस्तकों में ख्याति खाता Rs 30,000 पर प्रकट होता है । आवश्यक प्रविष्टियाँ कीजिए।

A and B are partners in a firm sharing profits in the ratio of 2: 1. They admitted C as a new partner. C brought in Rs 40,000 for his share of capital and Rs 15,000 as Goodwill for 1/6th share in profits of the firm. Goodwill withdrawn by A & B from the firm. On C’s admission goodwill appeared in the books of the firm at Rs 30,000. Record necessary Journal entries.

हलेः

![]()

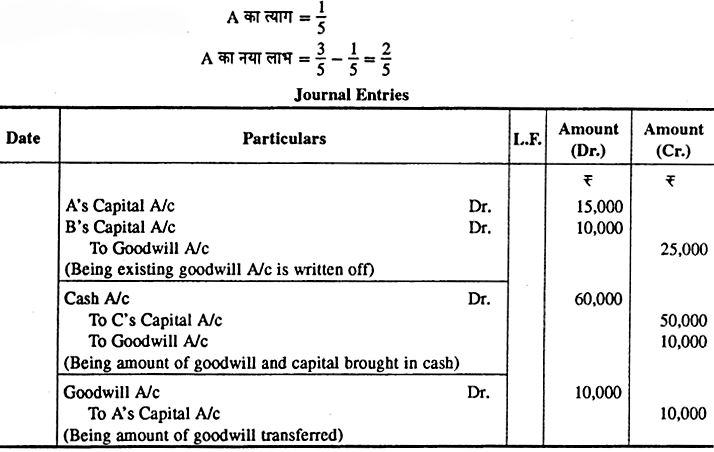

प्रश्न 15.

A व B एक साझेदारी फर्म में 3:2 में लाभ विभाजन करते हैं। वे C को लाभों का 1/5 हिस्से के लिए प्रवेश देते हैं। C अपना पूरा हिस्सा A से प्राप्त करता है। C Rs 50,000 पूँजी वर Rs 10,000 ख्याति के लिए नकद लेकर आता ह।C के प्रवेश की तिथि को पुस्तकों में ख्याति खातार Rs 25,000 पर बताया गया है। आवश्यक प्रविष्टियाँ कीजिए।

A and B are partners in a firm sharing profits in the ratio of 3 : 2. They admitted C as a new partner for 1/5th share in profits of the firm. C acquires his entire share from A. C brought in Rs 50,000 as his capital and Rs 10,000 as goodwill. On C’s admission goodwill appeared in the books of the firm at Rs 25,000. Record necessary Journal entries.

हले:

प्रश्न 16.

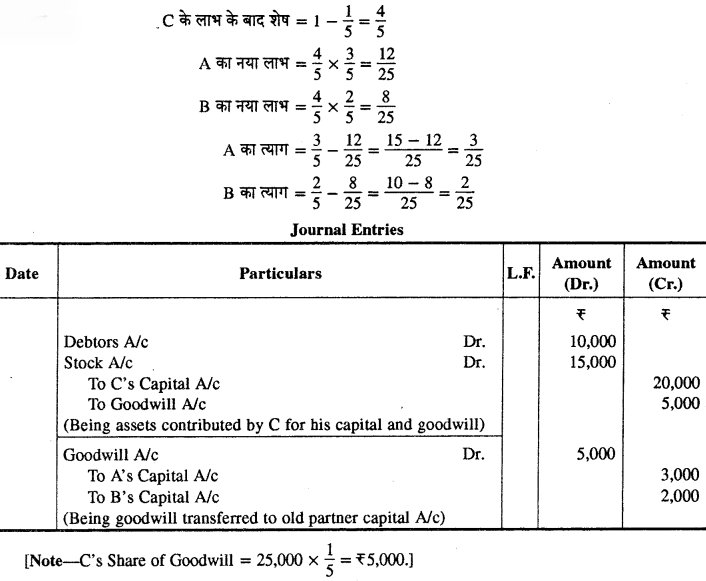

A व B 3:2 के अनुपात में लाभ विभाजन करते हुए साझेदार हैं ये C को लाभों का 1/5 हिस्से के लिए प्रवेश देते हैं। C के प्रवेश की तिथि को फर्म की ख्याति Rs 25,000 पर मूल्यांकित की जाती है । C ने अपनी पूँजी व ख्याति के लिए निम्न सम्पत्तियों का योगदान दिया। देनदार Rs 10,000, स्टॉक Rs 15,000 उपर्युक्त को प्रभावी करने के लिए आवश्यक प्रविष्टियाँ कीजिए।

A and B are partners in a firm sharing profits in the ratio of 3 : 2. They admitted C as a new partner for 1/5th share in profits of the firm. On the date of C’s admission goodwill was valued at Rs 25,000.C contributed the following assets to his capital and his share of goodwill. Debtors Rs 10,000 & Stock Rs 15,000. Record necessary Journal entries.

हले :

![]()

प्रश्न 17.

A, B व C एक फर्म में 3:2:1 के अनुपात में लाभ विभाजन करते हुए साझेदार हैं। वे D को लाभों में \(\frac { 1 }{ 7 }\) हिस्से के लिए प्रवेश देते हैं। D पूँजी के लिए Rs 1,00,000 वर Rs 45,000 ख्याति के लिए लेकर आता है। आवश्यक प्रविष्टियाँ दीजिए।

A, B and C are partners in a firm sharing profits in the ratio of 3 : 2 : 1. They admitted D as new partner for 1/7th share in profits of the firm. D brought in Rs 1,00,000 as his capital and Rs 45,000 as goodwill. Record necessary Journal entries.

हल:

Note-इस स्थिति में पुराना लाभ विभाजन अनुपात तथा त्याग अनुपात समान होगा।

Cash A/C – Dr. 1,45,000

To D’s Capital A/C – 1,00,000

To Goodwill A/C – 45,000

(Being amount of capital out goodwill brought in cash)

Goodwill A/C – Dr. 45,000

To A’s Capital A/c – 22,500

To B’s Capital A/c – 15,000

To C’s Capital A/c – 7,500

(Being goodwill transferred to old partners capital a/c)

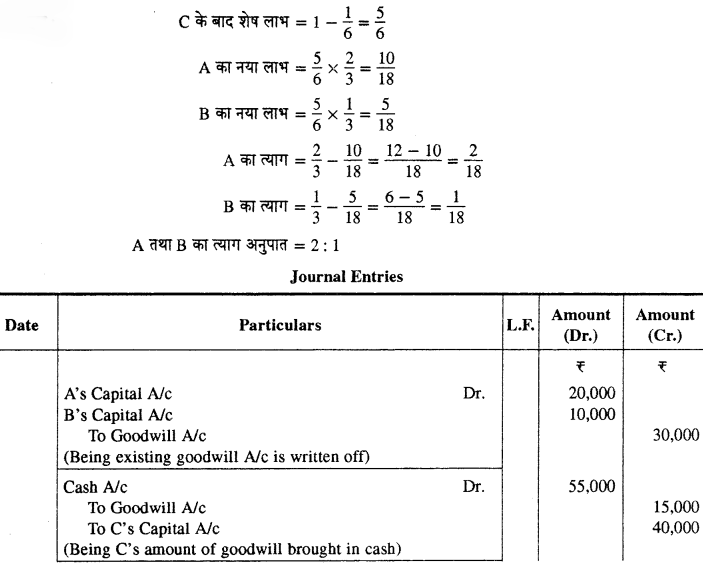

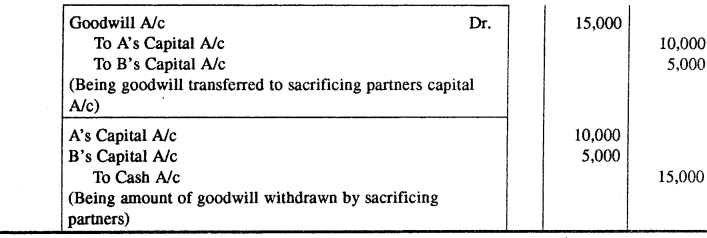

प्रश्न 18.

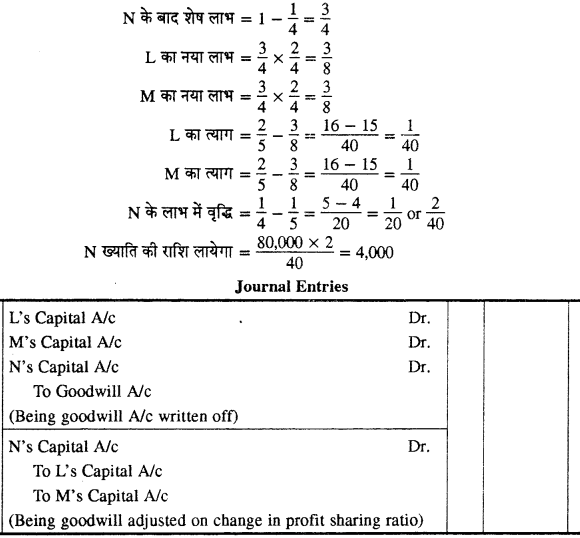

L, M तथा N एक फर्म में साझेदार हैं और लाभ को 2:2:1 के अनुपात में बाँटते हैं। वे निर्णय लेते हैं कि भविष्य में N को लाभों में 1/4 हिस्सा मिलेगा । फर्म की ख्याति का मूल्यांकन के Rs 80,000 किया गया था। पुस्तकों में ख्याति Rs 20,000 दिखाई गई है। जर्नल में अपेक्षित प्रविष्टियाँ कीजिए।

L, M and N are partners in a firm sharing profits in the ratio of 2 : 2 : 1. They decided that N will get 1/4th share in future profit. Goodwill of the firm was valued Rs 80,000. Goodwill already appeared in the books Rs 20,000. Pass necessary journal entries.

हल :

![]()

प्रश्न 19.

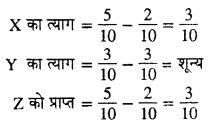

एक्स, वाई तथा जैड साझेदार थे और लाभ को 5 : 3 : 2 के अनुपात में बाँटते थे। उन्होंने निर्णय लिया कि 1.04.2017 से लाभों का बँटवारा 2: 3:5 के अनुपात में करेंगे। वे निम्नलिखित के प्रभाव को उनके पुस्तक मूल्य को बदले बिना दिखाना चाहते हैं।

- लाभ तथा हानि खाता Rs 24,000;

- विज्ञापन उचन्ती खातार Rs 12,000; अपेक्षित समायोजन प्रविष्टि कीजिए।

X, Y and Z were partners sharing profits in the ratio of 5: 3:2. They decided to share future profits in the ratio of 2 :3 : 5 with effect from 1.04.2017. They decide to record the effect of the following without affecting their book value.

- Profit and Loss A/c Rs 24,000,

- Advertisement Suspense A/c Rs 12,000. Pass the necessary adjustment entry.।

हले :

RBSE Class 12 Accountancy Chapter 2 निबन्धात्मक प्रश्न

प्रश्न 1.

नये साझेदार के प्रवेश से क्या समझते हैं ? ख्याति की गणना की विभिन्न विधियों को उदाहरण सहित समझाइये।

उत्तर-

नये साझेदार का प्रवेश (Admission of a New Partner)

नये साझेदार के प्रवेश का अर्थ है साझेदारी के व्यवसाय में नये सदस्य का स्वामी के रूप में प्रवेश करना और साझेदारों की संख्या में वृद्धि होना । नया साझेदार, साझेदार बनने के बाद फर्म द्वारा किये गये समस्त कार्यों के लिए उत्तरदायी हो जाता है परन्तु वह साझेदार बनने से पूर्व के कार्यों के लिए उत्तरदायी नहीं होता है।

ख्याति के मूल्यांकन की विधियाँ (Methods of Valuation of Goodwill)

ख्याति का मूल्य साझेदारी फर्म की उपार्जन क्षमता पर आधारित होने के कारण इसका मूल्यांकन करना एक कठिन कार्य होता है। वास्तव में ख्याति के मूल्यांकन की कोई विशिष्ट विधि नहीं है, परन्तु इसकी अनेक विधियाँ प्रचलित हैं। कब कौन-सी विधि प्रयोग की जाय यह सम्बन्धित दशाओं एवं ख्याति की प्रकृति पर निर्भर करता है। ख्याति के मूल्यांकन की प्रमुख विधियाँ निम्नलिखित हैं

1. वर्षों की क्रय विधि (Year’s Purchase Method)-

जब ख्याति का मूल्यांकन व्यवसाय के लाभों के कुछ वर्षों के गुणा के आधार पर किया जाता है तो इसे वर्षों की क्रय विधि कहते हैं। इस विधि में व्यवसाय के लाभों की गणना दो आधारों पर की जाती है-

- औसत लाभ आधार (Average Profit Base),

- अधिलाभ आधार (Super Profit Method) ।

![]()

(i) औसत लाभ अथार-(अ) सरल औसत लाभ (Simple Average Profit)-

इस विधि में ख्याति का मूल्यांकन पिछले कुछ वर्षों के औसत लाभों (हानियों सहित) के आधार पर किया जाता है । औसत लाभों की गणना करते समय पिछले वर्षों के लाभों में निम्न समायोजन कर लेने चाहिए

- सम्बन्धित वर्ष की आय में से असामान्य लाभ/आय को घटा देना चाहिए।

- सम्बन्धित वर्ष की आय में असामान्य हानि/व्यय को जोड़ देना चाहिए।

- सम्बन्धित वर्ष की आय में से गैर-व्यापारिक विनियोगों पर प्राप्त आय को घटा देना चाहिए।

वास्तविक औसत लाभ (Actual Average Profit) = औसत लाभ – साझेदारों को पारिश्रमिक

ख्याति = वास्तविक औसत लाभ x वर्षों के क्रय की संख्या

Goodwill = Actual Average Profit x No. of Years Purchase

उदाहरण-

फ्छिले पाँच वर्षों के औसत लाभ के आधार पर चार वर्षों के क्रय मूल्य पर ख्याति की गणना कीजिए। पिछले पाँच वर्षों के लाभ क्रमशः Rs 40,000, Rs 50,000, Rs 60,000,Rs 50,000 तथा Rs 60,000 थे।

Calculate the amount of goodwill at four year’s purchase of the last five year’s average profit. The profits of the last five year were Rs 40,000, Rs 50,000, Rs 60,000, Rs 50,000 and Rs 60,000 respectively.

हल :

(a) Total Profits for five years = 40,000 + 50,000 + 60,000 + 50,000 + 60,000 Rs

= Rs 2,60,000

Now

(ब) भारित औसत लाभ (Weighted Average Profit) – जब संस्था के लाभ लगातार बढ़ रहे हों या लगातार घट रहे हों तब भारित औसत लाभ विधि के आधार पर ख्याति का मूल्यांकन किया जाता है। इस विधि में सबसे पहले प्रत्येक वर्ष के लाभ को सम्बन्धित भारांकों से गुणा करके गुणनफल ज्ञात किया जाता है। इसके बाद भारित औसत लाभ का निर्धारण करने के लिए गुणनफलों के योग को भारित संख्याओं के योग से विभाजित किया जाता है। तत्पश्चात भारित औसत लाभ को स्वीकृत संख्या से गुणा करके ख्याति का मूल्य निर्धारित कर लिया जाता है। अतः इसके लिए निम्नलिखित दो सूत्रों का प्रयोग किया जा सकता है

Weighted Average Profit = \(\frac { Total Products of Profit }{ Total of Weights }\)

Goodwill = Weighted Average Profits x Agreed Number of Years Purchase

![]()

(ii) अधिलाभ आधार (Super Profit Base)-

यदि फर्म का वास्तविक औसत लाभ उसी व्यवसाय को करने वाली अन्य फर्मों के सामान्य लाभ से अधिक हो तो दोनों का अन्तर ही अधिलाभ कहलाता है। इस विधि में जितने वर्षों के क्रय के बराबर ख्याति का मूल्य ज्ञात करने के लिए प्रश्न में कहा जाय उसका गुणा अधिलाभ से करके ख्याति का मूल्यांकन किया जाता है।

अधिलाभ = वास्तविक औसत लाभ – सामान्य लाभ

Super Profit = Actual Average Profit – Normal Profit

![]()

विनियोजित पूँजी = प्रयुक्त सम्पत्तियाँ – बाह्य दायित्व

Capital Employed = Assets Employed – Outside Liabilities

सामान्य प्रत्याय दर = ब्याज की दर + जोखिम तत्व

Normal Rate of Return = Rate of Interest + Risk Factor

ख्याति = अधिलाभ x वर्षों के क्रय की संख्या

Goodwill = Super Profit X No. of Year’s Purchase

2. पूँजीकरण विधि (Capitalization Method)-

इस विधि में व्यवसाय द्वारा अर्जित लाभों को पूँजीकरण करके ख्याति का मूल्य ज्ञात किया जाता है। इसमें ख्याति का मूल्यांकन दो आधारों पर किया जा सकता है

(अ) औसत लाभों की पूँजीकरण विधि

Goodwill = Capitalized Value of Profits – Capital Employed

उदाहरण-

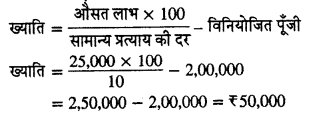

एक फर्म का औसत लाभ Rs 25,000 है और फर्म की पूँजी Rs 2,00,000 है। सामान्य प्रत्याय दर 10 प्रतिशत है। औसत लाभों की पूँजीकरण विधि से ख्याति की गणना कीजिए।

हलेः

(ब) अथिलाभों की पूँजीकरण विधि – इस विधि में सबसे पहले अधिलाभ की गणना की जाती है उसके बाद ख्याति की राशि ज्ञात करने के लिए निम्न सूत्र का प्रयोग किया जाता है

3. छिपी हुई या अनुमानित ख्याति विधि (Hidden Goodwill Method)-

इस विधि में नये साझेदार के लाभ के हिस्से वे उसके द्वारा लाई गई पूँजी के आधार पर फर्म की कुल पूँजी ज्ञात करते हैं।

ख्याति = कुल पूँजी – पुराने साझेदारों की समायोजित पूँजी – नये साझेदार की पूँजी

पुराने साझेदारों की समायोजित की पूँजी = पूँजी शेष + संचय + लाभ – हानि

उदाहरण-

ए तथा बी एक फर्म में साझेदार हैं जिनके पूँजी खातों के शेषर Rs 15,000 वर Rs 25,000 हैं। चिट्टे में अवितरित संचय Rs 10,000 का है। सी को 1/4 हिस्से के लिए फर्म में प्रवेश देते हैं जो Rs 25,000 पूँजी लाता है। उक्त सूचनाओं से ख्याति का मूल्य ज्ञात कीजिए।

हल :

सी की पूँजी के आधार पर फर्म की कुल पूँजी = \(\frac { 25,000\times 4 }{ 1 }\) = Rs 1,00,000

ए व बी की समायोजित पूँजी = (15,000 + 5,000) + (25,000 + 5,000) = 50,000

सी की पूँजी = 25,000

फर्म की ख्याति = 1,00,000 – 50,000 – 25,000 = Rs 25,000

![]()

4. क्रय प्रतिफल विधि (Purchased Consideration Method)-

इस विधि के अन्तर्गत व्यापार को क्रय करते समय क्रय प्रतिफल का, सम्पत्तियों में से दायित्वों को घटाकर आने वाली शुद्ध सम्पत्तियों पर आधिक्य ही ख्याति का मूल्य माना जाता है। सूत्र रूप में

ख्याति = क्रय प्रतिफल – शुद्ध सम्पत्तियाँ

Goodwill = Purchase Consideration – Net Assets

Net Assets = Assets – Liabilities

उदाहरण-एक व्यवसाय की सम्पत्तियाँ Rs 3,00,000 वे दायित्व Rs 75,000 के हैं। व्यवसाय का क्रय प्रतिफल Rs 2,60,000 तय हुआ तो ख्याति का मूल्य कितना होगा ?

हल:

Net Assets = Assets – Liabilities

= 3,00,000 – 75,000 = Rs 2,25,000

Goodwill = Purchase Consideration – Net Assets

= 2,60,000 – 2,25,000 = Rs 35,000

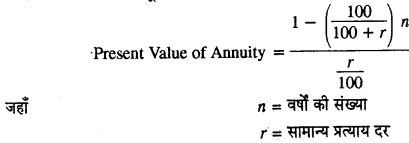

5. वार्षिकी विधि (Annuity Method)-

इस विधि के अन्तर्गत ख्याति का मूल्य भविष्य में उपार्जित किये जाने वाले अधिलाभ के वर्तमान मूल्य के बराबर माना जाता है। भावी अधिलाभों के वर्तमान मूल्य की गणना वार्षिकी तालिकाओं के आधार पर की जाती है। इस तालिका में एक से की वार्षिकी विभिन्न वर्षों के लिए विभिन्न ब्याज दरों के आधार पर दी हुई होती है जिसे अधिलाभ की राशि से गुणा करके ख्याति का मूल्यांकन किया जाता है।

Goodwill = Super Profit x Present Value of Annuity

यदि वार्षिकी का वर्तमान मूल्य ने दिया गया हो तो उसकी गणना निम्न सूत्र से कर ली जाती है

उदाहरण-

औसत लाभ = Rs 40,000, विनियोजित पूँजी = Rs 2,00,000, सामान्य प्रत्याय की दर = 10%, वर्तमान मूल्य = 2:487 वार्षिकी विधि से ख्याति का मूल्य ज्ञात कीजिए।

हल:

Normal Profit = Capital Employed x N.R.R.

= \(\frac { 2,00,000\times 10 }{ 100 }\)

= Rs 20,000

S.P. = AP – NP = 40,000 – 20,000

= 20,000

Goodwill = 20,000 x 2:487

= 49,740

प्रश्न 2.

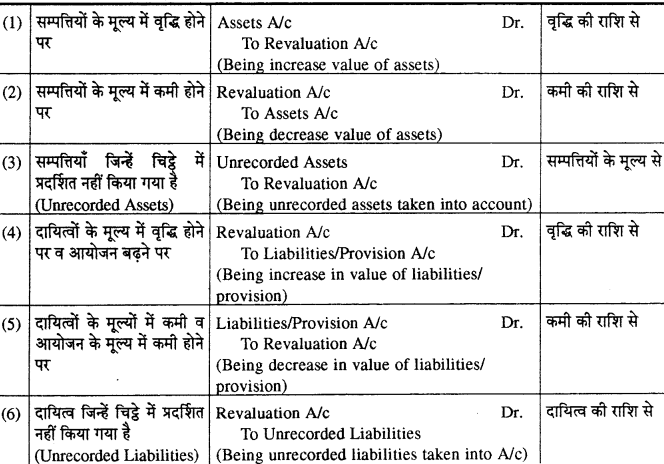

पुनर्मूल्यांकन खाता क्या है ? यह क्यों बनाया जाता है ? एक नये साझेदार के प्रवेश के समय सम्पत्तियों के पुनर्मूल्यांकन एवं दायित्वों के पुनः निर्धारण से सम्बन्धित जर्नल प्रविष्टियाँ दीजिये।

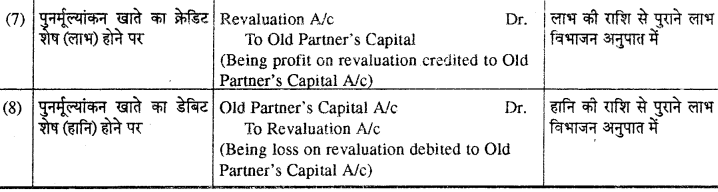

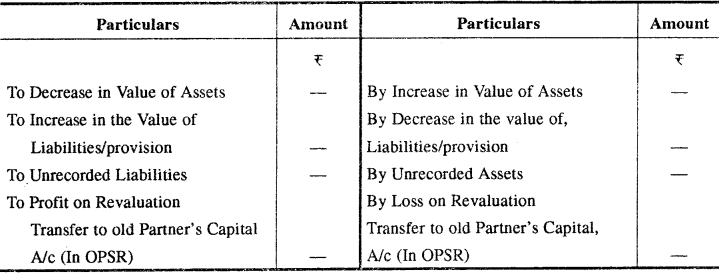

उत्तर-

सम्पत्तियों का पुनर्मूल्यांकन व दायित्वों का पुनः निर्धारण (Revaluation of Assets and Reassessment of Liabilities)

नये साझेदार के प्रवेश के समय सम्पत्तियों व दायित्वों को नये मूल्य पर दिखाने के लिए उनका पुनर्मूल्यांकन किया जाता है। क्योंकि सम्पत्तियों के मूल्यों में वृद्धि होने व दायित्वों के मूल्यों में कमी होने पर लाभ होता है और सम्पत्तियों के मूल्य में कमी होने व दायित्वों के मूल्य में वृद्धि होने पर हानि होती हैं। लाभ होने पर पुराने साझेदार नये को नहीं देना चाहेंगे। उसी प्रकार हानि होने पर नया साझेदार उसे वहन नहीं करना चाहेगा । इसलिए पुनर्मूल्यांकन के लाभ-हानि को पुराने साझेदारों में पुराने लाभ विभाजन अनुपात में बाँट दिया जाता है। इस स्थिति में एक विशेष खाता खोला जाता है, जिसे पुनर्मूल्यांकन खाता (Revaluation Account) या लाभ-हानि समायोजन खाता (P & L Adjustment A/c) कहते हैं। इस खाते की प्रकृति अवास्तविक खाते की होती है।

![]()

पुनर्मूल्यांकन खाते के लिए जर्नल प्रविष्टियाँ

पुनर्मूल्यांकन खाते का प्रारूप (Format of Revaluation Account)

Dr. Revaluation/P & L Adjustment Account

प्रश्न 3.

एक नये साझेदार के प्रवेश के समय कौन-सी समस्याएँ आती हैं ? उनके समाधान हेतु कौन-कौन से समायोजन किये जाते हैं ? वर्णन कीजिए।

What problems occur at the time of admission of a new partner, for which what adjustments are made ?

उत्तर-

साझेदारी फर्म में एक नये साझेदार के प्रवेश के समय विभिन्न समस्याएँ आती हैं, जैसे—नया लाभ विभाजन अनुपात क्या होगा ? नये साझेदार के पक्ष में कौन अपने हिस्से के लाभ का त्याग करेगा ? ख्याति का मूल्यांकन कैसे होगा ? सम्पत्तियों का पुनर्मूल्यांकन व दायित्वों का पुनर्निर्धारण कैसे होगा ? संचय तथा अवितरित लाभों का समायोजन कैसे होगा ? पूँजी का समायोजन कैसे किया जायेगा ? आदि प्रमुख समस्याएँ हैं। इनके समाधान के लिए निम्नलिखित समायोजन किये जाते हैं

1. नये लाभ विभाजन अनुपात व त्याग अनुपात की गणना (Calculation of New Profit Sharing Ratio & Sacrificing Ratio)-

नया साझेदार अपने लाभ का हिस्सा पुराने साझेदारों से प्राप्त करता है, इस कारण उनका लाभ विभाजन अनुपात परिवर्तित हो जाता है। अतः नये लाभ विभाजन अनुपात की गणना की जाती है। नये साझेदार के प्रवेश पर पुराने साझेदार अपने लाभ के हिस्से का जिस अनुपात में त्याग करते हैं उसे त्याग अनुपात कहते हैं।

त्याग अनुपात = पुराना लाभ विभाजन अनुपात – नया लाभ विभाजन अनुपात

नया लाभ विभाजन अनुपात = पुराना लाभ विभाजन अनुपात – त्याग अनुपात

नये लाभ विभाजन अनुपात व त्याग अनुपात की गणना करने की विभिन्न परिस्थितियाँ निम्नलिखित हो सकती हैं

- जब प्रश्न में केवल नये साझेदार का अनुपात दिया गया हो ।

- जब नया साझेदार पुराने साझेदारों से समान अनुपात में अपना हिस्सा प्राप्त कर रहा हो ।

- जब नया साझेदार अपना हिस्सा असमान अनुपात में प्राप्त करता है।

- जब नया साझेदार अपना हिस्सा पूर्णतया किसी एक साझेदार से प्राप्त करता है।

- जब नया साझेदार अपना हिस्सा पुराने साझेदारों से एक निश्चित अनुपात में प्राप्त करता है ।।

- जब पुराने साझेदार अपने हिस्से को एक निश्चित भाग नये साझेदार के पक्ष में त्याग करते हैं।

![]()

2. ख्याति से सम्बन्धित समायोजन (Adjustment Related to Goodwill)-

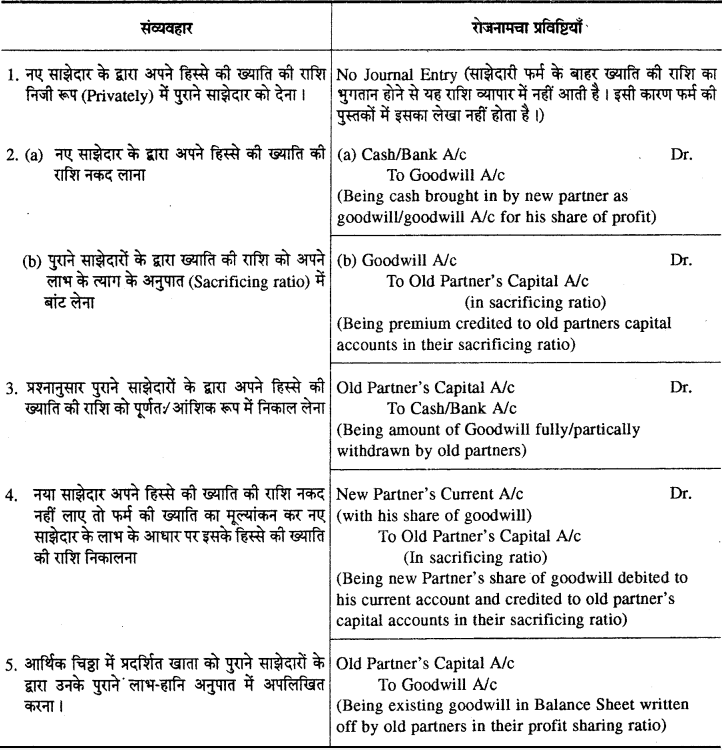

नये साझेदार के प्रवेश पर ख्याति की गणना करके उसके समायोजन से सम्बन्धित या बँटवारे से सम्बन्धित लेखे किये जाते हैं। ख्याति के मूल्यांकन की प्रमुख विधियाँ निम्नलिखित हैं

- वर्षों की क्रय विधि,

- पूँजीकरण विधि,

- छिपी हुई या अनुमानित ख्याति विधि,

- क्रय प्रतिफल विधि,

- वार्षिकी विधि।

ख्याति का लेखांकन व्यवहार – ख्याति का लेखा करने की विभिन्न परिस्थितियाँ निम्नलिखित हो सकती हैं

- जब ख्याति की राशि का भुगतान निजी रूप से किया जाये।

- जब नया साझेदार अपने हिस्से की ख्याति की राशि नकद लेकर आये ।

- जब नया साझेदार ख्याति की राशि नकद न लाये ।।

- जब नया साझेदार अपने हिस्से की ख्याति आंशिक रूप से नकद में लाये।

- जब नया साझेदार सम्पत्ति के रूप में ख्याति लाये ।

सम्पत्तियों तथा दायित्वों का पुनर्मल्यांकन (Revaluation of Assets and Liabilities) –

जब एक नया साझेदार फर्म में प्रवेश करता है तो वह जानना चाहता है कि चिट्टे में दर्शायी गयी सम्पत्तियों व दायित्वों को मूल्य ठीक है या नहीं, इसके लिए सम्पत्ति व दायित्वों का पुनर्मूल्यांकन किया जाता है और इनमें होने वाली कमी व वृद्धि का लेखा पुनर्मूल्यांकन खाते में किया जाता है। यह खाता नाम मात्र का खाता होता है। सम्पत्ति के मूल्यों में कमी तथा दायित्वों में वृद्धि होने से फर्म को हानि होती है तथा सम्पत्तियों में वृद्धि व दायित्वों में कमी होने से फर्म को लाभ होता है ।

यदि पुनर्मूल्यांकन खाते के क्रेडिट पक्ष को योग अधिक है तथा डेबिट पक्ष का योग कम है तो लाभ होगा तथा डेबिट पक्ष को योग अधिक है तथा क्रोडिट पक्ष का योग कम है तो हानि होगी । पुनर्मूल्यांकन खाते में होने वाले लाभ व हानि को पुराने साझेदारों में पुराने अनुपात में बाँट दिया जाता है।

अवितरित संचय एवं लाभ/हानि (Undistributed Reserves and Profit/Loss) –

अवितरित संचय या लाभ/हानि को पुराने साझेदारों के पूँजी खाते में पुराने लाभ-हानि वितरण अनुपात में बाँट दिया जाता है। क्योंकि वह उन्हीं के द्वारा कमाये गये लाभ का भाग होता है।

पूँजी का समायोजन (Adjustment of Capital) –

एक फर्म में नये साझेदार के प्रवेश पर साझेदारों की पूँजी को समायोजन निम्नलिखित तीन प्रकार से किया जा सकता है

1. पुराने साझेदारों की पूँजी को समायोजन नये साझेदार की पूँजी के आधार पर करनी-

जब पुराने साझेदारों की पूँजी का समायोजन नये साझेदारों की पूँजी के आधार पर किया जाता है तो नए साझेदार की पूँजी के अनुसार सबसे पहले पूरी फर्म की पूँजी निकाली जाती है । इसके बाद इसे नये लाभ विभाजन अनुपात में समायोजित कर किया जाता है । इस प्रकार जिन साझेदारों की पूँजी कम या अधिक रहती है वे साझेदार फर्म को पूँजी चुकाकर या फर्म से पूँजी निकालकर बराबर कर लेते हैं। यह समायोजन रोकड़ में किया जा सकता है या साझेदारों के चालू खाते के माध्यम से किया जा सकता है । प्रश्न में यदि कोई सूचना नहीं है तो समायोजन नकद खाते के माध्यम से ही किया जाता है।

2. नये साझेदार की पूँजी का निर्धारण, पुराने साझेदारों की पूँजी के आधार पर करना-

इसके अन्तर्गत पुराने साझेदारों की पूँजी का आशय नये साझेदार के प्रवेश के पश्चात् ख्याति, अवितरित लाभ, पुनर्मूल्यांकन पर लाभ/हानि आदि के समायोजन करने के पश्चात् शेष रही पूँजी से है। इस विधि में पुराने साझेदारों की पूँजी के कुल शेष के आधार पर फर्म की कुल पूँजी ज्ञात करके, नये साझेदार की पूँजी का हिस्सा निकाला जाता है।

3. नयी फर्म की पूँजी दी गयी हो-

यदि प्रश्न में नयी फर्म की पूँजी दी गयी है तो पूँजी का बँटवारा नये अनुपात में होगा। नया साझेदार अपने हिस्से की पूँजी लायेगा । पुराने साझेदार अपनी नयी पूँजी वे समायोजित पूँजी का अन्तर नकद लायेंगे या अधिक होगी तो ले जायेंगे अथवा चालू खातों के माध्यम से अपनी पूँजी को समायोजित कर लेंगे।

![]()

प्रश्न 4.

स्मरणार्थ पुनर्मूल्यांकन खाता क्या है ? यह पुनर्मूल्यांकन खाते से किस प्रकार भिन्न है ?

उत्तर:

स्मरणार्थ पुनर्मूल्यांकन खाता (Memorandum Revaluation Account)

नये साझेदार के प्रवेश पर कभी-कभी साझेदार यह समझौता कर लेते हैं कि सम्पत्तियों एवं दायित्वों का पुनर्मूल्यांकन तो किया जाय परन्तु उनके प्रभाव को खाते में न दर्शाया जाय अर्थात् सम्पत्तियाँ एवं दायित्व पुराने मूल्य पर ही दिखाये जायें। ऐसी स्थिति में स्मरणार्थ पुनर्मूल्यांकन खाता बनाया जाता है । इस खाते को सम्पत्तियों के पुनर्मूल्यांकन में हानि होने पर डेबिट तथा लाभ होने पर क्रेडिट किया जाता है । इस प्रकार इस खाते का शेष लाभ अथवा हानि प्रदर्शित करता है जिसे पुराने साझेदारों के पूँजी खातों में पुराने अनुपात में हस्तान्तरित कर दिया जाता है इसके बाद उसी राशि से सभी साझेदारों के पूँजी खातों में नये अनुपात में विपरीत लेखा कर दिया जाता है। इस सम्बन्ध में निम्न प्रकार प्रविष्टि होती हैं

पुनर्मूल्यांकन पर लाभ की दशा में

Memorandum Revaluation A/c DR.

To Old Partner’s capital A/c

(Profit on revaluation transferred in old ratio)

All Partner’s Capital A/c

To Memorandum Revaluation A/c

(Memorandum Revaluation A/c closed in new ratio)

उपरोक्त दोनों प्रविष्टियों के स्थान पर निम्नांकित एक प्रविष्टि भी की जा सकती है-

All Partner’s Capital A/C Dr.

To Old Partners Capital A/C

(Adjustment of revaluation made)

पुनर्मूल्यांकन पर हानि की दशा में

Old Partner’s Capital A/C Dr.

To Memorandum Revaluation A/C

(Loss on revaluation transferred in old ratio)

Memorandum Revaluation A/C

To All Partner’s Capital A/C Dr.

(Memorandum revaluation A/c closed in new ratio)

उपरोक्त दोनों प्रविष्टियों के स्थान पर निम्नांकित एक प्रविष्टि भी की जा सकती है–

Old Partner’s Capital A/c Dr.

To All Partners Capital A/C

(Adjustment of revaluation made)

स्मरणार्थ पुनर्मूल्यांकन खाता तथा पुनर्मूल्यांकन खाते में अन्तर

प्रश्न 5.

किसी साझेदार के प्रवेश के समय भारतीय AS-26/Indian AS-38 के अनुसार ख्याति का लेखांकन संव्यवहार बतायें।

उत्तर-

लेखी मानक 26/लेखा मानक 38 के अनुसार ख्याति को पुस्तकों में तभी लिखा जाता है जबकि इसको क्रय करने हेतु मुद्रा या मुद्रा के समान अन्य कोई प्रतिफल चुकाया गया हो । अतः केवल क्रय की गई ख्याति का लेखी पुस्तकों में होगा। साझेदार के प्रवेश, अवकाश ग्रहण,मृत्यु अथवा वर्तमान साझेदारों के लाभ विभाजन अनुपात में परिवर्तन होने पर स्वअर्जित ख्याति का लेखा करके उसे साझेदारों के पूँजी खातों/चालू खातों के माध्यम से समायोजित किया जायेगा।

नये साझेदार के प्रवेश पर ख्याति का लेखा (Goodwill Treatment on Admission of New Partner)

लेखा मानक 26 के आधार पर एक साझेदार के प्रवेश के समय ख्याति के सम्बन्ध में निम्न प्रकार लेखे किए जायेंगे-

![]()

RBSE Class 12 Accountancy Chapter 2 आंकिक प्रश्न

प्रश्न 1.

A व B एक फर्म में 3:1 के अनुपात में लाभ विभाजन करते हुए साझेदार हैं। वे C को लाभों का 1/4 हिस्से के लिए प्रवेश देते हैं। C के प्रवेश की तिथि को फर्म की ख्याति Rs 40,000 पर मूल्यांकित की गयी । निम्न परिस्थितियों में ख्याति के लेखांकन हेतु प्रविष्टियाँ दीजिये

(a) C अपने हिस्से की ख्याति निजी तौर पर A व B को देता है।

(b) C अपने हिस्से की ख्याति नकद लेकर आता है।

(c) C अपने हिस्से की ख्याति नकद लेकर आता है A व B अपने हिस्से की 1/2 ख्याति व्यवसाय से निकाल लेते हैं।

(d) C अपने हिस्से की ख्याति में से Rs 6,000 नकद लेकर आता है।

(e) C अपने हिस्से की ख्याति नकद लेकर नहीं आता है।

A & B are partners sharing profits in the ratio of 3 : 1. They admit C for 1/4th share in profits of the firm. Goodwill of the firm is valued at Rs 40,000 on the date of admission of C. Pass Journal Entries in the following cases :

(a) C pays for his share of Goodwill privately to A & B.

(b) C brings his share of goodwill in cash.

(c) C brings his share of goodwill in cash. A & B withdraws half of the goodwill.

(d) C brings Rs 6,000 in cash out of his share of goodwill.

(e) C is unable to bring his share of goodwill in cash.

उत्तर:

A तथा B का त्याग अनुपात = 3:1

A, B तथा C का नया लाभ-हानि अनुपात = 9:3:4

(a) निजी तौर पर ख्याति का हिस्सा देने पर फर्म की पुस्तकों में कोई लेखा नहीं होगा।

(b) (i) Cash A/C Dr. 10,000

To Goodwill A/c 10,000

(Being amount of goodwill brought in cash)

(ii) Goodwill A/c Dr. 10,000

To A’s Capital A/c 7,500

To B’s Capital A/c 2,500

(Being goodwill transferred to sacrificing partners capital a/c)

(c) (i) Cash A/C Dr. 10,000

To Goodwill A/C 10,000

(Being amount of goodwill brought in cash)

(ii) Goodwill A/C Dr. 10,000

To A’s Capital A/C 7,500

To B’s Capital A/C 2,500

(Being goodwill transferred to sacrificing partners capital A/C)

(iii) A’s Capital A/C Dr. 3,750

B’s Capital A/c 1,250

To Cash A/c 5,000

(Being 1/2 amount of goodwill withdrawn by sacrificing partners)

(d) (i) Cash A/C Dr. 6,000

To Goodwill A/C 6,000

(Being amount of goodwill brought in cash)

(ii) Goodwill A/C 6,000

C’s current A/C Dr. 4,000

To A’s Capital A/C 7,500

To B’s Capital A/C 2,500

(Being goodwill transferred to sacrificing partners capital A/C)

![]()

(e) C’s current A/C Dr.

To A’s Capital A/C

To B’s Capital A/C

(Being share of goodwill of new partners is adjusted)

प्रश्न 2.

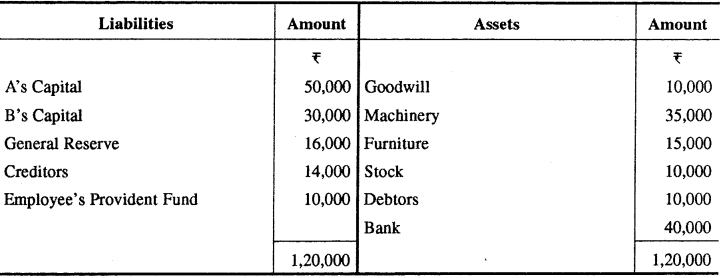

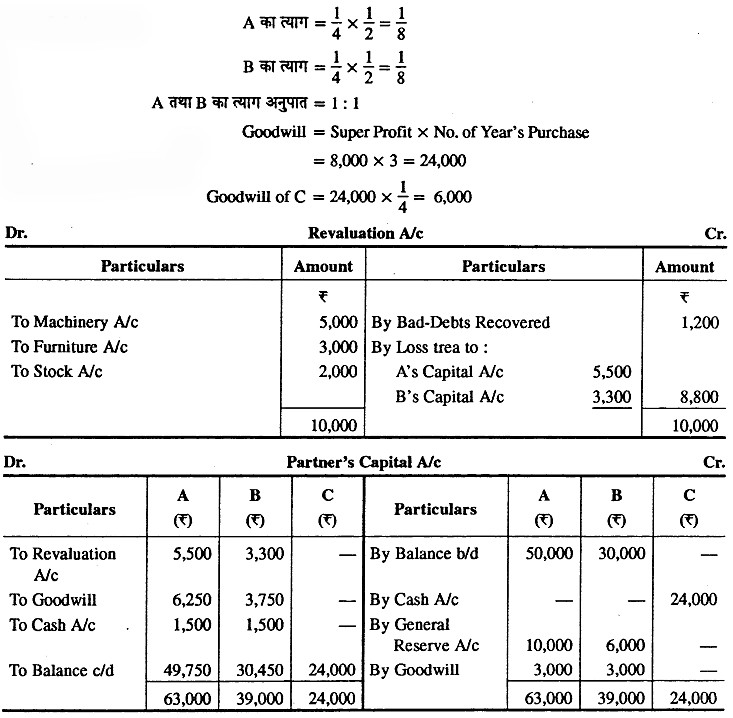

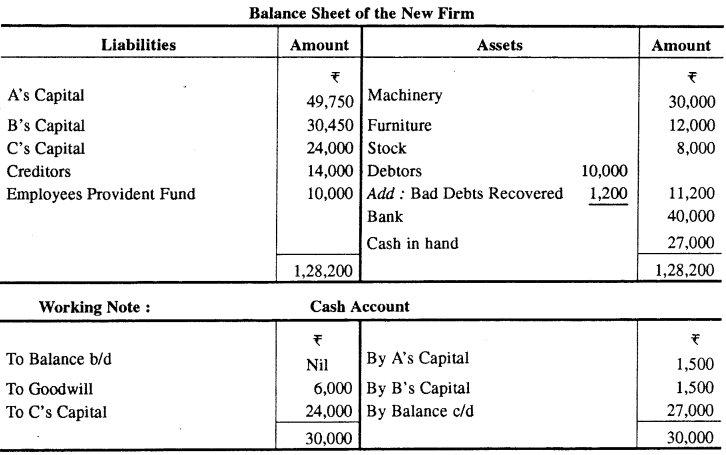

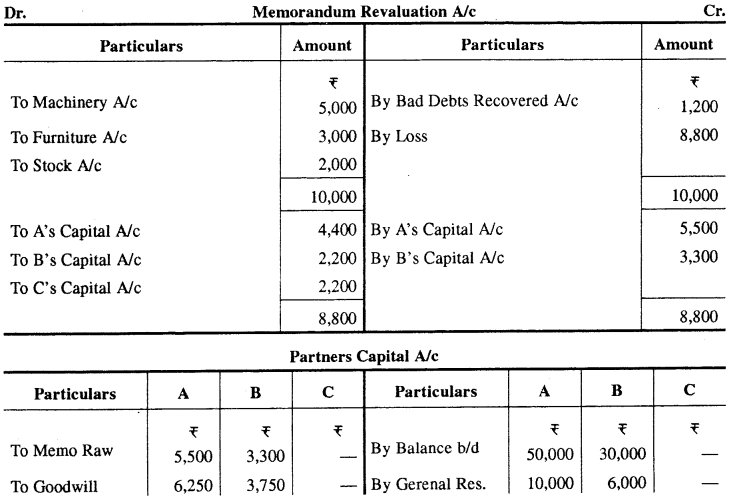

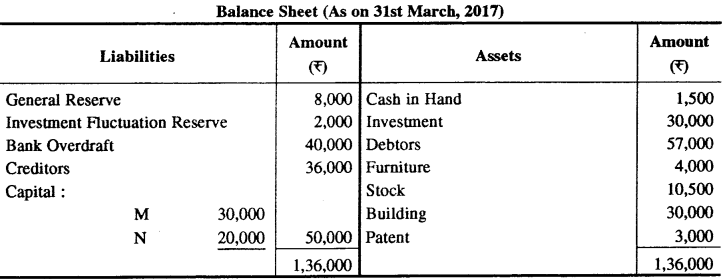

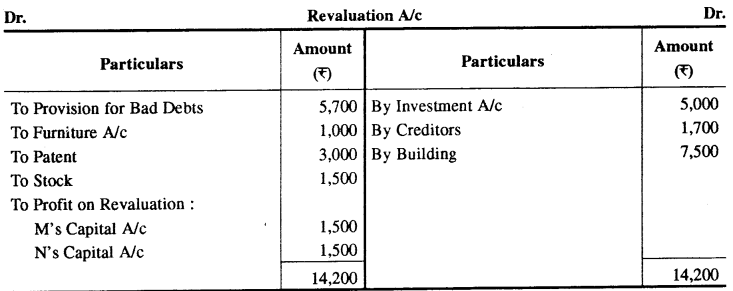

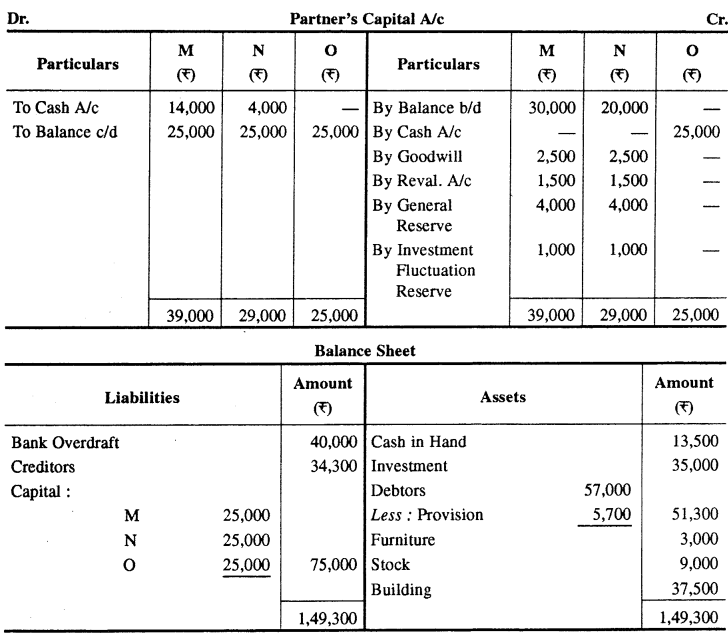

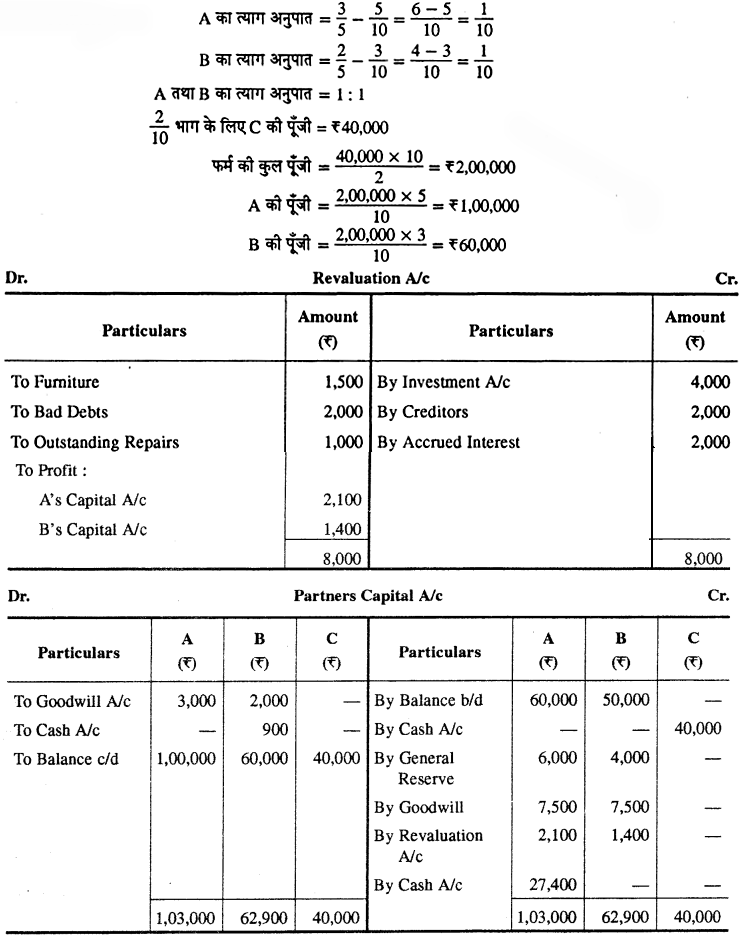

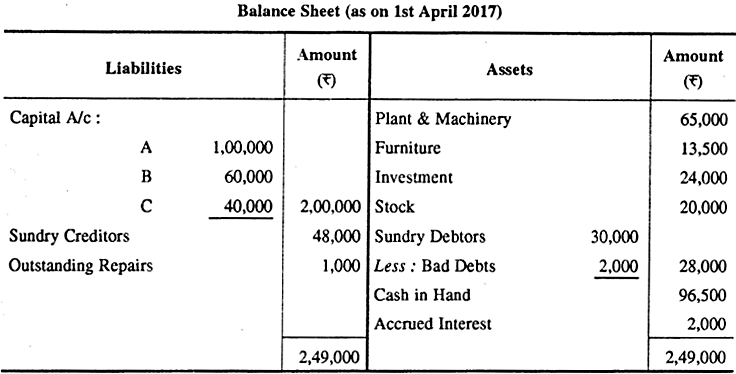

अ और ब एक व्यवसाय के लाभों को 5 : 3 में बाँटते हैं। वे स को लाभ में 104 हिस्से के लिए शामिल करते हैं जो कि अ तथा ब द्वारा बराबर दिया जायेगा । स के प्रवेश के समय फर्म का चिट्ठा निम्न प्रकार था

A and B shares the profits of a business in the ratio of 5:3. They admitted C into the firm for 1/4th share in profits which is to be contributed equally by A and B. On the date of admission of C the Balance Sheet of the firm was as follows:

स के प्रवेश की शर्ते निम्न थीं

- से अपने हिस्से की पूँजी तथा ख्याति के लिये Rs 30,000 लाएगा एवं पुराने साझेदारों द्वारा आधी ख्याति फर्म से निकाल ली। जाएगी ।

- फर्म की ख्याति का मूल्यांकन अधिलाभर Rs 8,000 के तीन वर्षों के क्रय के बराबर किया गया है।

- मशीन, फर्नीचर एवं स्टॉक का पुनर्मूल्यांकन क्रमश Rs 30,000, Rs 12,000 एवं Rs 8,000 पर किया गया है।

- एक ग्राहक जिसका खाता डूबत ऋण मान लिया गया था। वह Rs 1,200 देने के लिए सहमत हो जाता है।

उपरोक्त के आधार पर पुनर्मूल्यांकन खाता साझेदारों के पूँजी खाते तथा नई फर्म का चिट्ठा बनाइए। यदि यह तय किया गया कि सम्पत्तियों व दायित्वों को पुराने मूल्यों पर ही दिखाया जाये तो स्मरणार्थ पुनर्मूल्यांकन खाता पूँजी खते व चिट्ठा बनाइये।।

Terms of C’s admission were as follows :

- C will bring Rs 30,000 for his share of capital and goodwill. Half of the goodwill shall be withdrawn by the old partners.

- Goodwill of the firm has been valued at 3 years purchase of the super profit Rs 8,000.

- Machinery, furniture and stock are revalued at Rs 30,000, Rs 12,000 & Rs 8,000 respectively.

- An old customer whose account was written off as bad debts has promised to pay 1,200. From the above prepare

Revaluation account, Partner’s Capital accounts and Balance Sheet of the new firm. If it has been agreed that Assets and Liabilities are to be shown at old values. Prepare Memorandum Revaluation A/c. Partner’s capital A/c and Balance Sheet.

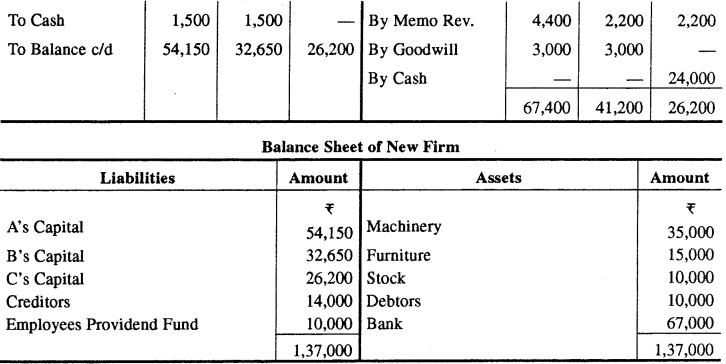

उत्तर:

यदि सम्पत्तियों व दायित्वों के पुराने मूल्य पर ही दिखाया जाय तब निम्न प्रकार खाते बनेंगे

![]()

प्रश्न 3.

एक्स व वाई 2:1 के अनुपात में लाभ बाँटते हुए साझेदार हैं। 31 मार्च, 2017 को उनकी फर्म का चिट्ठा निम्न प्रकार है।

X and Y are partners sharing profit in the ratio of 2 : 1. Their Balance Sheet as on 31st March, 2017 is as under :

1st अप्रैल 2017 को उन्होंने जेड को 1/4 हिस्से के लिए फर्म में प्रवेश दिया जिसे वह एक्स से प्राप्त करेगा। उस समय निम्न निर्णय लिये–

- जेड पूँजी के रूप में Rs 36,000 नकद तथा Rs 14,000 मूल्य के राम लि. के अंश लाता है।

- फर्म की ख्याति का वर्तमान मूल्य Rs 12,000 है। जेड हिस्से की ख्याति नकद लाता है।

- देनदारों पर डूबत ऋण आयोजन 10% तक बढ़ाया जाये तथा अब अदत्त वेतन की आवश्यकता नहीं है।

- संयन्त्र व मशीनरी 5% से अधिमूल्यांकित किया गया है तथा हतियार Rs 2,400 से बढ़ाया जाये।

- भवन का मूल्य 10% से कम मूल्यांकित है।

- Rs 4,000 के लेनदार अपलिखित करने हैं।

- कर्मचारी क्षतिपूर्ति संचय के विरुद्ध Rs 9,000 का दायित्व निश्चित हो गया है।

जेड के प्रवेश पर लाभ-हानि समायोजन खाता साझेदारों के पूँजी खाते एवं चिट्ठा बनाइए।

They admitted Z in the firm from 1st April, 2017 for 1/4th share, which he will receive from X. Following decisions were taken on that time :

- Z brings Rs 36,000 in cash and share of Ram Ltd. Worth Rs 14,000 as his capital.

- The present value of firm’s goodwill is Rs 12,000. Z brings his share of goodwill in cash.

- Provision for Bad Debts on debtors be increased to 10% and outstanding salary is not required now.

- Plant and Machinery overvalued by 5% and stock to be increased by Rs 2,400.

- Building undervalued by 10%.

- Sundry Creditors were written back by Rs 4,000.

- Liability against Workmen Compensation determined at Rs 9,000.

Prepare Profit & Loss Adjustment Account, Partners Capital Accounts and Balance Sheet on the admission of Z.

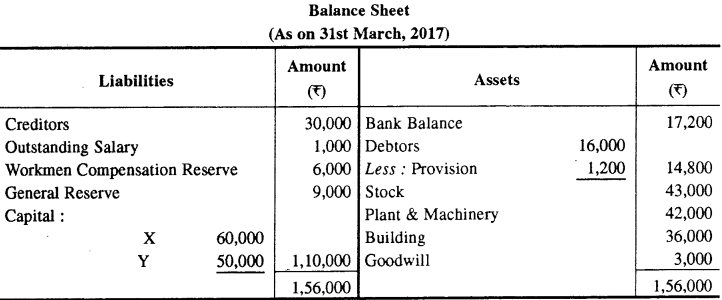

उत्तर:

Dr. P & L Adjustment A/C Cr.

![]()

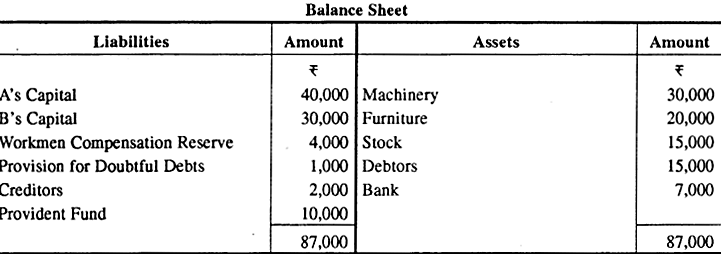

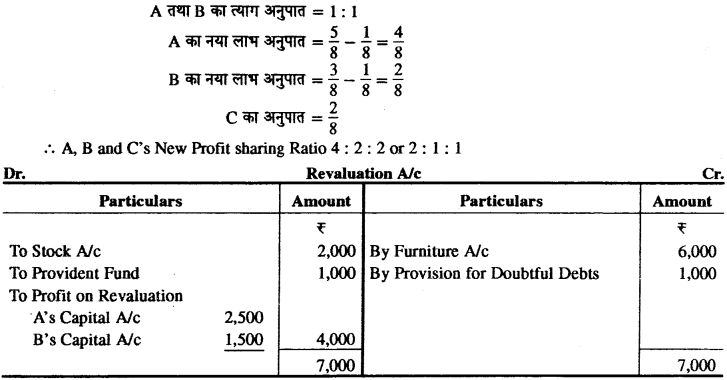

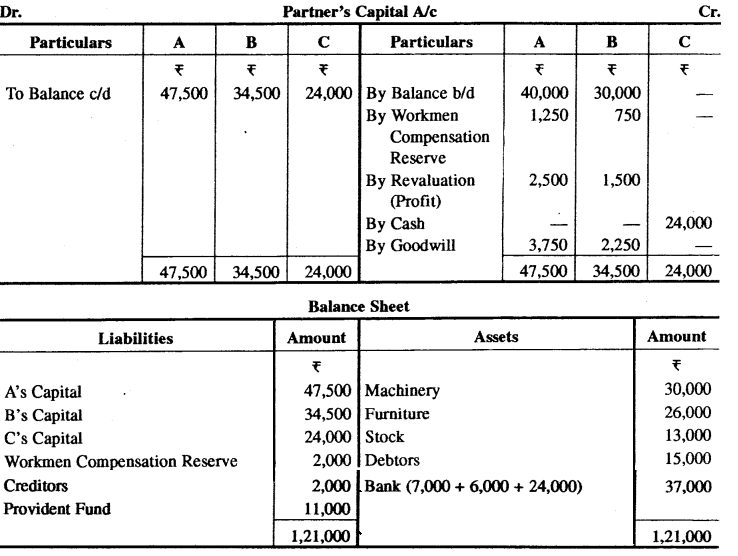

प्रश्न 4.

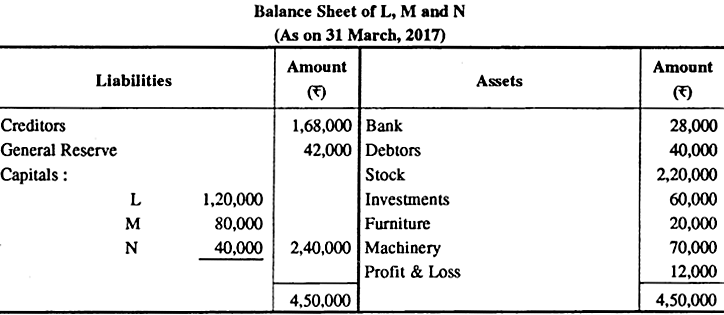

एल. एम. तथा एन. एक फर्म के साझेदार थे तथा 3:2:1 के अनुपात में लाभ बाँटते थे। 31.3.2017 को उनका स्थिति विवरण निम्न प्रकार से था

L. M. and N were partners in a firm sharing profits in the ratio of 3:2:1. Their Balance Sheet on 31.3.2017 was as follows :

उपर्युक्त तिथि को ‘ओ’ को एक नया साझेदार बनाया गया तथा यह निर्णय लिया कि

- एल. एम. एन. तथा ओ का नया लाभ अनुपात 2:2:1:1 होगा ।

- फर्म की ख्याति का मूल्यांकन Rs 1,80,000 किया गया तथा ओ अपने भाग की ख्याति (प्रीमियम) नकद लाया।

- निवेशों का बाजार मूल्य Rs 36,000 था।

- मशीनरी को Rs 58,000 तक घटाया जायेगा।

- Rs 6,000 का एक लेन्दारे दावा नहीं करेगा अत- उसे अपलिखित किया जायेगा।

- फर्म में लाभ के 1/6 भाग के लिए ओ आनुपातिक पूँजी लायेगा।

- देनदारों पर 5% की दर से संदिग्ध ऋणों के लिए आयोजन तथा 2% की दर से देनदारों पर बट्टे के लिए आयोजन किया जाये।

पुनर्मूल्यांकन खाता साझेदारों के पूँजी खाते तथा पुनर्गठित फर्म की स्थिति विवरण तैयार कीजिए।

- The new profit sharing ratio between L, M, N and O will be 2:2:1:1.

- Goodwill of the firm was valued at Rs 1,80,000 and O brought his share of goodwill (premium) in cash.

- The market value of investments was Rs 36,000.

- Machinery will be reduced to Rs 58,000.

- A creditor of Rs 6,000 was not likely to claim the amount and hence was to be written off.

- O will bring proportionate capital so as to give him 1/6th share in the profits of the firm.

- Provision for doubtful debts to be maintained @ 5% and Provision for discount on debtors be made @ 2%.

Prepare Revaluation Account, Partner’s Capital Account & Balance Sheet of the New Firm.

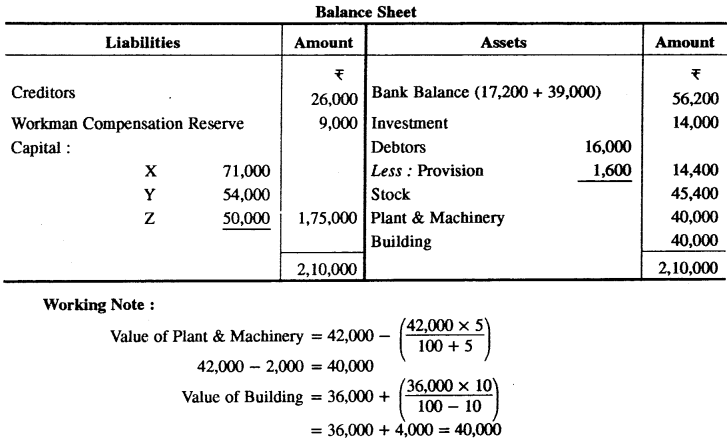

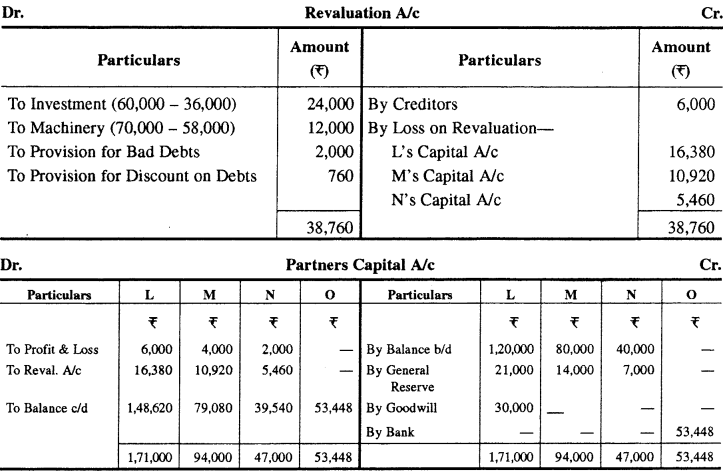

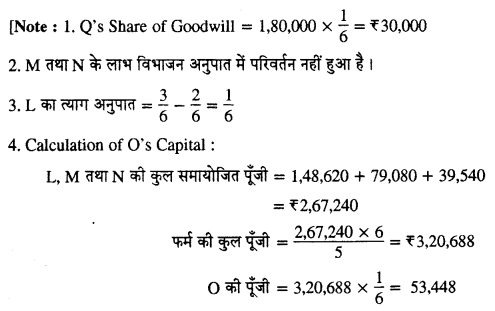

उत्तर:

![]()

प्रश्न 5.

ए व बी 5 : 3 में लाभ बाँटते हैं। उन्होंने सी को लाभ में 1/4 भाग के लिए फर्म में प्रवेश दिया जो कि ए व बी द्वारा बराबर-बराबर देय होगा। सी के प्रवेश से तुरन्त पूर्व फर्म का चिट्ठा निम्नांकित है

A and B shares the profits in the ratio of 5 : 3. They admit C into firm for a 1/4th share in the profits to be contributed equally by A and B. Before admission of C, Balance Sheet of the firm is as follows :

‘सी’ के प्रवेश की निम्न शर्ते थीं

- सी Rs 30,000 पूँजी व ख्याति के हिस्से के लिए लायेगा ।

- फर्म की ख्याति पिछले चार वर्षों के औसत अघिलाभ के तीन गुने के आधार पर मूल्यांकित करनी है। पिछले चार वर्षों का औसत लाभ Rs 20,000 है जबकि विनियोजित पूँजी पर सामान्य लाभ Rs 12,000 हैं।

- फर्नीचर का मूल्य Rs 6,000 से बढ़ाना है, जबकि स्टॉक का मूल्य Rs 2,000 से कम करना है। भविष्य निधि में Rs 1,000 बढ़ोत्तरी करनी है।

- सभी देनदार अच्छे हैं।

- कर्मचारी क्षतिपूर्ति संचय के विरुद्ध Rs 2,000 का दायित्व निश्चित किया गया है।

पुनर्मूल्यांकन खाता, साझेदारों के पूँजी खाते एवं नयी फर्म को चिट्ठा तैयार कीजिए।

Terms of C’s admission were as follows:

- C will bring Rs 30,000 as his share of Capital and Goodwill.

- Goodwill of the firm has been valued at 3 times of the average super-profits of last four years. Average profits of the last four years are Rs 20,000, while the normal profits that can be earned with the capital employed are Rs 12,000.

- Furniture to be appreciated by Rs 6,000 and the value of stock is to be reduced by Rs 2,000. Provident fund be raised by Rs 1,000.

- All debtors are good.

- Liability against Workmen Compensation Reserve is determined at Rs 2,000.

Prepare Revaluation Account, Partner’s Capital Accounts and the Balance Sheet of the new firm.

उत्तर:

Super Profit = Average Profit – Normal Profit

Super Profit = 20,000 – 12,000 = 78,000

Goodwill = 8,000 x 3 = Rs 24,000

C’s Goodwill = 24,000 x \(\frac { 1 }{ 4 }\) = Rs 6,000

![]()

प्रश्न 6.

अतथा बका31 मार्च, 2017 का चिट्ठा निम्न है जो लाभहानि को 3:1 में विभाजित करते हैं

The following is the Balance Sheet of A and B, who are sharing profit in the proportion of 3:1 on 31st March, 2017,

1st अप्रैल 2017 को वे निम्न शर्तों पर स को साझेदारी में शामिल करने को सहमत हो जाते हैं

- स लाभों में 1/5 भाग के लिए Rs 14,000 पूँजी वे ख्याति के लाएगा ।

- फर्म की ख्याति का मूल्यांकन Rs 20,000 किंया गया।

- स्टॉक तथा फर्नीचर का मूल्य 10% से कम किया जाये तथा देनदारों पर 5% की दर से संदिग्ध ऋणों के लिये प्रावधान बनाया जायेगा।

- भूमि और भवन का मूल्य 20% से बढ़ाया जायेगा।

- साझेदारों के पूँजी खाते को नये साझेदार की पूँजी के अनुपात में समायोजित किया जायेगा तथा किसी आधिक्य या कमी को के चालू खाते में हस्तान्तरित किया जायेगा।

पुनर्मूल्यांकन खस्ता साझेदारों के पूँजी खाते तथा नई फर्म का चिट्ठा बनाइए।

They agreed to take C in partnership on 1st April, 2017 on the following terms :

- C will pay Rs 14,000 as his capital and goodwill for 1/5th share in the future profits,

- That the goodwill of the firm be valued at Rs 20,000.

- The stock and furniture will be reduced by 10% and the provision for doubtful debts will be created @ 5% on debtors.

- Value of Land & Building be appreciated by 20%.

- That the capital accounts of the partners will be readjusted on the basis of new partners capital and any excess of deficiency transferred to their current accounts.

Prepare Revaluation account, Partner’s Capital accounts and Balance Sheet of the new firm.

उत्तर:

![]()

प्रश्न 7.

अ और ब लाभ 3:2 के अनुपात में बाँटते हैं। 31 मार्च, 2017 को उनका चिट्ठा निम्न प्रकार था

A and B distributes profit in 3 : 2 ratio. On 31st March, 2017 their Balance Sheet is as follows:

1st अप्रैल 2017 को निम्न शर्तों के आधार पर स को साझेदारी में शामिल किया

- साझेदारों का नया अनुपात 2:2:1 होगा ।

- सर 40,000 अपनी पूँजी के चुकाता है ।

- स्टॉक कोर 2,000 से कम किया जाये, संदिग्ध ऋणों के लिए आयोजन Rs 3,000 तक रखा जाये ।

- फर्म की ख्याति में स का हिस्सा Rs 5,000 पर मूल्यांकित किया जाये। स ख्याति की नकद राशि लाता है।

- पूर्वदत्त बीमा व्यय Rs 1,000 ।

- बकाया बिजली के बिल Rs 500.

- भवन Rs 10,000 से कम मूल्यांकित है।

- सभी साझेदारों की पूँजी उनके लाभ विभाजन अनुपात में होगी। नकद से समायोजन किया जाये।

नयी फर्म में पूँजी खाते एवं चिट्ठा तैयार कीजिये।

On 1st April, 2017 C was admitted in partnership on the following conditions :

- New ratio of partners will be 2:2:1.

- C pays 40,000 as his capital.

- Stock be decreased by Rs 2,000. Provision for Doubtful debts is to be maintained up to Rs 3,000.

- C’s share in the Goodwill of the firm be valued at Rs 5,000. C brings cash for Goodwill.

- Prepaid Insurance Rs 1,000.

- Outstanding Electricity Bills Rs 500.

- Building undervalued by Rs 10,000.

- The capitals of all partners will be in their profit sharing ratio.

Adjustment is to be done by cash. Prepare Capital Accounts and Balance Sheet of the new firm.

उत्तर:

Working Note 1. C’s Capital = 40,000

[Note : Bank Balance = 25,000 + 45,000 + 31,000 – 28,500 = Rs 72,500]

![]()

प्रश्न 8.

एम एवं एन एक फर्म में समान अनुपात में साझेदार हैं। 31 मार्च, 2017 को उनका चिट्ठा निम्न प्रकार है

M and N are partners in the firm in equal profit sharing ratio. On 31st March, 2017 their Balance Sheet is as follows.

उन्होंने ओ को निम्न शर्तों पर साझेदार बनाया

- देनदारों पर 10% वार्षिक दर से डूबत ऋण आयोजन बनाया जाये।

- फर्नीचर का मूल्य 25% से कम किया जाये।

- विनियोगों का मूल्य 5,000 से बढ़ाया जाये।

- ओर 25,000 पूँजी लायेगा तथा उसे लाभों में 13 हिस्सा दिया जायेगी और Rs 5,000 ख्याति के लाएगा ।

- एक लेनदार 1,700 का है जो मृत हैं। भविष्य में इस खाते पर कोई दायित्व उत्पन्न नहीं होगा।

- एकस्व मूल्यहीन है।

- भवन का मूल्य 25% से बढ़ाया जाए। स्टॉक का मूल्य Rs 9,000 तक कम करना है।

पुराने साझेदारों की पूँजी उसी के आधार पर समायोजित की जाएगी। पुनर्मूल्यांकन खाता साझेदारों के पूँजी खाते तथा चिट्ठा बनाइये।

They admit O in the partnership on the following terms :

- Create provision for Doubtful Debts by 10% on Debtors.

- Furniture will be depreciated by 25%.

- Increase the value of Investment by Rs 5,000.

- O shall bring Rs 25,000 as his capital and his share in profit & loss will be 1/3rd and he will bring Rs 5,000 as his share of goodwill.

- A creditor for Rs 1,700 is dead. No liability shall arise in future on this account.

- Patents are valueless.

- Building will be appreciated by 25%. Stock is reduced to 19,000.

The capitals of old partners are also to be adjusted accordingly. Prepare Revaluation A/c, Partners Capital A/c and Balance Sheet.

उत्तर:

[Note : Cash in Hand = 1,500 + (25,000 + 5,000) – (14,000 + 4,000) = Rs 13,500]

![]()

प्रश्न 9.

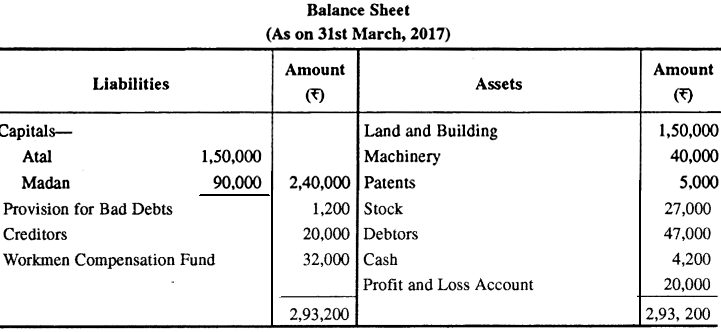

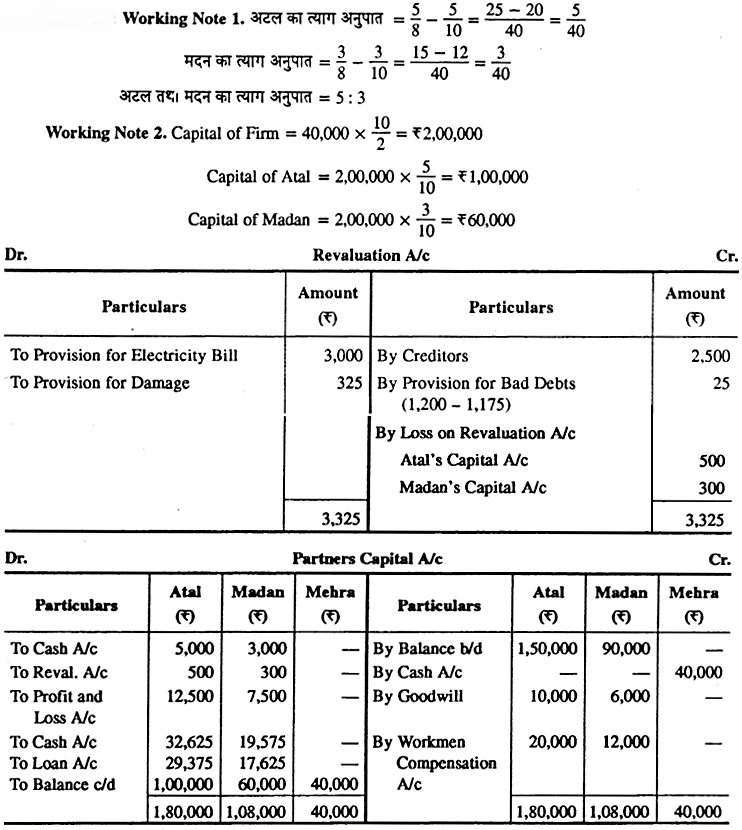

अटल तथा मदन एक फर्म के साझेदार थे तथा 5:3 के अनुपात में लाभ बाँटते थे। 31.3.2017 को उन्होंने लाभ के 1/5 वें भाग के लिए मेहरा को एक नया साझेदार बनायो । नया लाभ विभाजन अनुपात 5:3:2 था। मेहरा के प्रवेश के समय फर्म का स्थिति विवरण निम्न प्रकार से था-

Atal and Madan were partners in a firm sharing profits in the ratio of 5 : 3. On 31.3.2017 they admitted Mehra as a new partner for 1/5th share in the profits. The new profit sharing ratio was 5:3:2. On Mehra’s admission the Balance Sheet of the firm was as follows.

मेहरा के प्रवेश के समय यह निर्णय लिया गया कि :

- मेहरा अपनी पूँजी के लिए Rs 40,000 तथा ख्याति (प्रीमियम) के अपने भाग के लिए Rs 16,000 लाएगा, जिसका आधा भाग अटल तथा मदन ने निकाल लिया

- डूबत तथा संदिग्ध ऋणों के लिए \(2\frac { 1 }{ 2 }\)% का प्रावधान करना है ।

- विविध लेनदारों में Rs 2,500 की एक मद है जिसका भुगतान नहीं करना है।

- बिजली के अदत्त बिल के लिए Rs 3,000 का प्रावधान करना है।

- फर्म के विरुद्ध Rs 325 के एक क्षतिपूर्ति दावे के मंजूर होने की सम्भावना हें। उसके लिए प्रावधान करना है।

उपरोक्त समायोजनों के पश्चात् अटल तथा मदन की पूँजी को मेहरा की पूँजी के आधार पर समायोजित करना है। स्थिति के अनुसार अटल तथा मदन द्वारा रोकड़ लाई जाएगी अथवा उनको भुगतान की जाएगी।

पुनर्मूल्यांकन खाता, साझेदारों के पूँजी खाते तथा नई फर्म की स्थिति विवरण तैयार कीजिये।

On Mehra’s admission it was agreed that :

- Mehra will bring Rs 40,000 as his capital and Rs 16,000 for his share of goodwill (premium), half of which was withdrawn by Atal and Madan.

- A provision of \(2\frac { 1 }{ 2 }\)% for bad and doubtful debts was to be created.

- Included in the sundry creditors was an item of Rs 2,500 which was not to be paid.

- A provision was to be made for an outstanding bill for electricity Rs 3,000.

- A claim of Rs 325 for damages against the firm was likely to be admitted. Provision for the same was to be made.

After the above adjustments, the capitals of Atal and Madan were to be adjusted on the basis of Mehra’s capital. Actual cash was to be brought in or to be paid off to Atal and Madan as the case may be. Prepare Revaluation Account, Capital Accounts of the partners and the Balance Sheet of the new firm.

उत्तर:

[Note-पूँजी वापसी हेतु कमी की राशि को साझेदारों के ऋण खाते में दर्शाया गया है।]

![]()

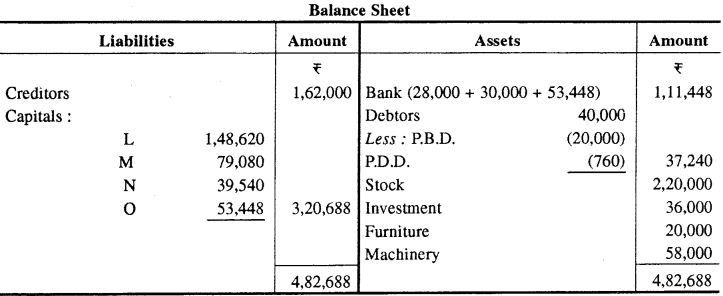

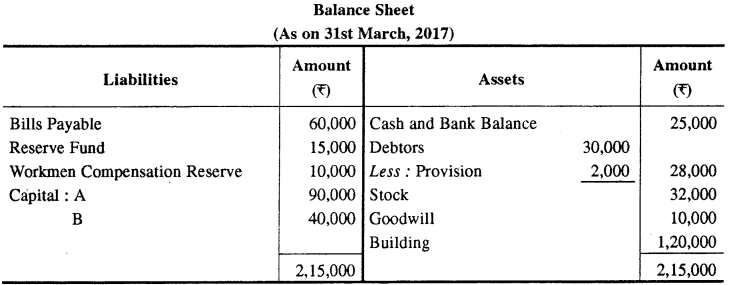

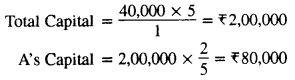

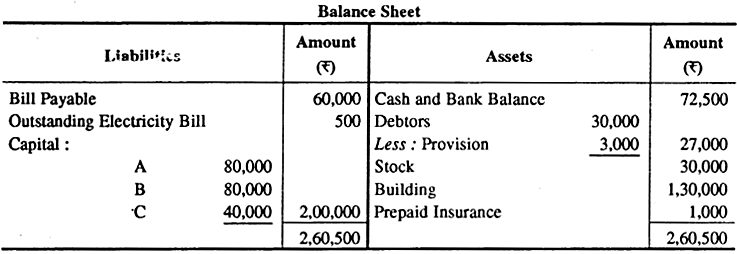

प्रश्न 10.

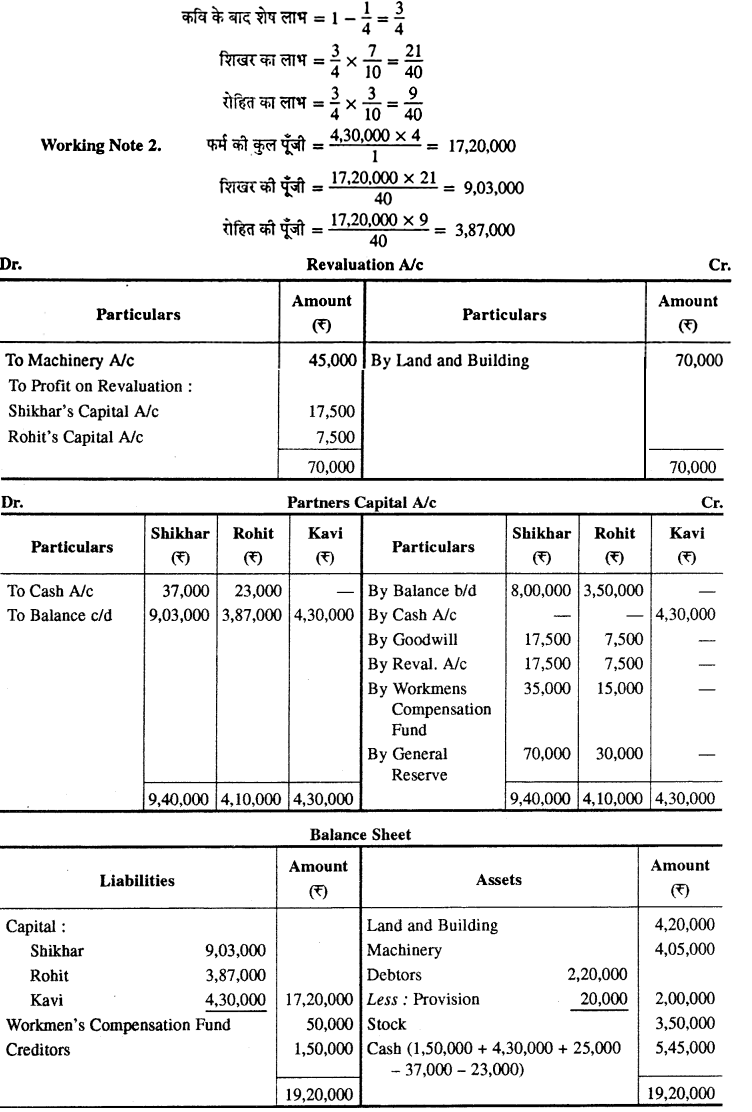

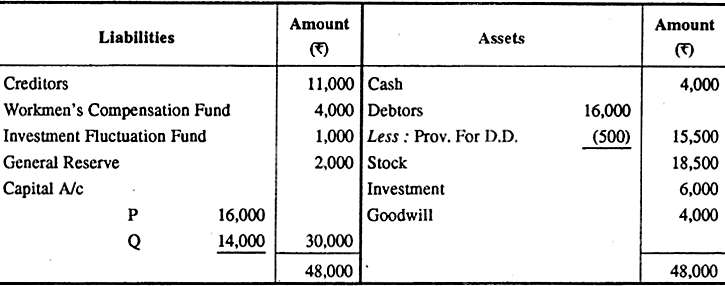

शिखर तथा रोहित एक फर्म में साझेदार थे तथा 7:3 के अनुपात में लाभ बाँटते थे। 1 अप्रैल, 2017 को उन्होंने कवि को फर्म के लाभों में 104 भाग के लिए एक नए साझेदार के रूप में प्रविष्ट कराया। कविर Rs 4,30,000 अपनी पूँजी के लिए तथा Rs 25,000 अपने ख्याति प्रीमियम के भाग के लिए लाया।1 अप्रैल, 2017 को शिखर तथा रोहित का स्थिति विवरण निम्नानुसार था

Shikhar and Rohit were partners in a firm sharing profits in the ratio of 7: 3. On 1st April, 2017 they admitted Ravi as a new partner for 1/4 share in profits of the firm. Ravi brought Rs 4,30,000 as his capital and Rs 25,000 for his share of goodwill premium. The Balance Sheet of Shikhar and Rohit on 1st April, 2017 was as follows:

यह निर्णय लिया गया कि–

- भूमि तथा भवन का मूल्य 20% से बढ़ाया जाएगा ।

- मशीनरी का मूल्य 10% से कम किया जाएगा ।

- कर्मचारी क्षतिपूर्ति निधि की देयता Rs 50,000 निश्चित की गई ।

- शिखर तथा रोहित की पूँजी कवि द्वारा लाई गई पूँजी के आधार पर समायोजित की जाएगी और इसके लिए आवश्यकतानुसार रोकड़ लाया जाएगा तथा इसका भुगतान किया जाएगा।

पुनर्मूल्यांकन खाता साझेदारों के पूँजी खाते तथा नई फर्म की स्थिति विवरण तैयार कीजिए।

It was agreed that :

- The value of Land and Building will be appreciated by 20%.

- The value of Machinery will be depreciated by 10%.

- The liabilities of Workmen’s Compensation Fund was determined at Rs 50,000.

- Capitals of Shikhar and Rohit will be adjusted on the basis of Ravi’s capital and actual cash to be brought in or to be paid off as the case may be.

Prepare Revaluation Account. Partner’s Capital Accounts and the Balance Sheet of the new firm.

उत्तर:

Working Note 1. नया लाभ विभाजन अनुपात की गणना

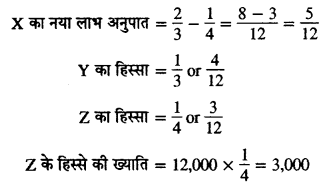

शिखर तथा रोहित का त्याग अनुपात = 7:3

![]()

प्रश्न 11.

A तथा B एक फर्म में साझेदार हैं और लाभ को 3:2 के अनुपात में बाँटते हैं। वे 1 अप्रैल, 2017 को C को लाभ में 1/5 हिस्से के लिए साझेदारी में सम्मिलित करते हैं। उस दिन का उनका स्थिति विवरण इस प्रकार था

A and B are partners in the firm sharing profit in the ratio of 3 : 2. On 1st April 2017. They admit C in new firm for 1/5 share in profit. Their balance sheet was as follows:

C को निम्नलिखित शर्तों पर सम्मिलित किया गया था

- C Rs 40,000 पूँजी के और Rs 15,000 ख्याति के लाएगा ।

- साझेदार भविष्य में लाभों को 5:3:2 के अनुपात में बाँटेंगे।

- निवेशों के मूल्य में 20% की वृद्धि की जाएगी और फर्नीचर में 10% का ह्रास किया जाएगा ।

- एक ग्राहक जिसे फर्म को Rs 2,000 देने थे, दिवालिया हो गया और उससे कुछ नहीं मिल पाएगा ।

- लेनदारों के Rs 2,000 कम किए जायेंगे।

- मरम्मत के 1,000 के बकाया बिले के लिए प्रावधान किया जाएगा ।

- निवेश पर उपार्जित (accrued) ब्याज Rs 2,000 था।

- साझेदारों की पूँजी उनके लाभ विभाजन अनुपात में होगी। इसके लिए समायोजन नकदी से किया जाएगा।

पुनर्मूल्यांकन खाता, साझेदारों के पूँजी खाते एवं नयी फर्म का चिट्ठा तैयार कीजिए।

C was admitted on the following terms :

- C is to bring capital Rs 40,000 and goodwill Rs 15,000.

- Partners agreed to share the future profits in the ratio of 5:3:2.

- Investments will be appreciated by 20% and furniture depreciated by 10%.

- One customer who owed the firm Rs 2,000 becomes insolvent and nothing could be released from him.

- Creditors will be written off Rs 2,000.

- Outstanding bills for repairs Rs 1,000 will be provided for.

- Interest accrued on investment Rs 2,000.

- Capitals of the partner’s shall be in proportion to their profits sharing ratio.

For this, adjustment be made through cash. Prepare Revaluation Account, Capital Accounts and the Balance Sheet of new firm.

उत्तर:

[Note-Cash in Hand = 15,000 + (40,000 + 15,000 + 27,400) – 900 = Rs 96,500]

![]()

प्रश्न 12.

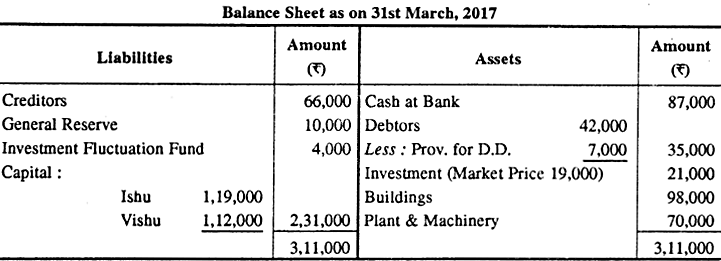

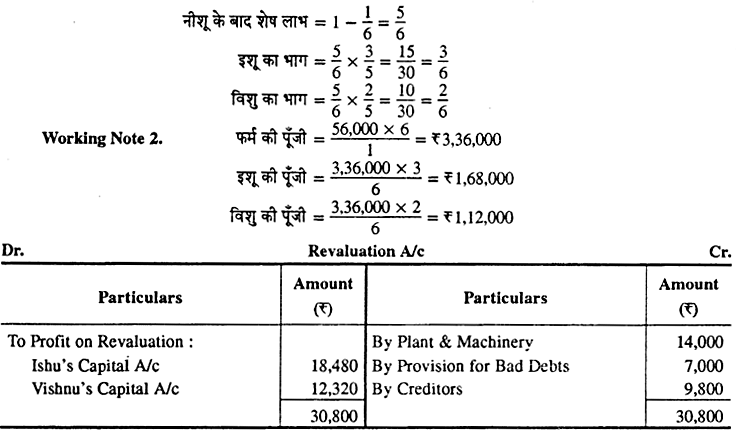

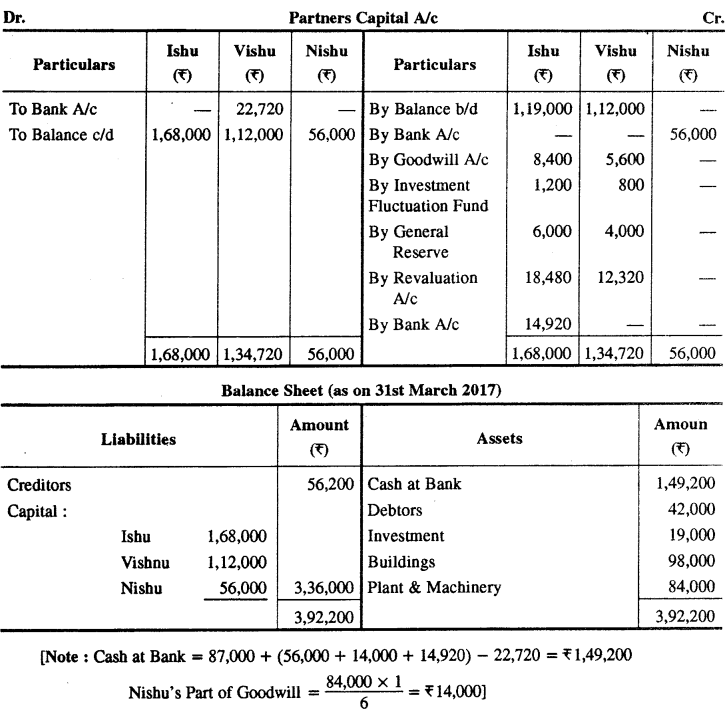

इशु और विशु 3:2 के अनुपात में लाभ बाँटते हुए साझेदार हैं। 31 मार्च 2017 को उनका चिट्ठा निम्न प्रकार था-

Ishu and Vishu are partners sharing profits in the ratio of 3 : 2. Their Balance Sheet as on 31st March 2017 was as follows:

नीशू को इस दिन 1/6 भाग पर निम्न शर्तो पर सम्मिलित किया-

- नीशूर Rs 56,000 अपने हिस्से की पूँजी लाएगा।

- फर्म की ख्याति Rs 84,000 ऑकी गई और नीशू अपना ख्याति का हिस्सा नकद लाएगा।

- प्लांट व मशीन को 20% बढ़ा दिया जाए।

- देनदार सभी उत्तम है।

- Rs 9,800 का दायित्व जो लेनदारों में शामिल है, उसे नहीं देना पड़ेगा।

- नीशू की पूँजी के आधार पर इशु और विशु की पूँजी का समायोजन करें तथा कमी या अधिकता को नकद से पूरा करें ।

पुनर्मूल्यांकन खाता, साझेदारी के पूँजी खाते व फर्म का समायोजन के बाद स्थिति विवरण बनायें

Nishu was admitted on that date for 1/6th share on the following terms :

- Nishu will bring Rs 56,000 as his share of capital.

- Goodwill of the firm is valued at Rs 84,000 and Nishu will bring his share of goodwill in cash.

- Plant and Machinery be appreciated by 20%.

- all debtors are good.

- There is a liability of Rs 9,800 included in Sundry creditors that is not likely to arise.

- Capital of Ishu and Vishu will be adjusted on the basis of Nishu’s capital and any excess or deficiency will be made by withdrawing or bringing in cash by concerned partner.

Prepare Revaluation Account, Partner’s Capital Accounts and the Balance Sheet of the firm after the above adjustments.

उत्तर:

Working Note 1. इशु और विशु का त्याग अनुपात = 3:2

![]()

प्रश्न 13.

A तथा B साझेदार हैं। लाभ को 3:2 के अनुपात में बाँटते हैं। 31 दिसम्बर, 2016 को उनका स्थिति विवरण इस प्रकार था

A and B who are partners in a firm sharing profits in the ratio of 3 : 2. On 31st December, 2016 their Balance Sheet was as follows:

उन्होंने C को लाभ में 1/5 हिस्से के लिए निम्नलिखित शर्तों पर साझेदारी में सम्मिलित करने का निर्णय लिया–

- संदिग्ध ऋण के लिए प्रावधान कोर Rs 2,000 से बढ़ा दिया जाए।

- स्टॉक के मूल्य कोर Rs 4,000 से बढ़ा दिया जाए और भूमि तथा मदन के मूल्य को Rs 18,000 तक बढ़ा दिया जाए।

- कर्मचारी क्षतिपूर्ति कोष से दायित्व Rs 2,000 निर्धारित किया गया है।

- C ख्याति का अपना हिस्सा Rs 10,000 नकद लाया ।

- उपरोक्त पुनर्मूल्यांकन तथा समायोजन कर लेने के बाद अपनी पूँजी के लिए A व B की संयुक्त पूँजी के 20% के बराबर राशि लाएगा ।

पुनर्मूल्यांकन खाता, साझेदारों के पूँजी खाते और C के प्रवेश के बाद फर्म की स्थिति विवरण बनाइए।

They agreed to admit C into partnership for 1/5th share of profits on the following terms :

- Provision for doubtful debts be increased by Rs 2,000.

- The value of stock be increased by Rs 4,000 and Land & Building be increased to Rs 18,000.

- The liability against workmen’s compensation fund is determined at 2,000.

- C brought in as his share of goodwill Rs 10,000 in cash.

- C would bring cash as would make his capital equal to 20% of combined capital of A & B, after the above revaluation and adjustments are carried out.

Prepare Revaluation Account. Partners Capital Accounts and the Balance Sheet of the firm after C’s admission.

उत्तर:

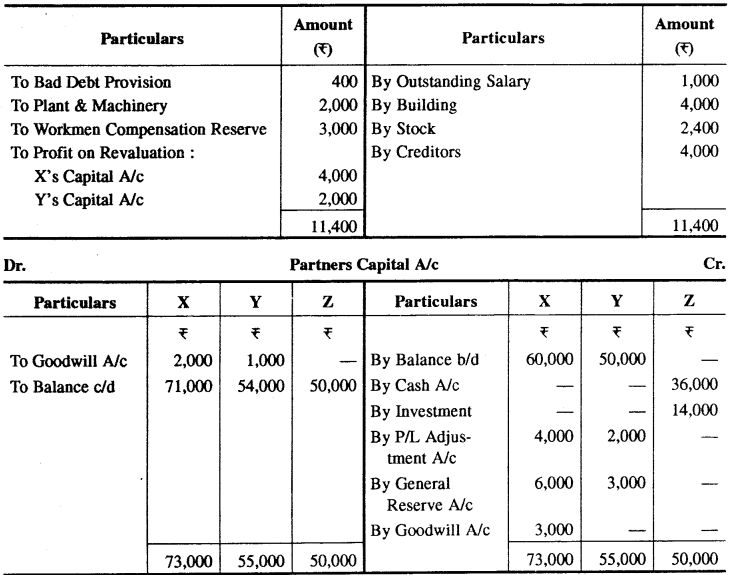

working Note : A तथा B का त्याग अनुपात = 3:2

![]()

प्रश्न 14.

P तथा Q एक फर्म में साझेदार हैं। लाभ को 3:1 के अनुपात में बाँटते हैं। उनका स्थिति विवरण इस प्रकार है

P and Q are partners in a firm sharing profits in the ratio of 3 : 1. Their Balance Sheet was as follows:

R को निम्नलिखित शर्तो पर लाभ में 1/5 हिस्से के लिए सम्मिलित किया जाता है-

- निवेशों का बाजार मूल्य Rs 4,200 माना गया हैं।

- उपार्जित ब्याज की राशि Rs 200 है।

- संदिग्ध ऋणों के लिए प्रावधान Rs 200 अधिक है।

- कर्मचारी क्षतिपूर्ति के एक दावे के लिए Rs 1,000 का प्रावधान किया जाए।

- R ख्याति के हिस्से के रूप में से 10,000 लाएगा ।

- फर्म की कुल पूँजी

Rs 5,000 निर्धारित की गई, जो माड़ोदारों के लाभ विभाजन अनुपात में समायोजित की जानी है। R अपनी पूँजी नकद में लाता है, परन्तु अन्य साझेदारों की पूँजी का समायोजन चालू खाते खोलकर किया जाए। पुनर्मूल्यांकन खाता, पूँजी खाते और नयी फर्म का स्थिति विवरण बुझाइये ।

R is admitted on 1/5th share in profit on the following terms:

- Market value of investment is taken as Rs 4,200.

- Accrued. Interest amounts to Rs 200.

- Provision for doubtful debt was in excess to Rs 200.

- A claim of Workmen’s Compensation for Rs 1,000 he provided.

- R is to bring Rs 10,000 as goodwill share.

- Total capital of the firm was agreed as Rs 50,000 to be adjusted in their profit sharing ratio.

![]()

R brings his capital in cash but capital of other partners be adjusted by opening current accounts. Prepare Revaluation Account, Capital Accounts and the Balance Sheet of new firm.

उत्तर:

Working Note

1. नवा अई विभाजन अनुपात-

P व Q का त्याग अनुपात = 3:1

प्रश्न 15.

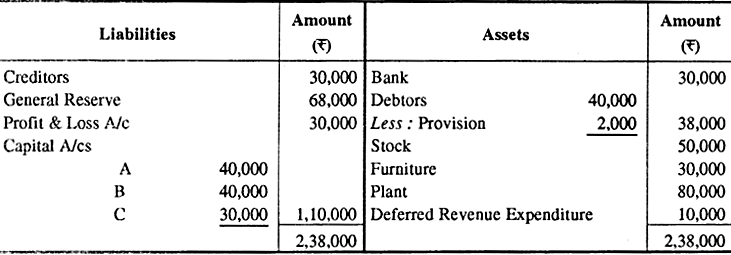

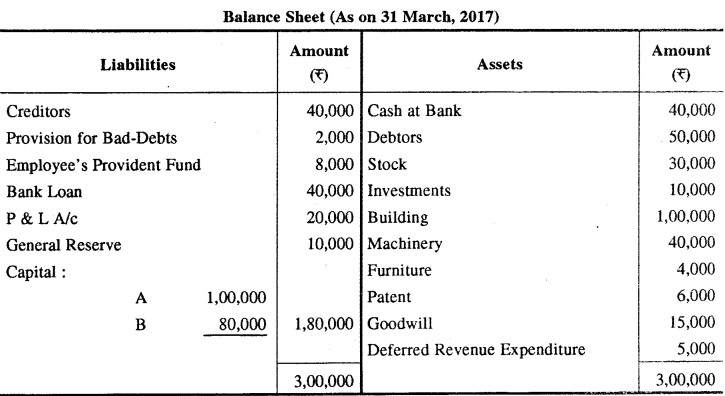

A, B तथा C सादार हैं और लाभ को 2 : 2 : 1 के अनुपात में बाँटते हैं। 31.3.2017 को उनका स्थिति विवरण इस प्रकार था

A, B and C are partners sharing profits in the ratio 2:2: 1. Their balance sheet on 31-3-2017 was as follows:

साझेदारों ने 1.4.2017 से लाभ को 1:1:1 के अनुपात में बाँटने का निर्णय लिया। उन्होंने यह भी तय किया कि :

- स्टॉक का मूल्य 20% बढ़ा दिया जाए।

- संदिग्ध ऋण के लिए प्रावधान Rs 1,000 से बढ़ा दिया जाए।

- फर्नीचर तथा प्लांट में 10% का ह्रास किया जाए।

- बकाया किराया Rs 2,000 हैं।

- फर्म की ख्याति का मूल्यांकन Rs 51,000 किया गया है।

![]()

साझेदारों ने निर्णय लिया कि सम्पत्तियों, दायित्वों और संचयों के मूल्य में कोई परिवर्तन किया जाए। उन्होंने ख्याति को पुस्तकों में न दिखाने का भी निर्णय लिया ।इन परिवर्तनों को लागू करने के एकल प्रविष्टि कीजिए।

The partners agreed to share profits in the ratio 1:1:1 from 1.4.2017. They further agreed that:

- Stock be valued at 20% more.

- Doubtful debt provision be increased by Rs 1,000.

- Depreciate furniture and plant by 10%.

- Rent outstanding is Rs 2,000.

- Goodwill of the firm is valued at Rs 51,000.

partners decided not to alter the values of assets, liabilities and reserves. They also decided not to show goodwill in the books. Pass a single entry to give the effect to above charges.

उत्तर:

General Entry

C’s Capital A/C Dr. 18,000

To A’s Capital A/c 9,000

To B’s Capital A/c 9,000

(Being adjustment made)

Profit on Adjustment = Goodwill + General Reserve + Profit &

Loss – Deferred Revenue Exp. – Loss on Revaluation

= 51,000 + 68,000 + 30,000 – 10,000 – 4,000 = Rs 1,35,000

प्रश्न 16.

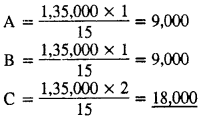

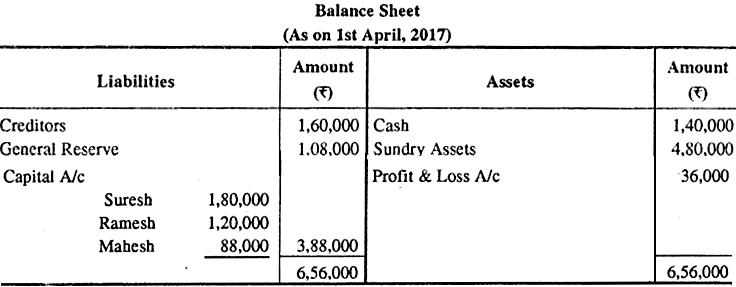

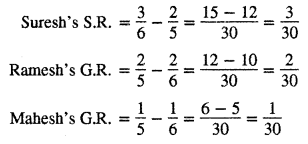

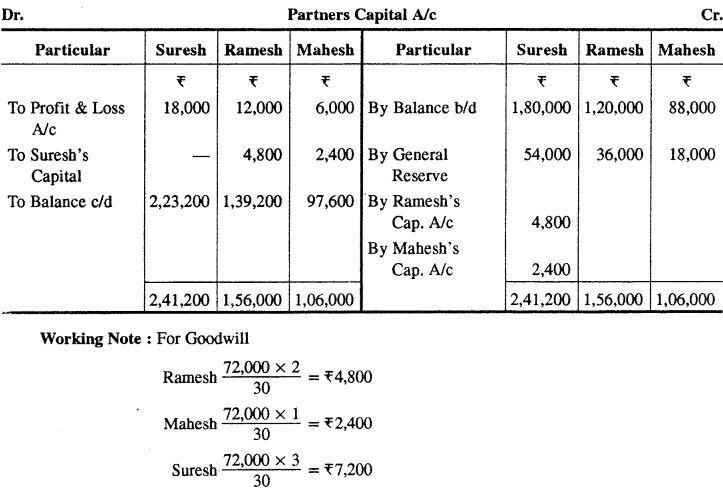

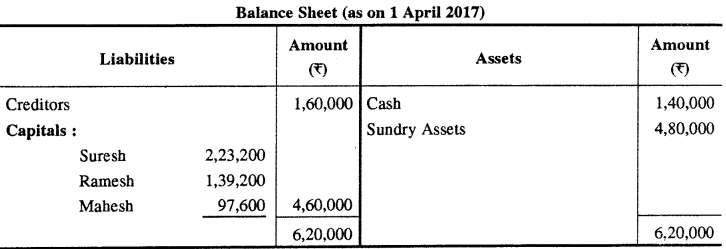

सुरेश, रमेश तथा महेश लाभों को क्रमशः 3:2:1 के अनुपात में बाँटते हैं। 1 अप्रैल, 2017 को उनका चिट्ठा निम्नलिखित था-

Suresh, Ramesh and Mahesh share profits in the ratio of 3:2:1 respectively. Their Balance Sheet as on 1st April, 2017 was as-

इस तिथि को उन्होंने तय किया कि सुरेश, रमेश तथा महेश भविष्य में लाभों को 2:2:1 अनुपात में बाँटेंगे। उस तिथि को फर्म की ख्याति का मूल्य Rs 72,000 किया गया। फर्म की पुस्तकों में साझेदारों के पूँजी खाते बनाइये तथा फर्म को चिट्ठा बनाइये।

On that date they decided that Suresh, Ramesh and Mahesh will share profits in future in the ratio of 2:2: 1 respectively. The goodwill of the firm was valued at Rs 72,000 on that date. Prepare Partner’s Capital Accounts and Balance Sheet of the firm.

उत्तर:

Working Note :

Profit on Adjustment = Goodwill + General Reserve – Profit & Loss A/c

= 72,000 + 1,08,000 – 36,000

= Rs 1,44,000

![]()

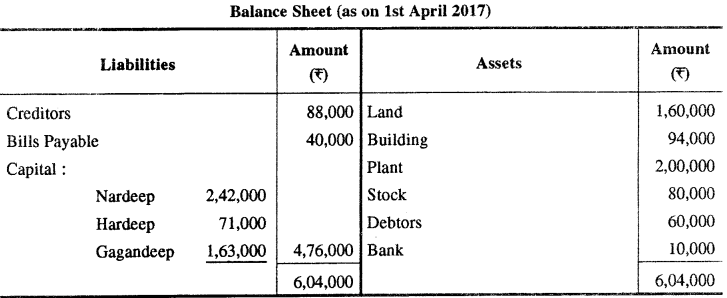

प्रश्न 17.

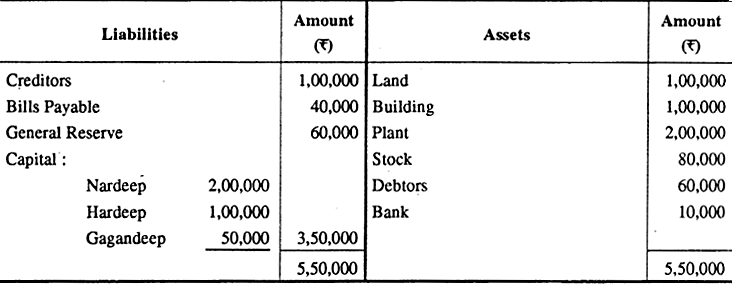

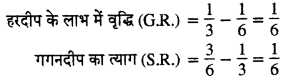

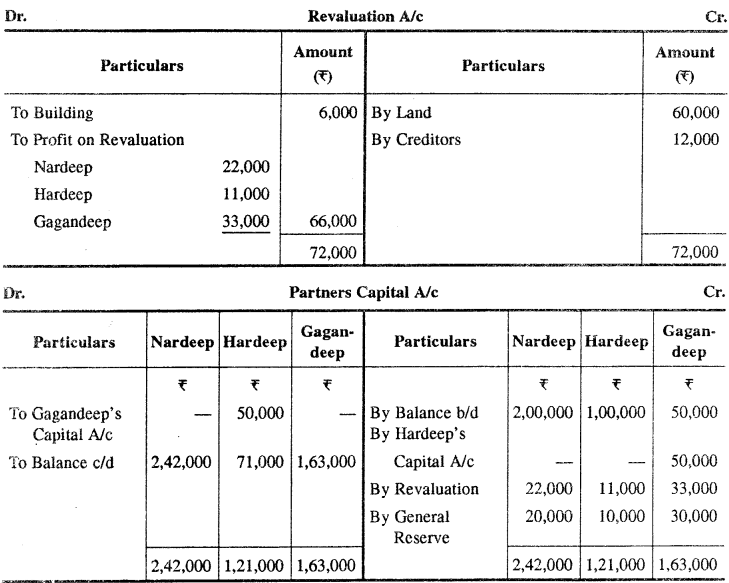

नरदीप, हरदीप तथा गगनदीप एक फर्म के साझेदार थे तथा 2:1:3 के अनुपात में लाभ बाँटते थे। 31.03.2017 को उनका स्थिति विवरण निम्न प्रकार से था

Nardeep, Hardeep and Gangandeep were partners in a firm sharing profits in 2:1:3 ratio. Their Balance sheet as on 31.3.2017 was as follows :

14.2017 से नरदीप हुरदीप तथा गगनदीप ने भविष्य में लाभ बराबर-बराबर बाँटने का निर्णय लिया इसके लिए यह समझौता हुआ कि-

(क) फर्म की ख्याति का मूल्यांकनर Rs 3,00,000 किया जाये।

(ख) भूमि का पुनर्मूल्यांकन Rs 1,60,000 पर किया जाये तथा भवन पर 6% मूल्य ह्रास लगाया जाये।

(ग) Rs 12,000 के लेनदार दावा नहीं करेंगे अतः इन्हें अपलिखित कर दिया जाना चाहिए।

पुनर्मूल्यांकन खाता साझेदारों के पूँजी खाते तथा पुनर्गठित फर्म का स्थिति विवरण तैयार कीजिए।

From 1.4.2017, Nardeep, Hardeep and Gagandeep decided to share the future profits equally. For this purpose it was decided that : (a) Goodwill of the firm be valued at Rs 3,00,000.

(b) Land be revalued at Rs 1,60,000 and building be depreciated by 6%.

(c) Creditors of Rs 12,000 were not likely to be claimed and hence be written off.

Prepare Revaluation Account, Partners Capital Accounts and the Balance Sheet of the reconstituted firm.

उत्तर:

Working Note :

नरदीप, हरदीप तथा गगनदीप का नया लाभ अनुपात = 1:1:1

![]()

प्रश्न 18.

A व B एक फर्म में 3:2 के अनुपात में लाभ विभाजन करते हुए साझेदार हैं। 31.03.17 को उनकी स्थिति विवरण निम्न प्रकार था

A & B are partners sharing profit in the ratio of 3 : 2 in a firm. On 31.3.2017 their Balance Sheet was as follows:

वे C को लाभों में 1/5 हिस्से के लिए प्रवेश देते हैं-C अपना पूरा हिस्सा A से प्राप्त करता है। C अपने लाभ के 1/5 भाग के लिए आनुपातिक पूँजी लायेगा ।

- फर्म की ख्याति का मूल्यांकन पिछले 3 वर्षों के औसत लाभों Rs 10,000 के दो वर्षों के क्रय के बराबर किया गया। C ख्याति की राशि नकद लाता है।

- ऐसी सम्पत्ति जिसका पुस्तकों में लेखी नहीं हुआ Rs 10,000 ।

- विनियोगों का मूल्यांकन Rs 12,000 पर किया गया व इसी मूल्य पर A ने ले लिए।

- सामान्य संचय की आधी राशि साझेदारों ने निकाल ली ।

- भवन के मूल्य में 10% से वृद्धि की गयी।

- मशीन का मूल्य 10% अधिक करना है।

- फर्नीचर का मूल्य 10% कम करना है।

- अदत्त वेतन Rs 2,000 ।

- एकस्व का मूल्य Rs 3,000 से कम करें ।

- कर्मचारी क्षतिपूर्ति संचय के विरुद्धर 2,000 का दायित्व निश्चित किया गया ।

- पूर्वदत्त बीमार 1,000 ।

- बैंक ऋण का भुगतान कर दिया गया है ।

- लेनदारों में शामिलर 4,000 के दायित्व का भुगतान नहीं करना है ।

- डूबते ऋण Rs 3,000 ।

- स्कन्ध को Rs 26,000 तक कम करें ।

पुनर्मूल्यांकन खाता, साझेदारों के पूँजी खाते व नयी फर्म का चिट्ठा बनाइये।

They decided to admit C for 1/5th share. he takes his share entirely from A. He had to contribute the proportionate capital.

- Goodwill for the firm is valued at 2 years purchase of average profit of last 3 years. Which was Rs 10,000. C brings his share of goodwill in cash.

- Unrecorded Assets Rs 10,000.

- Investment valued at Rs 12,000 & taken by A.

- 1/2 of General Reserve withdrawn by the partners.

- Building appreciate by 10%.

- Machinery valued at 20% more.

- Furniture valued at 10% Less.

- Outstanding Salary Rs 2,000.

- Patent reduced by Rs 3,000.

- Liability of Workmen compensation is Rs 2,000.

- Prepaid Insurance Rs 1,000.

- Bank Loan would be paid off.

- A Liability of Rs 4,000 included in creditors was not likely to arise.

- Bad debts Rs 3,000.

- Stock is reduced to Rs 26,000.

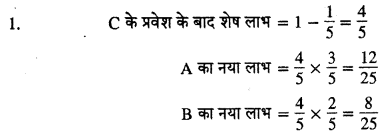

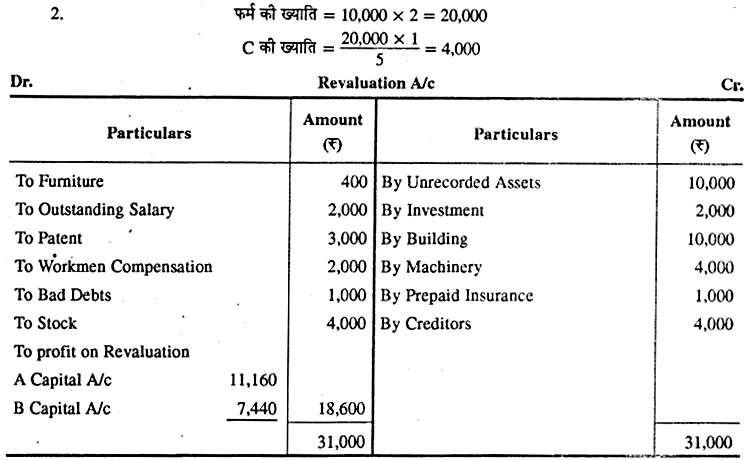

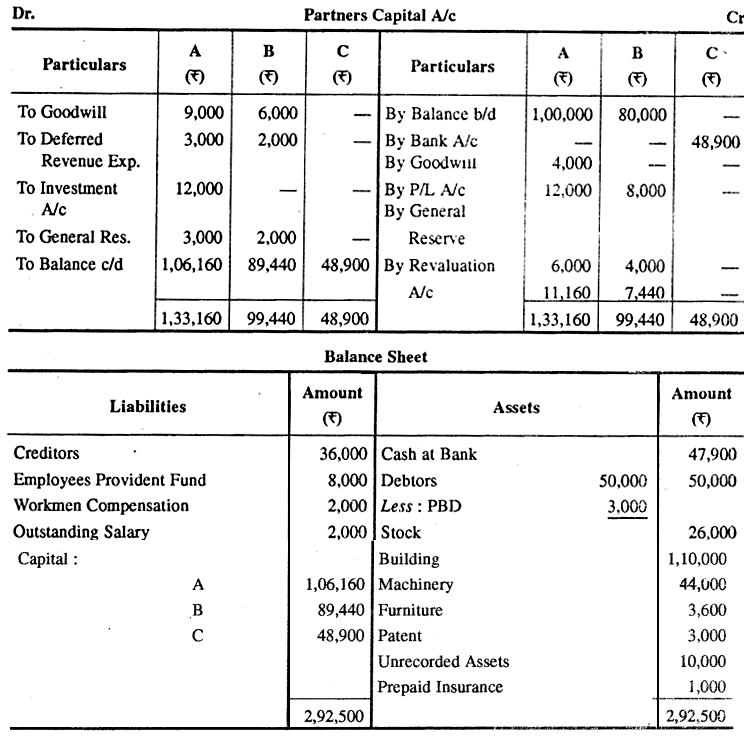

![]()

Prepare Revaluation A/C, Partner’s Capital A/cs and the Balance Sheet of the new firm.

उत्तर:

Working Note :